Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

How Industry Changes Will Impact the Homebuying Process

Changes are coming to common real estate practices. Find out what they are before you buy or list a home for sale.

If it’s been some time since you bought or sold a home, there are recent changes to the selling process you need to be aware of. These are part of nationwide changes from the National Association of Realtors® (NAR) and how homes are promoted in Multiple Listing Services (MLS) – regional databases across the country that compile information about homes for sale and sold, as well as rental properties that use an agent during the leasing process. Updates are designed to give consumers a better understanding of how they can negotiate fees associated with buying or selling a home and will take effect August 14.

It’s important to know that in our region Realtors® have been following these practices for decades, allowing for a clear and fair sales process that encourages both buyers and sellers to have their own representation in a sales transaction and negotiate their agent’s fee for service. What has changed is that a broker’s fee is not only more clear to the buyer but can now be a potential negotiating item of the buyer-seller contract, rather than being listed in an MLS as a co-operating fee between brokerages.

Here are some things to be aware of:

Buyers

- Your first step will be to sign a Buyer Agency agreement that will outline the ways your Realtor® will represent you in your search for a new home and how they will be paid for their professional services.

- Buyers can negotiate many terms in their offer to purchase, including cash concessions from the seller to help cover different costs associated with buying a home. This now includes negotiating for the seller to pay a buyer broker’s fee.

- The Department of Veteran Affairs (VA) announced a temporary policy allowing VA buyers to compensate their real estate agents directly.

- Not all sellers will consider financial concessions so it’s important to set your home purchase budget to cover all costs associated with the sale, including your agent’s fee.

- Read more at NAR’s resource page for homebuyers.

Sellers

- Your first step will be to sign a Listing Agreement that will outline the ways your Realtor® will represent you in the sale of your home, including how they will be paid for their professional services.

- Your Realtor® will advise you on current market conditions and what will make your home attractive to the greatest number of potential buyers.

- Sellers can indicate if they will consider concessions to a buyer but they are not obligated to do so. Sellers should evaluate offers to purchase their home based on all specific terms and conditions, which may include a request for cash concessions to cover a buyer’s costs, including their broker’s fee.

- Read more at NAR’s resource page for sellers.

A professional Realtor® is your best advocate and will work with you to develop the strategy that works best for your goals. Reach out to one of our agents to get started on your next move!

Take a look at our website for all of our listings available throughout Washington, D.C., Maryland, and Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Building Better Communities With Housing Sustainability

One agent’s firsthand report at how NAR’s focus on sustainability is preserving housing inventory and the land it sits on.

The National Association of Realtors® 2024 Sustainability Summit was held in early June in Minneapolis with a focus on initiatives to upgrade our nation’s housing stock, add client value, increase business, and lead on an urgent global issue. As an agent who is committed to helping my clients find new and innovative ways to increase value in their homes and build more resilient communities, I was excited to hear what’s coming to the sustainability market from those working in the sustainability industry.

Realtors® work to help our buyers and sellers navigate myriad changes in an accelerated landscape, something the Sustainability Summit reinforced with each panel discussion. As the organizers laid out in the mission of the conference, “(Agents) understand that sustainability isn’t a box to check, but a fundamental part of our job. Our inventory requires stewardship. The properties we help people call home must be maintained, protected, and updated to grow in value.”

The summit had an emphasis on high-performance homes, which are properties with features that increase energy efficiency, prioritize climate resiliency, and reduce emissions while reinforcing comfort, durability, and a healthy indoor environment. Mentioned throughout the meeting were organizations and resources that provide standards to measure these features, like the non-profit Passive House Institute US, Inc. (PHIUS) and the Department of Energy’s Pearl Certification. These provide savvy agents and their buyer-clients quantifiable ways to compare properties and interpret results. These standards will also help seller-clients leverage these features when marketing their homes.

Forward-thinking speakers dominated the panels, including Rohit Bhargava, the summit’s keynote speaker and best-selling author of How to be a Non-Obvious Thinker (And See What Others Miss), the newest addition to his Non-Obvious Thinking book series. In his presentation he shared, ““Obvious Thinking is the inability to imagine something different, think bigger, be open minded, or shift your perspective” and challenged participants to invest in unconventional thinking to inspire change within the industry and serve the public.

Bhargava’s presentation resonated because while real estate has always been a dynamic field, factors like fluctuating interest rates, reduced inventory, and rising prices are affecting housing sales nationwide. Other influencers such as technical innovations and climate change, and developments in related industries like public utilities and insurance companies, are all moving parts that affect housing and sustainability advances.

Sustainability, stewardship, and home ownership go hand-in-hand, and as housing professionals we work to educate our clients, help them navigate industry changes, avoid expensive or unnecessary pitfalls, and maximize not only a property’s environmental benefits but its investment value as well.

If you are interested in working with a Realtor® who has advanced knowledge about these initiatives, look for agents with NAR’s GREEN or a LEED Green Associate designation as they have completed additional training in issues of energy efficiency and sustainability in real estate. There are many within our McEnearney | Middleburg Real Estate | Atoka Properties family and we’re excited to share our passion for building great communities!

Since permanently moving back to Northern Virginia, JaneEllen McLaughlin Saums developed an intimate knowledge of its diverse communities, and thanks to her teaching background, JaneEllen has always educates her clients on the area’s market and housing options, to make sure that they find the best place suited to them to call home.

Take a look at our website for all of our listings available throughout Washington, D.C., Maryland, and Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Why Homeownership is a National Priority

Owning a home doesn’t have to be a dream. Check out these initiatives and resources to get buyers in a position to make homeownership a reality.

