Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Use Your Tax Refund Toward Homebuying Costs

For many, it’s a once a year windfall. Check out the best ways to make your tax refund work for you.

Tax season is right around the corner, and if you’re expecting a sizeable tax refund and want to invest in your homeownership future, here’s something you might not have considered: using your tax refund to buy your home. You’d be surprised at the creative ways you can utilize your tax refund for home buying success, so let’s review some options.

Your Down Payment

One of the first avenues you can funnel your tax refund to is towards your down payment. While it likely won’t be enough to cover the full down payment, you can combine it with CMG’s HomeFundIt™ program, a down payment gifting platform that allows you to raise funds from your community. HomeFundIt also guarantees a $2,000 matching grant to first-time home buyers.* If paired with your tax refund, you’ll have a healthy amount to put towards your home purchase.

Closing Costs

Various fees and expenses the borrower pays at closing can typically range from 2-5% of the total purchase price of the house. Some buyers forget that there is more to starting a mortgage than just covering the down payment. Closing costs are also split by both the buyer and seller, and your tax refund can significantly help cover those costs.

Emergency Funds

An emergency fund is an excellent option for your tax refund, especially if you’ve already covered the down payment and closing costs.

Unexpected expenses go hand-in-hand with being a homeowner, and if a plumbing issue or environmental damage happens to your home right off the bat, it will be a huge weight off your shoulders if that emergency money is ready to go.

Moving Costs

Whether it’s renting a U-Haul or hiring movers, there are extra fees to consider when making the big move once all loan documents have been signed off. Not only will you need to pay to move, but there could be deposits required for utilities, extra storage, or paying for new furniture and household items.

Next Steps

It can be tempting to use a cash windfall for a “treat” like vacations, travel expenditures, a shopping spree and the like. However, if you’re a hopeful homeowner, it may be a better idea to invest in your future and start building equity sooner rather than later. Whether you funnel your refund towards your down payment, closing costs, emergency funds, or other costs associated with moving into a new home, you won’t regret planning ahead and setting yourself up for success.

Reach out to our CMG financial advisors today for more tips on preparing yourself for homeownership.

*Grant is a $2-to-$1 match on regular down payment gifts received on HomeFundIt™, up to the lesser of $2,000 or 1% of purchase price for first-time buyers, as defined by Fannie Mae, who complete home buyer education prior to signing a purchase contract. Talk to your loan officer or visit your HomeFundIt dashboard for next steps, or you can also find a housing counselor near you by visiting https://www.hud.gov/counseling.

Grant funds are applied to nonrecurring closing costs. If closing costs are fully paid by seller or interested party, grant funds can be used to buy down the rate. Grant funds cannot be used towards a down payment. Visit https://www.homefundit.com/Grant for complete terms and conditions.

Brian W. Kempf

Senior Vice President, Branch Manager, NMLS ID# 483525

CMG Home Loans, NMLS ID# 1820

571-309-4911

Notice: This is an advertisement and is not a commitment to lend. Contact a loan officer today to explore the financing options specific to each borrower.

Home Purchase 411: The Top Five Things You Might Not Know

In homebuying, what you don’t know can indeed hurt you in the long run.

If you’re in the market for a new home you may be pondering many things: Will I get the best interest rate? What will my commute to work be like? What can we do with the basement? Will the primary bedroom closet fit all my clothes? Is there a cul-de-sac for the kids to play? Will I be able to afford the loan payment?

All important considerations, no doubt. But there are some not-so-obvious aspects of buying a home – one of largest, most important, and expensive transactions most people will undertake – that buyers should consider to minimize risk for what should be a happy and positive life milestone.

Keith Barrett, an attorney and founder of Vesta Settlements, recently met with many of our agents to discuss his Top Five things that buyers should be aware of.

Title Insurance

Title is the formal right of ownership of property; title insurance protects and insures an owner’s (or lender’s) interest in real property. Specifically, it is a policy of indemnification (“making whole”) against loss caused by any covered defect in the title. Title insurance is unique in its scope because where most insurance policies protect against future unknown events, title insurance is retrospective and looks back in history (generally back 40 years) at what has occurred to land or a property regarding ownership. It’s also unique in that the premium is paid once, rather than monthly or annual premiums like other insurance policies.

Why is this important? Title insurance protects a seller for the rest of their life because seller’s maintain liability related to the warranty they provide in the deed of conveyance.. As a result, the title policy protects the seller even after the property has sold … for all eternity! And even though you should permanently retain all title insurance documents, don’t worry if you happen to lose the physical copy of your title insurance as there will likely be a record at one the largest four title insurance companies.

There are two types of title policies: an optional Owner’s Policy (protects the homebuyer for life, with a one-time premium based on the purchase price) and a required Lender’s Policy (protects the lender until the loan is paid off, with a one-time premium based on the loan amount). And although title insurance is optional, it’s an expensive gamble to skip it. Barrett advises buyers ask themselves, “Am I willing to self-insure here?”

He used an example of the “extended warranties” that are pitched when buying appliances. If a $100 printer breaks down and you don’t have a warranty, it’s not that big a hit to buy another printer and be out a couple of hundred dollars. But when you’re looking at a $900,000 home for which you’ve put down a hefty downpayment of $100-200K, is that something you want to be on the hook for if a title claim arises.?

