Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Cannonball! Listings With Pools That Make a Splash

It’s heating up out there, and a refreshing dip in your own pool is the perfect way to cool down. If the sound of splashing water is what’s missing from your ideal backyard oasis, check out these cool listings from Corcoran McEnearney that feature pools and other water features.

And please invite us to your next pool party!

40959 Pacer Lane | Paeonian Springs, VA

This exceptional estate, sprawling across more than 14 acres of open land, offers a sanctuary of privacy and breathtaking natural beauty. The outdoor living spaces are designed for both grand entertaining and serene relaxation, starting with the expansive front porch. A 20-foot diameter stone fire pit, surrounded by a flagstone hardscape, creates an inviting ambiance for gatherings under the stars. A sparkling pool with built-in hot tub offers resort-style amenities, while covered & screened porches off the kitchen and first-floor primary suite provide seamless indoor-outdoor living.

Listed by: Ryan Clegg, Leesburg Office

1107 Savile Lane | McLean, VA

Recently featured for its outdoor kitchen on Inhabit, the Corcoran Blog, this spacious private estate will satisfy the most discerning buyer. Stunning 2020 whole-home renovation features modern design and high-end finishes. A refined and fully finished basement (including dressing rooms and a fully equipped kitchen) makes entertaining at the pool easy.

Listed by: Sandy McMaster, Alexandria Office

10052 Possum Hollow Drive | Delaplane, VA

Gap Run Farm is a beautifully maintained 50-acre country estate in the heart of Fauquier County. The thoughtfully designed main residence features more than 4,000 square feet of living space. Beautiful slate patios overlook the recently enhanced pool. A second 2-bedroom, 2-bath home provides comfortable accommodations for guests, extended family, or a farm manager. Perfect for the horse enthusiast, the property boasts an 8-stall center-aisle well-appointed barn, an outdoor arena overlooking the serene pond, and thoughtfully positioned turn-out paddocks with several run-in sheds and automatic waterers.

Listed by: Kerrie Jenkins, Middleburg Office

2506 Coulter Lane | Oakton, VA

This magnificent residence on 1.72 acres offers abundant space for relaxation and entertainment. More than 11,000 square feet of meticulously crafted living space extends to an outdoor oasis. The expansive patio area features a bar, outdoor grill area, and a tiered in-ground pool and spa, complete with a new heater, pump, and salination system for easy maintenance.

Listed by: Becky & Barb, Ashburn Office

2504 Sherwood Hall Lane | Alexandria, VA

Nestled behind a private gated entrance on over three-quarters of an acre, this remarkable estate offers unmatched privacy, luxury, and space to live, entertain, and relax. This outdoor oasis includes a large pool, relaxing hot tub, custom putting green, charming gazebo, and a fully-equipped tiki bar with an outdoor kitchen—ideal for hosting unforgettable gatherings.

Listed by: Rebecca McCullough, Alexandria Office

2030 Huntwood Drive | Gambrills, MD

This lifestyle property is the perfect private retreat. Location, presence, design, comfort, and appointments combine beautifully to create a haven of peace and privacy, less than 10 miles from downtown Annapolis.

Listed by: Sandy Chee, McLean Office

6320 Crosswoods Circle | Falls Church, VA

We know it’s not a pool, but Lake Barcroft is one of the area’s most sought-after lake communities with 5 sandy beaches, kayaking, sailing, canoeing, swimming, fishing, and more. This 5-bedroom waterfront home is just the spot to enjoy life on the lake to the fullest. Fabulous views from the home, deck, and two paver patios—one with a fire pit. Pathways with handsome stone steps lead to the boardwalk and dock. Oh, and the pontoon boat conveys!

Listed by: Susan Tull O’Reilly, McLean Office

If a home with a pool has been on your wish list, your Corcoran McEnearney agent will not only help you find those listings but will also be a great resource for recommending contractors and service professionals to maintain your splashy investment. Dive in and reach out today before the next heat wave hits!