June is a month for graduations, weddings, and summer dreams. It’s also the month when Realtors® and housing advocates promote various pathways to homeownership, a goal for those who want to build generational wealth and create a place to call their own.

But the truth is that buying a home in 2024 is challenging, and it is harder for some groups to take that first step to homeownership. According to Realtor.com research, low-income earners are 22% more likely to be denied a loan, LGBTQ+ are 25% less likely to own a home compared to all Americans, one in four Hispanic individuals complete the home-buying process entirely in Spanish, seven in 10 veterans are unaware they qualify for a zero-down home loan, and the gap between Black versus white homeownership is worse today than in 1968 when the Fair Housing Act was passed.

The Census Bureau’s quarterly report for Q1 2024 showed the latest homeownership rate is at 65.6%, down 0.1 percentage points from Q4 2023 and the lowest rate in two years. On May 31 the Biden administration issued a Proclamation on National Homeownership Month 2024, calling upon “the people of this Nation to safeguard the American Dream by ensuring that everyone has access to an affordable home in a community of their choice.”

Put simply, the proclamation states, “Whether they rent or buy, Americans deserve a safe place to call home.”

Some of the proposed initiatives to make homeownership more accessible include:

- A tax credit of $5,000 per year for the next 2 years for any family earning under $200,000 — money they can put toward a mortgage when they buy their first home or trade up for more space.

- My plan would also provide first-generation homebuyers with $25,000 for a down payment.

- A pilot program run by the Federal Housing Administration (FHA) to make it more affordable to refinance a home by eliminating title insurance fees on certain federally backed mortgages, which would save buyers $1,500 at closing.

- The FHA is now considering positive rental history when making decisions about creditworthiness — ensuring that the people who could qualify for mortgage financing receive it.

- Advancement in fair housing practices, including by rooting out bias in the home appraisal process, which keeps too many Black and Brown families from enjoying the full financial returns of homeownership.

Homeownership In Our Region

Let’s start with a look at what local buyers are up against. Overall, Realtor.com statistics shows the Washington, DC/Northern Virginia/Maryland/West Virginia region with a median listing price of $640,000 (unchanged from May 2023). The District, which is not a state, ranks the lowest in both our region and the nation at 43.9% for homeownership. There are many factors that contribute to this lower rate of homeownership, including a higher transition rate of people moving in-and-out of the region (9.8% for DC compared to 2.5% nationally). This is partly explained by the number of universities, embassies, research facilities and government contract work that brings short-term residents to the area, but high housing costs are another factor. According to Realtor.com the median listing home price in Washington, DC was $614,900 in May 2024 (trending down -5.4% year-over-year) while the median home sold price was $697,500.

On the other end of the scale is West Virginia, which ranked highest in the nation at 74.7%, thanks in part to home values that are less than half that for the entire country. Again from Realtor.com, the median listing home price in Charleston, WV was $182.500 in May 2024 (trending down -13.1% year-over-year) while median home sold price was $181.900. Comparing the two areas, it’s clear that a buyer’s dollar is going to go much further in West Virginia than DC.

Rounding out the homeownership review is Virginia at 69.9% and Maryland at 70.9%. The average sales price in Northern Virginia in May 2024 was $882,180, up 10.2% the previous year’s average of $800.427, while the median sales price was $760,000 in May 2024, up from $715,000 in May 2023. Meanwhile, the average Maryland home value was $421,804, up 4.0% over the past year.

Where To Start?

Buyers in the DC-Metro area need a strong and strategic game plan to succeed in our competitive and expensive local market. The first step a buyer should take is to hire a Realtor® to assist in their search for a home. Agents have the resources, connections, insight to help buyers navigate the buying process and save their clients from the pitfalls of going into a major financial negotiation unprepared and unrepresented. An agent will connect buyers with savvy lenders who know the best financing and grant programs available and can guide buyers through complicated scenarios with many moving pieces.

First-time home buyers have it the hardest in this current market, with interest rates higher than they’ve been in decades (although still relatively moderate in the 6-7% rate range), high home prices, and limited equity. But a little bit of research and preparation goes a long way! Both Realtor.com and the U.S. Department of Housing and Urban Development (HUD) have extensive resources to tap, in addition to the advice their agent will offer.

Putting It All Together

Deciding to buy a home is a personal, economic, and logistical process. It’s not always the right choice for everyone, but for those who have a goal to become a homeowner, put down roots in a community, and begin building financial security through home equity, there is a way forward. Start with a conversation with an experienced McEnearney | Middleburg Real Estate | Atoka Properties agent and see which path is right for you,

Additional Resources for National Homeownership Month:

- PropertyAction.Realtor

- Northern Virginia Association of Realtors®

- American Property Owners Alliance

- Greater Capital Area Association of Realtors®

- West Virginia Housing Development Fund

Take a look at our website for all of our listings available throughout Washington, D.C., Maryland, and Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Why FSBOs Don’t Deliver For Sellers

No matter how hot the market is, homes listed with a Realtor® garner higher prices and faster closings than those sold directly by owners.

In a hot seller’s market like what the DC-Metro region has experienced for several years, it might seem like all owners have to do to sell a property is to stick a sign in the yard and wait for buyers to stream in. But, according to NAR’s research, For Sale By Owner (FSBO) transactions accounted for just 7% of home sales in 2023, a historic low that tied with 2021 for the fewest number of FSBO listings.

Even more striking is that the typical FSBO property sold for a median of just $310,000 compared to the median of $405,000 for properties sold with the assistance of an agent – almost $100,000 and 30% less.

To paraphrase “Field of Dreams,” it would appear that selling a home is a lot more challenging than simply intoning, “If you list it, they will come.”