(Here’s an interesting bit of local history related to deeds: Barrett shared that most of our region’s land and property records were destroyed during the Civil War, but Loudoun County clerks had time to collect their records and hide them in various places throughout Virginia. This means Loudoun County still has their original records from more than 200 years ago! Worth taking a visit to tour this local bit of national history.)

Caveat Emptor…Buyer Beware!

If you’re a buyer in Virginia, the onus is on you to do your due diligence before purchasing a home to ensure the property is of suitable type and condition. While Virginia law requires a seller to provide a Residential Property Disclosure, it’s really a disclaimer statement and not a disclosure. A seller makes no representation to the buyer as to the condition of the property, adjacent parcels, covenants, or restrictions. Generally a seller will only be liable in the event actions were taken to conceal a condition or evidence of other fraudulent activities.

Why is this important?

Buyers might assume that sellers have a legal obligation to tell them about problems in a home, but in reality, in Virginia a seller doesn’t have an obligation to disclose known material adverse facts about the property and it’s up to the buyer to conduct inspections and seek out information. By law, agents are held to a higher standard for disclosure than their seller clients. Barrett offered an example of how disclosure works, such as a broken washing machine, by answering these five questions:

- Is it material to a buyer?

- Is it a fact?

- Is it adverse?

- Is it regarding the physical condition of the property?

- Does the agent have actual knowledge of this?

Surveys

Imagine you are walking the backyard of a property and you see a traditional white-picket fence. You might assume that everything inside the fence is part of the property and everything outside the fence is not. But without a survey, you have no actual knowledge of where a property line actually falls.

A survey is a physical depiction of the property including boundary lines and other characteristics such as patios, sheds, decks, driveways, fences, setback lines and, possibly, easements. In the example above, a survey could reveal that the fence was in fact built on the neighbor’s property and, therefore, certain property inside the fenceline is not actually the property.

Why is this important? Conducting a property survey is not required by lenders, but that doesn’t mean buyers should skip one. Through the American Land Title Association, lenders receive survey coverage in their final title policies whether the buyer gets a survey or not. But the lender’s coverage does not cover a buyer.

Barrett joked that, despite the great expense and work that it takes to buy a home in our region, “Sometimes I feel like people do more due diligence buying a smartphone than they do buying an $800,000 or $900,000 home.” He shared that the average cost of a survey runs around $350, a mere pittance when thinking about the consequences of having to move a driveway or a shed because it fell a few feet into over a boundary line.

Taking Title

When two or more people take title to property, a tenancy will have to be selected from one of these three options:

- Tenancy by the Entirety – reserved for married couples only. Includes rights of survivorship and basic asset protection to the extent the creditors of only one spouse cannot lien the property under this tenancy.

- Joint Tenants – with this tenancy, each tenant holds equal undivided shares in the property. Includes rights of survivorship.

- Tenants in Common – each tenant holds a proportionate undivided interest in the property, but it does not have to be equal shares. (Note that this is the default tenancy in Virginia.)

Why is this important? If you’re single or married, there’s very little to decide about tenancy. But when you have more than one buyer and they are not married it can have significant consequences down the road if the parties don’t understand how each tenancy plays out and how the home as an asset might be divided or protected in the case of a claim against assets (ex: creditors).

Home Inspections

As we saw above in “Caveat Emptor,” buyers need to do their homework about the state and condition of the property to uncover any issues. But most buyers don’t know what to look for when it comes to major systems like electrical, HVAC, plumbing, roofing, and foundations.

Why is this important? Without knowing the condition of a property, a buyer could get a nasty surprise when something major fails. Even in a competitive market, it’s critical to bring in an expert home inspector to do a thorough review of the home, looking at the age and condition of major systems and look for future issues that could arise. If a buyer wants to make an offer without including a home inspection contingency, ask to conduct a pre-offer inspection. That way the buyer is informed what may need to be updated, repaired, or replaced and can move forward with an offer or move onto a different property.

While homebuyers have a lot to worry about, these five areas are not normally top of mind. But giving these topics more thought and consideration will reduce headaches later. To make sure you’re working with an agent who will ask the out-of-the-ordinary questions to ensure you are informed about tricky subjects, reach out to any of our experts at Corcoran McEnearney to help keep trouble at bay.

Take a look at our website for all of our listings available throughout Washington, D.C., Maryland, and Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Why Pricing Matters, Even In a Hot Seller’s Market

Every seller thinks their home is The Best Listing. But the most successful sellers have a plan to make their property stand out to buyers.

The winter holidays aren’t known for frantic selling of real estate, especially when homes to buy are few and far between and buyers are focused on spending their dollars elsewhere. And stubborn interest rates that refuse to move below 7% is keeping a lot of people on the sidelines. But as we prepare for what’s new in 2025, it’s smart to look to last month’s statistics for clues as to what savvy home sellers can do to be ready… and where buyers should be focused.