Visit corcoranmce.com to search listings for sale in Washington, D.C., Maryland, Virginia, and West Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Where is the Housing Market Headed?

Everyone is talking about the market, but what is the market actually telling us?

A steady stream of spring market data is signaling a shift toward balance in the DC metro housing market, with homes staying on the market longer and buyers increasingly approaching a home purchase with negotiation in mind.

Despite record-high home prices in the DC metro area, May 2025 showed a modest rebound in contract activity across several jurisdictions. However, the broader year-to-date trend remains slightly down. We’re seeing modest week-over-week growth in the number of newly ratified – but that growth is very unevenly distributed.

- Northern Virginia led the way with a 9.9% year-over-year increase in May contracts, followed by Montgomery County (up 5.2%) and the District (up 4.0%).

- Loudoun County (up 0.8%) and the Virginia Countryside (down 0.4%) saw smaller changes, while Prince George’s County posted a slight 0.2% dip.

- However, most areas are still trailing slightly behind 2024 levels for the first five months of the year, with contract activity down between 0.4% and 10.2%.

Homes are also taking longer to sell: average days on market rose across the region, ranging from 23 days in Northern Virginia and Loudoun County to 55 days in the District. Together, these indicators reflect a market adjusting toward balance, where motivated sellers must work to stand out, and buyers may find emerging opportunities.

Whether you’re on the market to buy or sell, or thinking about jumping in, here’s what to keep in mind.

If Your Home Is Listed

Compared to last May, the number of homes on the market has risen significantly in every jurisdiction, and this is absolutely a market where “price matters and time kills.” Even though contract activity was very stable compared to last May, that rising inventory pushed down absorption rates – the rate at which available properties go under contract within that month – pretty much across the board.

Home prices are still strong, more than half of homes are selling at or above list, and in most local jurisdictions, the absorption rates are above the 30% threshold for a “Sellers Market.” But absorption rates are tracking lower by the month, not just year over year. Some tips if you currently have a “For Sale” sign on your home right now:

- Be Competitive When Pricing: Be realistic given current conditions and get familiar with the factors that are influencing your neighborhood, and watch for signs in other comparable areas that things are selling more quickly or slowly than your home. Smart sellers know this is not the time to “test the market” and push the envelope on peak pricing.

- Consider Strategic Staging & Renovations: The first showing is your home’s audition, and you may not get the chance at a callback. Make sure your home is perfectly presented from the minute a buyer pulls up and that a tour reinforces that the home is show-ready. Offers with home inspection contingencies are more common now, especially if buyers are paying top-dollar (they want to know what they’re getting!) Making sure your listing is sound in structure and appointed with the modern conveniences that buyers flock to will ensure it stands out from an increasingly crowded field of options. Allowing pre-offer inspections will also keep serious buyers engaged and moving toward a clean offer.

- Flexible Financial Incentives: With prices and mortgage rates still in the upper ranges, entice buyers with concessions like rate buydowns (which 37% of new construction builders are using) and other sweeteners like paying their agent’s compensation or offering money towards closing costs.

- Targeted marketing: Work with your agent to emphasize neighborhood strengths and include a list of great features and resources that can be found in the area. Don’t assume buyers have time to do the local research that you’ve accumulated over the years. Brag about what makes your home in that neighborhood such a great place to live!

If You’re In the Market To Buy

- Opportunity window: Prices stabilizing (or not increasing as rapidly), and more inventory is giving buyers the best shot in a long time for negotiating leverage. With more choices and fewer bidding wars, buyers can negotiate better, and smart sellers on a tight timeframe may be willing to negotiate on everything from buyer concessions to price reductions.

- Mortgage rate plateau: Mortgage rates have steadied at just under 7%, with recent retreat into the mid‑6% range (around 6.84–6.85%). While still elevated, this plateau signals some relief and suggests rates may remain fairly stable or ease modestly as inflation cools.

- Be prepared: Readiness is critical – having your pre‑approval in hand, being flexible on timelines when possible, and taking swift action when you find a home can mean the difference between winning a deal or watching it slip away.