What these FSBO owners discovered is that a buyer liking a home is just one of many steps on the path to closing a deal, and without a professional Realtor® who understands not only the real estate transaction process but also the local market dynamics that shape how deals come together, it can be a long, lonely, and costly process.

Not All FSBOs Are the Same, Except When They Are

There are some circumstances where a FSBO can make sense, for example in rural areas which make up 14% of FSBO sales compared with 3% in urban areas. Or, if the seller and buyer know each other like a neighbor or family member; 54% of eventual FSBO sellers knew their buyer.

But by and large, FSBO sellers found it difficult to reach the widest selection of qualified buyers and then manage the work that came once a buyer was interested. FSBO sellers must manage multiple methods to market their home through “word-of-mouth” to friends, relatives, and neighbors making up the majority (20%) of how properties are promoted and a yard sign running a close second (19%). Only 5% of FSBO properties were promoted on a Multiple Listing Service (MLS), meaning a huge number of buyers and their agents would likely never even know that FSBO property existed because site aggregators like Realtor.com, Zillow, or Homes.com pull listing data from MLS feeds.

For FSBO sellers lucky enough to land a buyer who found their needle-in-a-haystack property and then would agree to work with an unrepresented seller, that’s when the real work kicks in. NAR’s report showed that some of the most difficult tasks for FSBO sellers were:

- Getting the pricing right (15%)

- Understanding and completing/performing paperwork (7%)

- Selling within the planned length of time (7%)

- Helping buyers obtain financing (5%)

- Preparing/fixing up home for sale (4%)

- Attracting potential buyers (4%)

Why a Realtor® Matters

With so much stacked against FSBO sellers, why attempt to go it alone? The obvious answer for most FSBO sellers is that they want to save money by not paying a Realtor® fee. However, 75% of all sellers paid a fee to a Buyers’ Agent regardless of whether they used a listing agent to sell their home. So if a FSBO seller is likely paying commission fees while also receiving a lower sales price and carrying costs, the value of hiring a listing agent becomes a lot more clear.

One of the best tools an agent will share with their seller is a smart pricing strategy. Realtors® live and breathe local statistics and use them to tell a story, one that helps sellers understand where their home sits in comparison with other homes in the market. An agent’s pricing knowledge can be the difference between a property that goes under contract in a week and one that “tests the market” and sits unsold for a month or longer, costing the seller money in the long run.

The guidance a Realtor® provides can also ensure that oversights don’t become lawsuits. Agents use contracts, addenda and other sales paperwork that has been vetted by local Realtor® associations, allowing for clear understanding of terms and conditions. Realtors® are governed by NAR’s Code of Ethics and uphold the highest standards of conduct in working with clients, customers, and colleagues, ensuring that everyone is treated fairly and in the clients’ best interest.

But the most important role a Realtor® can play for their seller clients is to be a Trusted Advisor who understands the value of a home, both in market dollars and as a significant personal investment. Selling a home is a huge undertaking, both in the logistical and emotional sense, and it’s not easy to navigate a process with so many moving pieces. It’s also why many Realtors® refer to what they do as a “calling,” a deep satisfaction in helping others achieve their real estate goals and pride in building stronger communities with each new sale. It’s what they’re trained to do, it’s what they love to do.

Learn the lesson from many regretful FSBO sellers: to earn more money and have fewer headaches, consult a McEnearney Associates | Middleburg Real Estate | Atoka Properties Realtor® and let their expertise guide you to your next real estate adventure.

Take a look at our website for all of our listings available throughout Washington, D.C., Maryland, and Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

What Your Realtor® Wants You To Know About Fair Housing (Part 2)

Each April, Realtors® commemorate the passage of the Fair Housing Act of 1968 which provides protections against housing discrimination and segregation. Here’s Part 2 of a two-part overview of what consumers should understand about their rights and obligations under the law.

In its 2023 Fair Housing Report, the National Fair Housing Alliance reported that in 2022 there were more than 33,000 housing discrimination complaints, the highest number of complaints filed and an increase of nearly 6 percent over 2021. However, some estimate that could be only 1 percent of actual fair housing violations that occur.

Last week we looked at the history of the Fair Housing Act and those who are protected under federal, state, and local regulations, including race, color, religion, sex, national origin, familial status, and disability. This week we highlight some protected classes that housing providers may not know are covered under the Fair Housing Act, including some cases discussed at an education session for our Agents earlier in the month, led by Keith Barrett of Vesta Settlements.

Barrett noted that housing providers have to make individual decisions based on complex issues, creating questions about what qualifies as a protected class and complicating attempts to make those accommodations. Here are a few examples of emerging issues that Barrett cited as areas that housing providers should consider.

Service Animals and Assistance/Emotional Support Animals

- As defined under The Act, an assistance animal is an animal that works, provides assistance, or performs tasks for the benefit of a person with a disability, or that provides emotional support that alleviates one or more identified effects of a person’s disability. An assistance animal is not a pet and housing providers cannot refuse to make reasonable accommodations in “rules, policies, practices, or services when such accommodations may be necessary to afford a person with a disability the equal opportunity to use and enjoy a dwelling.” In short, rules such as a “No Pets” policy do not apply here.

- Service animals are categorized as animals trained to do a specific task for their owner (such as a guide dog) and are allowed in public accommodations because of the owner’s need for the animal at all times. Assistance animals need not be trained to perform a service and the emotional and/or physical benefits from the animal living in the home are what qualify the animal as an assistance animal. A letter from a medical doctor or therapist is all that is needed to classify the animal as an assistance or emotional support animal.

- Specific guidelines can be found here for DC, Maryland, Virginia, and West Virginia.