There has been a significant pullback on the overall relationship of sales price to original list price, and the average days on market has increased as well. Nonetheless, overall housing supply in almost all of the 17+ jurisdictions we track is still less than 2 months, an indication of a strong seller’s market; a balanced market is when there is a 5- to 6-month supply of housing inventory.

(The notable exceptions are: Washington, DC, where overall supply reached 5.5 months, and all three property types – detached, townhome & condominium – exceed 4 months, and Baltimore City, where supply is 2.9 months.)

A modest easing of the market isn’t new and we’ve watched this trend for several months. What it tells us is that sellers who ”get it right” still sell quickly at a substantial premium. And despite this move toward a slightly more balanced market, there is still a significant gap between “Very Successful Sellers” and all the other sellers. Let’s take a look at their advantages.

The Difference Between Immediate Success and an Eventual Sale

The “Very Successful Sellers” are those who sold at or above original list price. In DC in December, 35% of all homes going to settlement sold above original list price – a 1.9% premium above list. And they sold in an average of just 39 days.

Contrast that with the “Eventually Successful Sellers,” who sold below original list price. That was 65% of all homes settling in DC in December and they took a big haircut, selling for an average of 12.1% below original list and with an average of 103 days to sell. That’s a lot of money and a lot of time those sellers lost by not pricing their homes correctly at the outset.

Pity the “Hopeful Sellers” – those whose homes are still on the market, waiting for offers — who have been on the market for an average of 122 days.

Let’s look at some other regional stats:

- In Montgomery County, half of the properties that settled sold at an average of +2% above original list in an average of 19 days. The other half of properties sold at just 94% of original list in 53 days. The average days on market for those homes that are unsold is 79.

- In Alexandria, 36.6% of homes sold in 18 days at an average +1.8% above list price, while 63.4% of homes sold at an average of -4.4% below list price and took nearly 52 days to sell, just beating out those still unsold at 58 days on market.

- Arlington & Falls Church sales averaged almost 45 days on market, with 43% of very successful sellers finding buyers within 13.5 days and for +2.4% above list, compared to 57% of eventually successful sellers who took almost 70 days to sell and -5.1% below list price. Hopeful sellers languished at nearly 90 days unsold, one of the highest of all the areas we surveyed.

- In Fairfax County & Fairfax City, successful sellers made up more than half of all sales – 53.6% – with a healthy +2.1% above list price and under contract in 13 days. The remaining 46.4% of eventual sellers sold at almost -6% below list and it took nearly two months to get there. The hopeful sellers are hanging on for nearly 74 days.

- Prince William County has one of the tightest markets for inventory, with just a 0.9 month’s supply of available properties. The most successful sellers saw +1.4% over list price and went under contract in 16.7 days. Eventual sellers got there in 51 days but at -4.8% below list price. If there’s a glimmer of hope for those unsold properties, it’s that they had the lowest days on market of the regions we surveyed, at 49 days unsold.

- In Prince Georges County, 53.6% sellers sold at +1.4% above list in 21 days, while the remaining sellers netted -5.7% below list and it took just over two months to sell. Unsold homes have been on the market for and average of 65.6 days.

- Big round of applause for Loudoun County most successful sellers, 56.5% of whom took just 9 days to sell and got +1.2% above list. The eventual sellers took 44 days with a -4.7% under list price, while unsold homes remained on the market for 71 days.

- The Virginia Countryside’s most successful sellers saw the closest list/sale price of +0.6% in 17 days, but they were just 38.5% of all sales. The remaining 61.5% of sellers took 70.5 days to sell at a lackluster -8.1% below list price. That’s making it tough for the “hopeful” sellers who take 2nd place to DC in remaining days on market at 94.9 days.

- West Virginia rounds out our regional look with a 2.3 month supply of inventory. This was also the most evenly divided of statistical insight: successful sellers made up 50.3% of sales at +0.5 above list in 44 days while eventual sellers made up 49.7% of sales netting -6.3% below list price over two months on market. Hopeful sellers have been on the market for nearly three months.

Plan for Success

What can a seller do to ensure they land in the “Highly Successful” camp? The first step is to work with a licensed Realtor® who will provide local market insight and guide your pricing strategy. The second is to prepare your home to attract the most qualified buyers: fix, remodel, and paint for the best first impression, and consider offering credits for buyers.

Finally, have a plan to make a pricing adjustment if the home hasn’t sold within 21 days, which appears to be the local “tipping point” when sales prices drop. Most experts agree that a listing that is 30 days on market without an offer is likely 3-5% overpriced. Be ready to make a pricing decision that keeps you within a competitive time-and-pricing window that keeps buyers interested.

As we have noted before, there are still buyers actively engaged in the market, but they make their decisions based on value. And they don’t see value in an overpriced home. So, heed the warnings of three out of four kinds of sellers who learned the hard way: price matters and time kills.

Read more housing analysis in our Market in a Minute and Weekly Meter and connect with one of our agents to find the best strategy to very successfully sell your home!

Take a look at our website for all of our listings available throughout Washington, D.C., Maryland, and Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Why Mortgage Rates Aren’t Dropping

The Fed lowered the Fed Funds Rate last fall but mortgage rates have increased. Why?