- Barrett shared two cases that involved violations of reasonable accommodation for service and support animals. In 2016’s Arnal v. Aspen View Condo Association, et al., the condo owner plaintiff alleged that his Colorado condominium association improperly denied a reasonable accommodation to its “no dogs” policy to allow his tenant to keep a service dog that assisted with her epilepsy, and that the association retaliated against him for allowing his tenant to keep the dog by issuing fines. In 2019’s Calvillo, et al. v Baywood Equities, L.P., et al., the plaintiffs alleged that the managers of California’s Baywood Apartments complex discriminated against the tenants on the basis of disability when they denied a request for an emotional support animal while also making intimidating statements. The defendants were judged to pay $32,500 to the plaintiffs, while also requiring the defendants to implement new policies, training, and reporting practices.

Source of Funds

- Under state Fair Housing laws in DC, Maryland, and Virginia, buyers or renters who receive assistance or subsidies for housing payments cannot be denied accommodations. This includes housing vouchers (sometimes referred to as Section 8 funds).

- Housing providers can still require a minimum income threshold to qualify to rent, but when calculating the minimum requirements the fund amount should not be added to a person’s income but rather deducted from the rent being charged.

- For example a prospective tenant wants to rent a property of $1,000, has an income of $800, and a housing choice voucher of $750. The landlord requires an income threshold of three times the rental amount to qualify to rent the property, or $3,000 (3 x $1,000). The correct calculation is to take the $750 amount and subtract it from the $1,000 rent, resulting in a $250 difference. Taking $250 x 3 = $750 as the minimum income threshold to qualify and the tenant meets that requirement with their income of $800.

Hoarding

- Hoarding is the excessive accumulation of items along with the inability to discard them even if they appear useless. It was qualified as a disability in 2013 when it was added to the Diagnostic and Statistical Manual (DSM) psychiatric diagnosis, offering protection under the Fair Housing Act.

- Housing providers must offer reasonable accommodation even if the resident doesn’t ask for an accommodation, admit to having a disability, or agree that the unit needs cleaning.

- Housing providers should instead set goals, create a plan with a defined timeline, and schedule follow-ups with the resident.

Former/Recovering Addict

- Addiction to alcohol and the illegal use of drugs are treated differently under the ADA. Alcohol addiction is generally considered a disability whether the use of alcohol is in the present or in the past. For people with an addiction to opioids and other drugs, the ADA only protects a person in recovery who is no longer engaging in the current illegal use of drugs.

- If a person is prescribed medication to treat a substance use disorder, the ADA and/or the Fair Housing Act may require housing programs to admit the individual. The ADA also requires that state-funded housing provide “reasonable modifications” to individuals with disabilities, including those in recovery.

It’s important to note that Realtors® are bound by professional ethics and have a higher standard of service to the public than their clients regarding Fair Housing requirements and will advise their clients on federal, state, and local laws regarding housing. If a Realtor® finds that a client or customer is violating Fair Housing laws they can decline to work with the housing provider and report them to appropriate authorities. Those who believe they have been impacted by or wish to report housing discrimination can file a complaint to the US Department of Housing and Urban Development (HUD), the National Fair Housing Alliance, and local governing authorities (DC, MD, VA, WV).

Barrett’s final advice for anyone involved in providing housing or a dwelling to the public: “Treat everyone fairly and consistently.”

For guidance on Fair Housing Rights and Requirements, consult a McEnearney Associates | Middleburg Real Estate | Atoka Properties Realtor® to help navigate your individual housing situations. We’re here to help!

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

What Your Realtor® Wants You To Know About Fair Housing (Part 1)

Each April, Realtors® commemorate the passage of the Fair Housing Act of 1968 which provides protections against housing discrimination and segregation. Here’s Part 1 of a two-part overview of what consumers should understand about their rights and obligations under the law.

Have you ever felt discriminated against or “othered” when trying to buy a home, rent an apartment, or even stay at a hotel? If so, you may have been a victim of a violation of the Fair Housing Act. But what qualifies as a violation and how can housing providers ensure that they are not making decisions to restrict housing of a potential resident or customer based on a protected class?

Keith Barrett, Attorney and Founder of Vesta Settlements, recently held an overview for our McEnearney | Middleburg Real Estate | Atoka Properties Associates about Fair Housing, specifically ways in which discrimination is still prevalent in real estate and dwelling transactions and how agents should conduct their business to avoid violations and educate their clients about the law.

“Every single person is protected by the Fair Housing Act even though its genesis came from protecting against racial discrimination,” Barrett shared.

Background on The Act

The Fair Housing Act was enacted in 1968 and amended in 1988 to “prohibit discrimination by direct providers of housing, such as landlords and real estate companies as well as other entities, such as municipalities, banks or other lending institutions, and homeowners insurance companies whose discriminatory practices make housing unavailable to persons of specific protected classes including: race, color, religion, sex, national origin, familial status and disability.” The Civil Rights Act of 1866 can also provide relief although its scope is limited to racial discrimination.

The Fair Housing Act covers most housing and in very limited circumstances the Act exempts “owner-occupied buildings with no more than four units, single-family houses sold or rented by the owner without the use of an agent, and housing operated by religious organizations and private clubs that limit occupancy to members.” In addition to homes, rental units, and land to be used for development, dwellings covered by Fair Housing may include nursing homes, hotels, dormitories, temporary migrant housing, and homeless shelters.

Federal laws provide the minimum level of protection while state and local governments can add further protections.

- DC’s Fair Housing protections include age, personal appearance, sexual orientation, gender identity or expression, family responsibilities, political affiliation, matriculation, source of income, place of residence or business, status as a victim of an intra-family offense, sealed eviction record, and homeless status.

- Maryland’s additional protected classes are marital status, sexual orientation, gender identity, and source of income.

- Virginia adds additional protections for elderliness (55+), source of funds, sexual orientation, gender identity, and military status.

- West Virginia’s additional protections include ancestry, age (40+), and blindness.

- Local jurisdictions within the DC-Metro area can include even more protections.

How The Act Combats Discrimination

“Overt discrimination is alive and well in the United States,” observed Barrett, citing several examples of cases of Fair Housing violations across a broad range of protected classes.

Barrett noted that following the law’s enactment most claims were about race, but currently, 53% of claims made were on the basis of disability, primarily in rentals. Many Fair Housing violations come from not making reasonable accommodations for persons with disabilities, which can cover a wide range of physical, mental, and psychological conditions and may not often be outwardly visible.

At every level, Realtors® work with their clients and communities to educate housing providers and empower consumers to understand their roles and responsibilities in adhering to Fair Housing guidelines. Read more about those initiatives at the National Associations of Realtors® (NAR).

In Part 2 next week, we’ll look at several Fair Housing categories and real-life scenarios that both housing providers and those seeking housing should be aware of to ensure equal treatment of all. For guidance on Fair Housing Rights and Requirements, consult a McEnearney Associates | Middleburg Real Estate | Atoka Properties Realtor® to help navigate your housing situations. We’re here to help!

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Where Have All The Listings Gone? And Are They Coming Back?!?

It is no secret that there is a national shortage of homes for sale on the market, and with a few exceptions, that dearth of inventory is especially acute in the metro Washington, DC* area.

This has been coming for a long time. The average inventory at the end of February over the decade from 2005 – 2015 was right at 10,000 homes. At the end of February 2019 – just before the onset of the COVID pandemic – there were 7,600 available homes, and at the end of February 2024, there were less than 4,000. When you realize that the population of our area has grown 39% (1.5 million people) since 2000, that’s a staggering drop. Put simply, there’s 60% less inventory today with 40% more people.

But why is this happening? There are lots of reasons, and most are long-lasting.

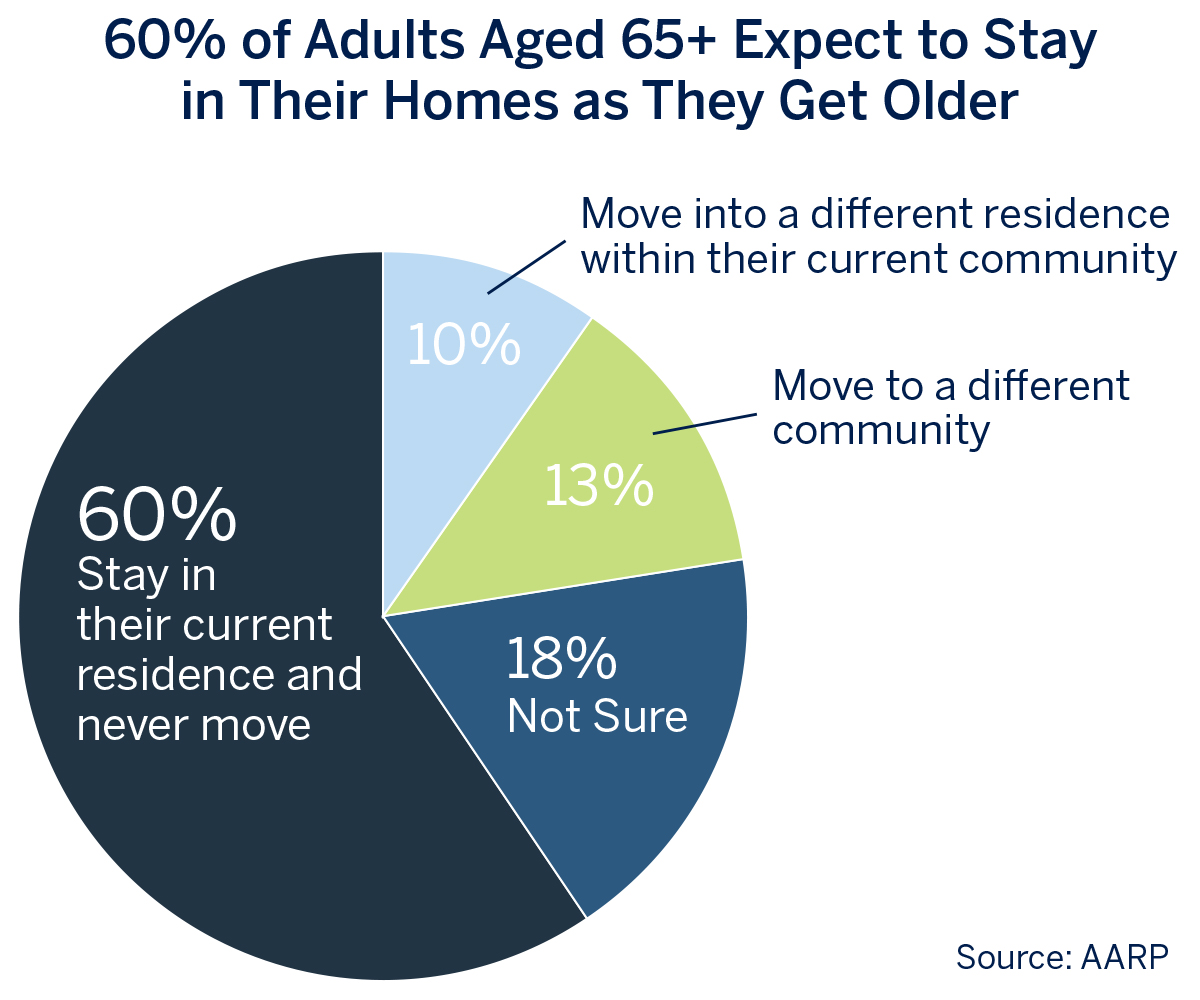

Demographics – and the Silver Tsunami that’s more like a ripple

People are staying in their homes much longer. The National Association of Realtors tracks “seller tenure,” the median length of time a seller has been in their home before they sell. For a generation that stayed steady at 7 years – and it’s now more than 12. And while the Silver Tsunami, the big jump in population of aging Baby Boomers is real, the impact thus far on real estate has been a ripple at best. A recent study by AARP indicates that 60% of adults aged 65 or older have no plans to move from their current home – ever. That’s a lot of inventory that isn’t going to come on the market anytime soon.