The Federal Reserve began lowering the Fed Funds Rate this past September with a ½ point decrease, followed by additional ¼ point reductions in November and December. Consumers had eagerly awaited these reductions in the hope that rates on consumer loans, such as mortgages, would follow.

Unfortunately, the opposite has been the case.

According to Freddie Mac’s weekly mortgage rate survey, the average rate on 30-year fixed-rate loans closed during the week of the September Fed rate cut was 6.08%. The survey shows the average rate increasing in the following months with that number currently sitting at 7.04%. So, with a total decrease in the Fed Funds rate of 1.0%, mortgage interest rates have actually increased 1.0%. Why?

Mortgage rates generally track the direction of the 10-year Treasury Yield. The 10-year yield and the yields of other long-term treasuries and bonds are driven largely by expectations of where short-term interest rates will be in the future, as opposed to where they are now.

The Federal Reserve lowered the extremely short-term interest rate, the Fed Funds Rate, but economic reports and even commentary from Federal Reserve governors continues to indicate concerns that instead of moving closer to the Fed’s 2% inflation target, we are actually moving away from it.

In addition to the actual economic numbers we are currently seeing, we have the prospect of tariffs being added to the mix, the result of which would very likely be inflationary. Fed commentary suggests they are less likely to continue lowering the Fed Funds Rate in the near term which has the impact of keeping long term yields, including mortgage rates at higher levels.

No one can tell consumers when mortgage rates will trend lower again, but waiting for lower rates before purchasing a home may not be the wisest financial move. The median price for a home in the DC Metro area rose approximately 6.2% in 2024 to $610,000. We continue to see low inventory and will likely see similar increases in home prices during 2025. As prices increase, so do loan amounts. Consumers should remember when rates decline, you can refinance a loan to a lower rate, but you can never “refinance” your purchase price to a lower price.

Let’s look at an example: a $610,000 purchase price now with 20% down at a rate of 7% results in a principal and interest payment of $3,247 on a loan of $488,000. Refinancing the balance a year later to a 6% rate reduces the P&I payment to $2,896.

But if a consumer waits that same year for rates to drop to 6%, the price of that same home will likely be $647,820, an increase of almost $40,000. With 20% down the loan would increase to $518,256 which results in a P&I payment of $3,107, or just $140 less than the previous year.

So while the purchaser saved $140/month in their P&I payment in the second example by waiting to purchase until rates dropped the next year, they could have saved $351/month by refinancing the loan if they had purchased the year before. Waiting for rates to decrease while home prices increase almost never makes sense.

If you’re in the market to purchase a home, we’d love to create a home-buying strategy that gets you a rate you can live with for a home you can afford today. Please reach out to me or my colleagues at Atlantic Coast Mortgage to get started.

Brian Bonnet

SVP, Sr. Loan Officer, NMLS: 224811

Atlantic Coast Mortgage, NMLS: 643114

O: (703) 766-6702 | M: (703) 304-0188

Notice: This is an advertisement and is not a commitment to lend. Contact a loan officer today to explore the financing options specific to each borrower.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

The Importance of an Emergency Fund When Planning on Buying a Home

By Bill Stern, Branch Manager for CMG Home Loans

Saving for your home doesn’t end with a down payment.

If you’re looking to buy a home, do you have an emergency fund? If you’re like many prospective first-time home buyers, this question may have sent a chill of anxiety down your spine.

You’re not alone. This is a big financial regret for many, but especially for Gen Zers and Millennials, who, according to CNBC, feel “not saving enough for emergencies ranks at the top of their lists.”

But don’t worry! We’re here to provide you with helpful information about emergency funds and calm any homeowning anxieties you may have, ensuring that your homeownership journey is a successful one.

A Safety Net for the Unexpected

It’s not just good to be prepared for the worst, it’s essential. What if you’ve just moved into your house using all of your savings, only for a tree to smash through your roof a week later — how can you afford the repairs? An emergency fund is exactly what you need in these unpredictable, money-leeching scenarios. Your back-up savings account is the bread and butter of happy homeownership, like a friend you can always count on in an emergency.

Other New Home Repair Woes

Aside from a tree crashing on your roof, the unexpected “joys” of homeownership can have a funny habit of making themselves known within the first few months of moving into your dream home. The furnace might be on its last leg and you might’ve moved in right before winter. Or you may have to deal with a closet collapsing, a leaking garage roof, water damage in your crawlspace, a malfunctioning defrost tube in your fridge, or perhaps your water stops working in general, leading you to fully replace your well pump and pressure tank.

If you’re not a handy person, you’ll pay a sizeable amount to professionals to patch together the home you just spent a big down payment to buy. An emergency fund can help assuage your anxieties and take care of these unforeseen circumstances.

Offset Income Loss or Unemployment

Career changes and unexpected unemployment are an unfortunate possibility. Whether it’s a reduction in your work hours or a companywide lay-off, an emergency fund can serve as another type of safety net. You’ll want to save enough money to cover your monthly mortgage payments and other household essentials.

How Much Should I Save?