Interest Rates and Tax Policy

We’ve never seen a time of such rapid increases in mortgage interest rates following record- low rates. Roughly half of all homeowners have a current mortgage at a rate of 4% or less – and many have a sub-3% mortgage. Consider this basic example: a homeowner with a $500,000 mortgage at 3% has a monthly principal and interest payment of $2,108.02. If that same homeowner sells and buys something with a mortgage that is just 10% more – $550,000 – their new monthly payment at the current rate of 7% would be $3,659.16. That’s a 74% increase in the payment for just a 10% bigger loan, and many sellers understandably won’t make that switch. On top of that, those sellers – like aging Baby Boomers – who have owned their home for a long time might face a tax hit if their capital gain exceeds $500,000. All of that has locked a lot of would-be inventory off the market.

High Cost of Land – and the High Cost of Regulation

Our region has battled this for a long time, and it really restricts affordable new home construction. As intensely developed as the close-in areas of metro DC are, much of the new construction is in the outlying suburbs, and that may not be where people want to live. There have been studies that indicate as much as 25% of the cost of new construction is involved with planning and compliance with federal, local, and state regulations. That contributes to driving home prices higher, another hill to climb for current homeowners who might consider moving.

There’s Inventory – and There’s Inventory That People May Not Want

There isn’t enough inventory – except for condos and co-ops in Washington, DC. It’s another indication that there isn’t just one real estate market, and buyers really do care about what they buy even when they don’t have many choices. Through most of the last 20 years, the inventory of condos and co-ops on the market in DC constituted about 7% of all available homes. Now, it’s 25%. Much of that inventory is in older buildings with few amenities, and that’s not what today’s buyers are typically looking for. Time isn’t going to make those units better. So even in a time of scarce inventory, market dynamics still matter, and a buyers’ market can exist when almost everything else tilts in favor of sellers. Those condos and co-ops will still sell, but they will be on the market longer and won’t command the higher prices that other property types do.

What Happens From Here?

Markets adjust over time. There is pent-up demand from people who would really like to sell their home, and we will see the typical increase in inventory this spring. But that rebound will be muted until interest rates come down substantially, and that’s going to take a while. And the demographic pressures really aren’t going to change. Be prepared for an extended time of inventory that is insufficient to meet the demand – and that means continuing higher home prices.

We also hear theories that the upcoming elections will have a major impact on the region’s housing – watch for our next MarketWatch where we will dispel that myth.

*Data derived from BrightMLS for Northern Virginia (Fairfax and Arlington Counties and Alexandria, Fairfax and Falls Church Cities), Loudoun County, Prince William County (including Manassas City and Park), Washington, DC, Montgomery County and Prince George’s County.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Shocked By Spiking Home Insurance Rates? You’re Not Alone.

Massive increases in insurance premiums are busting budgets and derailing some home purchases.

If you’re a property owner, you know you need homeowner’s insurance. And if you live in an area that’s been designated as having a higher risk for property damage – such as in a flood zone, an area of extreme weather, or a densely-wooded location – you might expect that your insurance rates will be higher. And, of course, homeowners know that if they file a claim or two over the years that they should pay more at their next policy renewal.

But many homeowners and would-be buyers are finding out that premiums are rising sharply through no fault of their own, if insurance can be secured at all. What was once a standard, perfunctory item on a homeowner’s to-do list has become a lot more complicated as larger insurance companies try to stem losses caused by an increase in claims in areas affected by major natural disasters like wildfires, flooding, tornadoes, and hurricanes. Those costs are being passed down the line to consumers.

“It’s problematic for our buyers and problematic for our sellers,” said Jillian Keck Hogan is a top-producing agent who works in DC, Maryland and Virginia and has experienced how acquiring insurance can complicate a home sale. She recently represented a seller for a listing that the buyer couldn’t secure insurance for because there weren’t definitive records about the age of the roof. Multiple roof inspectors gave reports that insurance deemed inadequate because the roof, while in sound condition, was past its half-life expectancy.

Roofs can last around 30 years and the average life of most roofs is around 20 years. In order to secure their insurance and proceed with closing on time, the seller chose to split the cost of replacing the roof after closing. Jillian said that education for both buyers and sellers is key. She advises that sellers should gather details about the age of their roof, systems, and utilities before bringing their home to market and be prepared for buyers who may request fixes for big ticket items, while buyers should start shopping for insurance sooner rather than later, and to investigate multiple carriers for rates.

“It ends up being messy if you’re trying to get all of your insurance research done only days before closing,” she warned.

Susie Adib, Senior Producer with Commercial Insurance Associates, said there are many factors that are causing a spike in premiums – in many cases more than 20% – including an increase in severe weather and natural disasters, a carrier’s drive for profitability as set by their combined ratio, and complications from pandemic recovery, including inflation, labor shortages. Many things that are just now working through the insurance pipeline, a process that takes time because of regulatory review at the state level for any changes a carrier makes regarding premium increases. State agencies make sure there are sufficient and affordable options for consumers and local departments of insurance and their resources can be found here for DC, Maryland, Virginia and West Virginia.