This general rule of thumb suggests 3-6 months of basic living expenses to set aside. However, once you hit that goal, don’t stop setting aside money. Keep contributing a set amount from each paycheck every month just in case. Our loan professionals can help customize your own emergency fund strategy by evaluating your income and lifestyle so that you have a better understanding of how much is enough for your unique situation. You can jumpstart the process by setting a household budget, which doesn’t have to be overly complicated; here’s one from Nerd Wallet that works for nearly every type of household at any income level.

Avoid High-Interest Debt

Because many don’t have an emergency fund before they become homeowners, people often have to turn to high-interest credit cards to cover those unexpected costs. Having your safety cushion means that you don’t have to accumulate high-interest fees and can avoid a nasty cycle of debt, keeping both your credit score and financial health intact.

Set Realistic Goals

The idea of starting an emergency fund may seem daunting, but it doesn’t have to be. You can start small and set realistic savings goals, increasing these goals as you achieve them. You can easily set up automatic transfers from your checking account to your savings account. It’s all about making saving money a habit.

It’s important that you move into your new home with a solid financial foundation and a boosted peace of mind. Reach out to our CMG financial advisors today for more tips on preparing yourself for homeownership and setting yourself up for success.

Bill Stern, Branch Manager | NMLS ID# 267577

CMG Home Loans | NMLS ID# 1820

540-222-0164 | Website | Email Me

Notice: This is an advertisement and is not a commitment to lend. Contact a loan officer today to explore the financing options specific to each borrower.

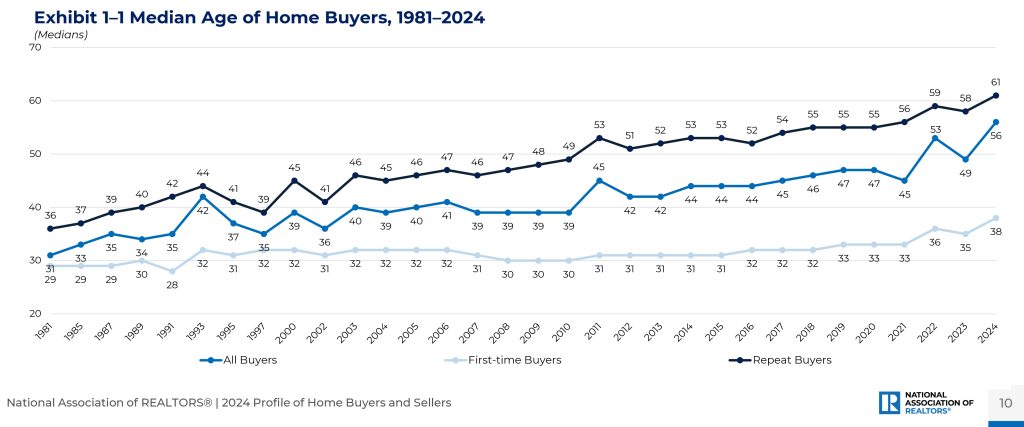

What NAR’s Report Says About Buyers & Sellers

It’s not just interest rates that are rising, so are the ages of home buyers and sellers.

Each fall the National Association of Realtors® (NAR) releases a comprehensive report on the demographics of real estate clients and compiles research on sales activities. This year, one of the most talked about trends was the rising age of buyers and sellers and a decrease in first-time homebuyers.

The first-time homebuyer market share dropped to a historic low of 24%, down from 32% last year, while buyers’ ages hit record highs. The median buyer age rose to 56 years (from 49), 38 for first-time buyers (up from 35), and 61 for repeat buyers (previously 58). By comparison, in 2002 the median age of first-time buyers was 31 and repeat buyers was 41.

Jessica Lautz, NAR’s deputy chief economist, noted, “The U.S. housing market is split: first-time buyers face high prices, high mortgage rates, and limited inventory, making them older and wealthier than previous generations, while current homeowners are using their equity for cash purchases or large down payments.”

Statistics were drawn from transactions that happened between July 2023 and June 2024 and included overviews of salaries, ethnic make-up, and marital status. Findings include:

- The median household income of buyers rose to $108,800 from $107,000 in 2022.

- First-time buyers had a median income of $97,000, a $26,000 increase over two years, while repeat buyers saw their incomes rise to $114,300 from $111,700.

- Among all buyers, 62% were married couples, up slightly, while single females increased to 20%.

- Single males and unmarried couples decreased by 8% and 6%, respectively, while single female first-time buyers increased by 5%.

- 73% of buyers reported no children under 18 in the home, the highest yet recorded.

- 83% of buyers were White, 7% were Black, 6% were Hispanic/Latino, 4% were Asian or Pacific Islander, and 3% were other ethnicities.

Multigenerational homes comprised 17% of purchases, the highest in the series. Lautz explained that rising costs have influenced buyers to “double up as families,” with young adults returning home due to prohibitive housing costs and elderly relatives moving in as families focus on close-knit support.

On the seller side, the typical age of home sellers reached the highest ever recorded at 63 years. The share of married couples selling their homes increased for the first time in four years, climbing from 65% last year to 69%. The most cited reasons for selling were the desire to move closer to friends and family (23%), the home was too small (12%), the home was too large (11%), and the neighborhood becoming less desirable (10%).

Other interesting takeaways from the report:

- The Price Is Right: Most sellers got 100% of their asking price, the highest median since 2002. But prices were lower for homes that stayed on the market for five to eight weeks and sold for slightly less at 98% of list price.

- Moving Into the Golden Years: Senior-related housing remained at 19% of buyers over the age of 60 this year; 58% purchased a detached single-family home, and 52% bought in a suburb or subdivision.

- Military Stats: 16% of recent home buyers were veterans and 2% were active-duty service members.

- FSBOs struggled: For-sale-by-owner listings, which represented a record low of 6% of all sales, typically fetched a lower sale price than homes represented by an agent with a median price of $380,000, far lower than the median selling price of all homes, which was $435,000.

- Price reductions uncommon: Even though price reductions were on the rise in 2024 compared to the pandemic years, the majority of sellers did not need to lower their sale price to close the deal: 65% never reduced the asking price, and 21% reduced it once.

- Sellers call the shots, usually: Because sellers largely retained the advantage in the housing market last year, just 24% (down from 33% last year) offered incentives to buyers; 76% of sellers offered no incentives, 9% provided assistance with closing costs, and 8% offered a home warranty.

- The White Picket Fence Dream: Detached single-family homes represented 81% of sales (up from 79% last year) followed by town- or rowhomes at 7%.

- Home Sweet Home: Overall, buyers expected to live in their homes for a median of 15 years, while 25% said that they were never moving.

But maybe the most important finding of the report was that both buyers and sellers overwhelmingly believed in the importance of using a real estate agent: 88% of buyers and 90% of sellers used an agent to assist with their transactions. Home buyers primarily sought help from an agent or broker in finding the right home to purchase (49%) and negotiating the terms of the sale (14%). Meanwhile, seller respondents reported that agents were most helpful for marketing the home to potential buyers (22%), pricing the home competitively (20%), and selling the home within a specific timeframe (18%). Finally, 88% of home buyers would use their agent again or recommend them to others.

If you’re contemplating a move, reach out to any of our experts at McEnearney Associates | Middleburg Real Estate | Atoka Properties to help you reach your real estate goals.

Read the full NAR report here.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Financing a Fixer-Upper

When the housing market is this tight, considering a home that needs a bit of work can pay off big dividends for flexible buyers.

Let’s face it, when purchasing a new home, most of us would prefer to purchase one with upgraded kitchens and baths, a new roof, new windows, new systems, and our favorite paint colors – oh, and in the ideal location. Most of us would also like to win the lottery.

None of those are realities for most people.

The housing market continues to struggle with a level of supply that is not keeping pace with demand. Buyers are competing for too few available houses and properties deemed “fixer-uppers” get less prospective buyer attention. However, these properties have untapped potential and should not be overlooked if a buyer is willing to take on the home improvement challenge and can identify the means to finance the effort.

As different properties require various levels of effort to improve them, the methods of financing those improvements can also differ greatly. Some buyers are flush with cash and have enough to cover a large down payment, closing costs, and improvements. Others struggle with how to meet the minimum cash requirement just to purchase a home. Just as homes differ in big and small ways, buyers need financing options that differ as well. Here are some general questions to consider.

Instead of making the down payment I had planned, can I make a smaller down payment and cover the cost of improvements with the cash I have retained?

The smaller down payment means a larger loan which requires a higher monthly payment. But since we are talking about fixer-uppers, the starting price for the home is presumably lower and therefore the loan amount is lower than would be the case for a home that did not need upgrades and improvements.

Can I borrow from my active retirement account to increase my cash to cover the down payment and the costs of improvements?

Most qualified retirement programs allow active participants to borrow for the purchase of a new home. The funds available can supplement or replace other savings which can then be used to cover the cost of repairs and improvements.

Does an FHA 203K loan make sense for my particular fixer-upper scenario?

Some lenders provide FHA 203K renovation loans for home purchasers that allow them to finance 96.5% of the cost of the purchase price plus qualified improvements and renovations.

- The streamlined 203K program allows for the purchase price plus non-structural renovations and upgrades up to an additional $75,000 in cost.

- The full 203K program allows for a purchase with major renovations up to a maximum loan amount in the Washington metro area of $1,149,825.

- The FHA programs require only 3.5% of the combined cost of the home purchase and renovations or upgrades from the purchaser.

Am I ready to take on a construction loan to turn the fixer-upper into my dream home?

Some lenders provide true construction financing which can finance anything from a major kitchen and bath renovation to buying a vacant lot and building a new home and can be an effective method to finance the complete renovation of a true fixer-upper. Often there is great value in the “bones” of the structure and the location of that structure but very little value in anything else associated with the property. A construction loan may be the best approach to acquiring and bringing new life to a tired, old, fixer-upper.

If you are lucky enough to find your perfect turn-key home in this competitive market, you can expect to pay top dollar for it. But savvy home buyers will tell you the best value is in properties that require some sweat equity and TLC. Keeping that in mind and identifying the best way to finance those efforts can open more homebuying opportunities in our tight housing market.