Adib said that much like credit scores, homeowners will have an insurance score that affects how much a policy will cost. This can include factors like how many claims you’ve made in the past, your credit score, and who you’ve been insured with in the past. For example, there many companies that won’t insure a slate or flat roof, historic properties, or homes built before 1900 and if you’ve had a previous insurance carrier that covered those items in the past, it will be a flag to a new carrier that there is a mitigating factor in the property.

What happens if a property is deemed uninsurable? Adib said there are still options. Again, much like credit companies, there is a market for substandard properties where premiums will be higher but at least the home will be covered. There is also the option to exclude coverage for a portion of the home that is at higher risk, for example a roof or liability for a pet. Lenders can also require force-placed insurance, whereby the lender secures the insurance and passes along the costs to the borrower via steep premiums in their mortgage.

“When it comes to insurance, there are so many options,” Adib said. “It’s so important to have an actual person you can talk to – not an #800-number – especially when a claim arises.” She advises homeowners to do timely research to make sure you have that person to go to bat for you when the time comes.

Here are some tips for keeping insurance premiums in check.

- Review your insurance policy every couple of years, especially if you’ve made improvements or renovations to the property. Adib said that shopping for new coverage won’t increase your rate and it’s important to understand how different carriers might evaluate your policy and the premiums you pay. “It’s your policy so make sure it covers what you need it to.”

- Don’t make small claims. The average homeowner makes one claim every seven years and anything above that could impact policy rates. For example, don’t file a claim if you have a $500 deductible and a tree falls on your backyard shed accounting for $700 in damages. Yes, you have insurance for a reason but not all claims are equal. The more claims on a policy the more likely it is to face a surcharge or be at risk for non-renewal.

- Shop replacement costs of your home, which are different from the market value of your home which also includes the value of the land the property sits on. Replacement costs are the amount of money needed to repair a property or replace belongings at current building supply costs. Over time, automatic annual increases driven by roll-on percentages that are driven by inflation can increase expected replacement costs that may not be aligned with actual costs. If you’ve had your policy for a while, it’s worth looking at the suggested replacement costs and see how they compare with other policy quotes. It’s important to note that while a carrier’s premium rates are reviewed and regulated by the state, roll-on percentages for replacement costs are not, even though high replacement costs can increase the premium. A home with a current replacement cost of $500,000 with an annual roll-on percentage of 3% is going to have a lower premium over time than a similar home with a roll-on rate of 6%. “You could be paying a lot more in premiums for coverage you might not need,” Adib said.

- A higher deductible can lower insurance rates, especially if you don’t have a lot of claims on the policy. Owners like low deductibles because they want to reduce how much they must pay out-of-pocket for damages to their property, but lower deductibles mean higher premiums, and deductibles only come into play when a claim is made. Over time, having a $2,500 deductible and a lower annual premium will save more money than having a $500 deductible and a higher premium. Another option is a percentage deductible, but Adib cautions that while this can lower premiums it will mean more money out of pocket if there is a claim.

- Maintain your home in good condition. Look for trees around the property that could cause damage, check the roof for missing shingles or areas of leakage or water absorption, keep up with maintenance on big-ticket appliances like the HVAC and hot water heater. Insurance carriers do conduct inspections on properties they cover – including using spatial imaging to evaluate roofs – and your rates could increase if they find something of concern.

- Consider a local carrier. National carriers have increased volatility in their rates because they cover the entire country, including areas that may be prone to natural disasters. To make up for losses in those areas they must be strategic about rates and be selective about the risk they will accept with new policies, while smaller and local carriers may be willing to take on that risk.

If you’re a current homeowner, take a few moments to review your current policy to check you have the coverage you need on terms that work for you now, as circumstances are likely to have changed if you’ve owned that property for a while. If you’re a buyer looking to secure coverage, pay attention to the condition of the property you’re purchasing and be prepared to negotiate with the seller to make fixes or shop around for an affordable policy.

Your trusted McEnearney | Middleburg Real Estate | Atoka Properties Associate can connect you with recommended insurance professionals who can explain options and help you find a policy that fits your needs and a rate that won’t break the bank.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

NAR’s Settlement, What’s not being said

Here’s what’s not being published: why consumers choose to pay us.

Salacious headlines that imply consumers have been duped into overpaying (the same fee) are wrong. That would assume we’re all the same. Also – wrong. Who you hire matters. I don’t care if it’s your hair or your house. Results vary and will depend on who you hire.

Consumers are smart.

Their decisions are the result of a balanced risk assessment.

Let’s use your lawn as another example. Let’s say a foreign species has taken over and is growing at a ridiculous rate. If consumers want to mow it down, they’ll likely do it themselves. If they want a treatment program that actually eradicates the weed, my bet is that they understand it may take more time, effort, and money.

You’re probably thinking, “Yeah—but those are simple things. Buying or selling real property is different.”

Exactly.

Buying and selling real property isn’t straightforward, simple, or low stakes. To propagate any other idea is misleading and harmful.

Why?

Because they know they shouldn’t do a big thing badly, and they know buying or selling is a big thing. It has real and impactful consequences, and there are nuances to their move.

As with any profession, skills matter.

The average consumer intuitively knows this – and they’re willing to pay the right professional.

The proposed settlement will reinforce what is already the best real estate system in the world and the pros who operate within it. To somehow infer otherwise is shortsighted and doesn’t give the consumer much credit.

If approved, NAR’s settlement would change some operational infrastructure and ensure clear communication and education between realtors and their clients.

This settlement isn’t about paying highly skilled realtors. They’re worth it, and don’t be fooled. Consumers know it.