Please reach out to me or my colleagues at Atlantic Coast Mortgage to have a conversation about whether a construction loan works for your homebuying goals.

Brian Bonnet

SVP, Sr. Loan Officer, NMLS: 224811

Atlantic Coast Mortgage, NMLS: 643114

O: (703) 766-6702 | M: (703) 304-0188

Notice: This is an advertisement and is not a commitment to lend. Contact a loan officer today to explore the financing options specific to each borrower.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

When Do You Need a Licensed Contractor vs. a Handyman?

Picking the right pro for the job takes a little homework.

There comes a day in every homeowner’s life when you realize: it’s time for reinforcements. Whether it’s a leaky pipe, a new electrical box, replacing an appliance, or drying a wet basement, finding a fix starts with choosing the right expert for the job. However, not all home projects are created equally, so how do you know whether to call a handyman or a licensed contractor?

(Renters, you will call your Landlord or Property Manager!)

The main differences between a licensed contractor and a handyman are the type and size of jobs they work on, their licensing requirements, and how many people they supervise. Contractors typically work on larger projects, like home additions or renovations, while handymen usually work on smaller projects and home maintenance.

When it comes to licensing, do your research for the requirements in your area as some handyman work may require a contractor’s license. For example, there are three levels of general contractor license in Virginia, based on the size of the job being performed. The lowest level of general contractor’s license, a class C license, allows for residential contracting jobs between the amount of $1,000 and $10,000, including materials and labor, while Class A contractors perform or manage construction, removal, repair, or improvements for projects $120,000 or more, or when costs for any12-month period is $750,000 or more.

A handyman may do work that includes painting, drywall repair, window or door repair, replacing faucets or electrical outlets, swapping out light fixtures, laying carpet, hanging curtains, or installing shelves. For smaller jobs that can be completed in a couple of hours or a day or two, homeowners can check out popular options on sites like TaskRabbit and Thumbtack – like Uber or DoorDash for home projects, complete with client reviews – or Angi (formerly Angie’s List), which also offers contractors for larger jobs. Handyman fees can be charged by the hour or per the project and generally don’t require signing a contract.

States often require a contractor’s license for jobs that cost more than a certain amount, require structural changes, or involve electrical, plumbing, or HVAC work. Sometimes the project may require a permit for work being contracted, including these examples:

- New windows. Replacing an existing window does not need a permit, but cutting a hole for a new window does. This includes new doors and skylights.

- Most municipalities require permits for siding projects whether you use strong cardboard or other materials.

- Not all fencing projects require a building permit but cities often place restrictions on non-permitted fences. For example, in Maryland’s Montgomery and Prince George’s Counties a permit is needed for fences 4-feet or higher while in Howard County it’s 6-feet or higher and in Calvert County it’s 7-feet or higher.

- Electrical and plumbing. If you’re installing new or removing current plumbing permits, you’ll need a permit. Any improvement project that includes installing a new electrical system also requires a permit.

- Water heater. You need a permit if you want to replace your water heater.

Who can apply for permits, expiration dates, and other details vary based on the type of permit required so be sure to check your local jurisdiction to confirm whether it will be you as the homeowner or the contractor who will apply for the appropriate permits. Regardless of whether you’re hiring a handyman or a contractor, interview a few professionals to see who fits best based on their expertise and how they answer these questions:

- How long has your company been in business?

- What experience do you have with this type of project?

- Do you have the necessary permits or licenses?

- Do you have references?

- What is the cost estimate?

- What is the timeline for this project?

- Are you insured?

Big or small, it can feel daunting to start a home improvement project, especially if it comes up unexpectedly due to damage or a breakdown. But with a bit of research and planning, you can find a home improvement professional who will work with your timeline and budget. And if you need recommendations, reach out to your trusted McEnearney Associates | Middleburg Real Estate | Atoka Properties agent to see who they use when they’re in need of the best!

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Navigating the Financing Contingency

When “Show me the money!” meets “Not so fast!” in buying a home.

On the winding road from purchase offer to contract ratification to settlement, there are a few speedbumps that both buyers and sellers must navigate together. Contingencies are one type of speedbump, additional agreements that the contract will continue to move forward as long as certain conditions are met.

Sonia Downard, Title Attorney with Vesta Settlements, recently spoke to our agents about guiding clients through the Financing Contingency for sales in Virginia and avoiding missteps along the way. She explained that while the financing contingency can benefit both the buyer and seller in a sale, it is decidedly buyer-friendly with several protections.

In a real estate transaction, the Financing Contingency is the clause that gives buyers time to secure the financing for the purchase of a property – usually through a mortgage with a lending institution – within a specific time period. If a buyer is unable to secure financing, they can void the contract using this contingency and avoid legal penalties or losing their EMD (earnest money deposit.)

The most common types of financing are Conventional (the most popular), VA (for veteran and military buyers), FHA (great for first-time homebuyers and those with limited cash for down payments and fees), and USDA (for properties in rural areas).

Financing contingencies can have an automatic extension or an automatic termination, and a buyer can satisfy or remove the contingency by delivering to the seller a written commitment from the lender for the required financing. If a buyer misses the financing contingency deadline and has an automatic extension, the seller can deliver a written notice to the buyer that they have three days to remove the contingency or void the contract. However, it’s more likely that the seller will allow a contingency to remain in place up until settlement as lenders complete their final underwriting tasks.

If the buyer does not void the contract or deliver the written commitment from the lender, the contract stays in place without the protection of a financing contingency. On the other hand, if the buyer receives a written rejection letter from the lender for their specified financing and delivers it to the seller within the contingency time frame or within the three days of a seller requesting lender commitment, the contract becomes void. For contingencies with an automatic termination, the contingency expires on the specified date and the contract continues in full force and effect without the financing contingency protection.

An Appraisal Contingency plays a part in the financing contingency because the appraisal report is used to determine the value of the loan collateral, and if the property does not appraise for the contracted sales price the buyer could be denied financing. If the appraised value meets the contracted sales price or if the buyer elects to make up any difference between the appraised value and the contracted sales price, the appraisal contingency is removed. But if the property does not appraise, is not approved for specified funding (ex: denying a VA loan to be used to buy acreage), or has inadequate collateral (ex: an illegal living unit on the property that affects zoning requirements), the buyer can deliver notice to the seller to void the contract, along with a letter from the lender denying financing.

Some buyers skip including an appraisal contingency to make their offer more competitive, relying solely on the financing contingency for protection. But Downard reminds buyers to remember that the appraisal contingency relates to the value of the property and not the purchaser’s qualifications for the loan itself, and to keep in mind that the protections offered are different between the two types of contingencies. Note that VA, FHA, and USDA loans – as federally-backed loans – cannot waive an appraisal, and these specific buyers have the right to void a contract if the property does not appraise, bypassing any further negotiations with the seller. In this case, the seller cannot “save” the deal by lowering the sales price to the appraised value as they could have with a conventional loan buyer.

Lender-required repairs can also come up with financing contingencies – most often with VA and FHA loans – requiring the buyer to give the seller notice from the lender about needed fixes, and the two parties can negotiate how to complete the repairs and who will pay. Sellers have five days to give notice to buyers if they will make the lender-required repairs, and if the seller does not agree then the buyer has an additional five days to agree to make the fixes or void the contract.

Understanding the details of a contract and having the insight and experience to help people move through the different stages of homeownership is why Realtors® provide so much value to their clients. Connect with one of our McEnearney Associates | Middleburg Real Estate | Atoka Properties Associates and be confident you will be guided by the best!

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

The State of the Housing Market in Washington, DC & Surrounding Areas – October 2024

Market in a Minute & StatPak October 2024

We profile the most important market indicators every month – contract activity, interest rates, inventory, affordability and direction of the market – in an easy to read and digest summary. It’s not just the numbers; it provides context to understand why the numbers are important and what they mean for the future of the market. Published for Washington, DC, Montgomery County, Prince George’s County, Northern Virginia, and Loudoun County. A quick summary of last month’s contract activity is shown below. To see the complete “Market in a Minute” reports for each jurisdiction we cover, click on the corresponding links.

What’s the Urgency Index?

This is simply the measure of the percentage of homes going under contract that were on the market 30 days or less, giving a sense of how quickly buyers feel they must act to put an offer on a home. To see your market’s Urgency Index click the link to view the full report.

Washington, DC

October 2024 StatPak – View Full Report

Contract activity in September 2024 was up 5.6% from September 2023 and was up in five out of six price categories. Through the first nine months of the year, contract activity is down 12.5%. The average number of days on the market for homes receiving contracts was 61 days in September 2024, up from 50 days in September 2023.

Montgomery County

October 2024 StatPak – View Full Report

Contract activity in September 2024 was up 16.2% from September 2023 and was up in five out of six price categories. Through the first nine months of the year, contract activity is up 2.9%. The average number of days on the market for homes receiving contracts was 25 days in September 2024, up from 21 days last September.

Prince George’s County

October 2024 StatPak – View Full Report

Contract activity in September 2024 was up 17.3% from September 2023 and was up for four out of five price categories. Through the first nine months of the year, contract activity is up 2.6%. The average number of days on the market for homes receiving contracts was 39 days in September 2024, up from 28 days in September 2023.

Northern Virginia

October 2024 StatPak – View Full Report

Contract activity in September 2024 was up 13.3% from September 2023 and was up for five price categories. Through the first nine months of the year, contract activity is basically unchanged. The average number of days on the market for homes receiving contracts was 25 days in September 2024, up from 24 days last September.

Loudoun County

October 2024 StatPak – View Full Report

Contract activity in September 2024 was up 32.8% from last September and was up for four price categories. Through the first nine months of the year, contract activity is up 3.3%. The average number of days on the market for homes receiving contracts was 24 days in September 2024, up from 21 days last September.

Virginia Countyside

October 2024 StatPak – View Full Report

Contract activity in September 2024 was up 25.3% from last September and was up for five price categories. Through the first nine months of the year, contract activity is up 11.5%. That’s the best in the region by far. The average number of days on the market for homes receiving contracts was 40 days in September 2024, up from 32 days last September.

Take a look at our website for all of our listings available throughout Washington, D.C., Maryland, and Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()