Sandy McMaster, a licensed real estate agent with McEnearney Associates. For over a decade, Sandy has helped hundreds of people in Alexandria and the DC area successfully navigate the changes and reduce the uncertainty that can easily become overwhelming. This experience allows her to see around corners and anticipate roadblocks. When working with Sandy, it will allow you to move quickly, with confidence and the knowledge that, no matter what happens, she’s got you.

Take a look Sandy’s website for all of her listings available throughout Virginia and Washington, D.C.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

The Pros & Cons of Financing and Appraisal Contingencies

In the immortal words of “The Gambler,” you gotta know when to hold ‘em and know when to fold ‘em in the high-stakes world of real estate negotiations.

It’s not always the offered price of a home that catches a seller’s attention; it could also be how quickly a contract can move to the settlement table. Factors like contingencies – addenda that allow a contract to be voided under certain specified conditions – are an important consideration for both buyers and sellers.

For most sellers, the fewer contingencies in an offer, the better. Every contingency comes with deadlines and terms that must be met and there’s potential for a contract to be delayed or derailed if the buyer doesn’t meet those terms. The reality of the current housing market is that many buyers are waiving their contingencies to appeal to a seller, including two of the most popular contingencies: Financing and Appraisal. But what happens when things go sideways and a buyer encounters trouble financing their loan or the home doesn’t appraise for the ratified contract sales price?

Brian Bonnet, SVP & Senior Loan Officer (NMLS ID 224811) for Atlantic Coast Mortgage, recently spoke with many of our Associates to run through different scenarios that buyers may encounter when using or waiving Financing and Appraisal Contingencies. While he noted that most of the contracts Atlantic Coast Mortgage is seeing have been ratified without a Financing or Appraisal contingency, there are situations where a qualified buyer should be hesitant to waive one or both of these contingencies.

What do these Contingencies do?

The Financing and Appraisal contingencies serve to protect a buyer during the real estate transaction. They are included in an offer that requires the buyer to “perform” according to the terms outlined in the contingency or risk defaulting on a ratified contract. If a buyer is not approved by the lender for their proposed financing, the Financing Contingency gives the buyer the option to cancel the contract without penalty (if they cancel within the terms of the appropriate Contingency Addendum). If a property’s appraised value – an amount that is determined by a licensed appraiser on behalf of the lending institution – doesn’t meet the contract sales price, a buyer has the option to void the contract if the seller doesn’t lower the contract sales price to the appraised value or doesn’t meet the lender’s standards required for the condition of the property.

These contingencies are available to conventional, FHA, and VA buyers while the latter two types of transactions may have additional restrictions on how they are used.

When might a Buyer waive the Financing Contingency?

If a buyer is considering waiving the Financing Contingency, beware of the pitfalls. “It is critically important that their financing is rock solid before they choose to remove that contingency,” Bonnet stressed. He recounted a recent experience with a buyer whose long-time work visa had expired and he therefore wasn’t able to continue at his current job until the visa had been renewed. Because the buyer had a Financing Contingency in place, the contract was voided. Had the contingency not been in place, the buyer could have been subject to losing their earnest money deposit (EMD) or other damages should the seller have elected to sue for defaulting on the contract.

When a Financing Contingency is put in motion, the lender will begin a “canceled, withdrawn, or denied” process and an Adverse Action Letter, also called a Rejection Letter, outlining generic terms of why the financing was denied which is then sent immediately to all parties of the contract. This will be followed up by the buyer’s agent with the required paperwork to void the contract, release the buyer from further obligations, and allow the seller to put the property back on the market.

A buyer may elect to waive this contingency if they are certain their employment is secure, are confident that their financial situation won’t change before settlement, or they are putting down a substantial downpayment that reduces the amount of their loan.

When might a Buyer waive the Appraisal Contingency?

An Appraisal is ordered by the lender to verify that a property is worth the amount of money that is being lent to purchase the property. For example, if a home is under contract for $500,000 the lender will want to see an appraisal value of $500,000 or greater. If there is an appraisal gap between the contract sales price and the appraised value, an Appraisal Contingency will spell out what happens next: the seller can agree to lower the sales price to the appraised value; the buyer and seller can renegotiate the sales price and the buyer can add additional cash to their offer to make up the difference; or the buyer can void the contract. In the absence of an Appraisal Contingency, the buyer is obligated to bring additional cash to make up the full difference in the appraisal gap.

A buyer may waive this contingency if they have a good cash reserve and can make up the difference without the cash outlay affecting the lending underwriting. Another scenario might be when a property is in an area where there is potential for value growth. Even if the appraisal comes in low, a buyer may elect to make up the cash difference because they are predicting that a property’s equity may grow quickly.

What can Buyers do?

- Work with a respected, local lender who will advise buyers honestly and clearly on their individual financial risk. Local lenders have a better understanding of regional market dynamics and can speak to factors that can affect the transaction better than most national lenders who don’t have ready access to local information.

- Ensure that when waiving an Appraisal Contingency, the contract specifies that an appraiser will still have access to the property. Many loans may not be approved without an appraisal, regardless of whether a buyer makes the appraisal a contingency to purchase.

- Consider the condition of the home before waiving an Appraisal Contingency. Even if the market value of the home is determined to be adequate, a lender may not approve a property deemed uninhabitable. Bonnet notes that while the “vast majority of homes meet (habitability) standards, you don’t want to be the lone property that doesn’t.”

Overall, Bonnet advises borrowers to go into any real estate transaction with “eyes wide open to make an informed decision.” Enlist a respected, local lender and an experienced McEnearney | Middleburg Real Estate | Atoka Properties Associate to be the team that helps you land your next property!

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()