- Get Creative with Financing Fixer-Uppers: Sometimes that “Dream Home” is actually a work in progress. If you have the vision to take a home that needs some TLC to make it your own, remodeling and investment loans – like a VA Renovation Loan, FHA 203(k) or Fannie Mae’s HomeStyle – can help you finance both the purchase and the renovation in one package.

Looking Ahead

Timing the market when buying or selling a home is difficult because real estate is influenced by many unpredictable factors – interest rates, inventory levels, economic shifts, and even seasonal trends. By the time a trend is clear, it’s often already reflected in prices or competition. Trying to “wait for the perfect moment” can mean missing real opportunities that align with your needs, rather than the market’s.

Sellers, make sure to adjust your pricing in response to the market – three weeks without an offer is probably an indication that you’re off the market and need to reevaluate either your pricing, your home’s condition, your marketing efforts… or all three. Buyers, this is a great opportunity to come off the sidelines and engage intentionally and smartly with motivated sellers to secure your spot on the path to homeownership.

Incoming insight suggests a turning tide: Sellers who price smart and stage carefully will still succeed, while buyers who come armed with preparation can capitalize on enhanced bargaining power.

Read more housing analysis in our Market in a Minute and Weekly Meter, and connect with one of our agents to find the best strategy to sell or buy your home!

Karisue Wyson

Karisue Wyson is the Director of Education for Corcoran McEnearney and was previously a Top Producing Realtor® in the Alexandria Office.

Visit corcoranmce.com to search listings for sale in Washington, D.C., Maryland, Virginia, and West Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Dream It, Fix It, Love It: Renovate with a VA Loan

June is for fresh starts, including home renovations.

As the days get longer and the weather warms up, June sparks a sense of renewal. It’s the perfect time to tackle projects that have been sitting on the back burner, especially when it comes to upgrading your living space. If you’re a Veteran or active-duty service member, there’s one option that might surprise you: the VA Renovation Loan.

Whether you’re buying a new home that needs some work or looking to refresh the one you already own, this program could be the key to making it happen with little to no upfront cost.

What are the benefits of a VA Loan program?

The VA loan benefit is earned through military service and is one very advantageous way that military personnel can buy, build, or improve a home. A few reasons that VA loans are a great option for qualified buyers and current homeowners:

- No down payment as long as the sales price isn’t higher than the home’s appraised value (the value set for the home after an expert reviews the property).

- Better terms and interest rates than other loans from private banks, mortgage companies, or credit unions (also called lenders).

- The ability to borrow up to the Fannie Mae/Freddie Mac conforming loan limit on a no-down-payment loan in most areas—and more in some high-cost counties. You can borrow more than this amount if you want to make a down payment. Learn more about VA loan limits here.

- No need for private mortgage insurance (PMI) or mortgage insurance premiums (MIP).

- No penalty fee if you pay the loan off early.

What is the VA Renovation Loan?

The VA Renovation Loan lets eligible borrowers roll the cost of home improvements directly into their mortgage, without needing a second loan or draining their savings. It’s designed specifically for primary residences and offers up to 100% financing, making it one of the most accessible ways to upgrade a home.

For example, maybe you want to modernize your kitchen, replace outdated flooring, or add accessibility features to suit your needs. As long as the repairs are non-structural and can be completed within 75 days of loan funding, they may be covered.

What can you use it for?

Eligible renovations include everything from new appliances and updated HVAC systems to roof replacements, plumbing work, bathroom remodels, and more. The loan is flexible enough to support both cosmetic improvements and essential repairs. In short, if the work makes the home more livable, efficient, or functional, there’s a good chance it’s allowed.

Who can apply?

This program is available to active-duty service members, Veterans, Reservists, National Guard members, and certain surviving spouses. If you’ve served our country, this is one way your benefits can serve you—helping you build a better home with a smarter financial strategy.

Not a VA Borrower? You’ve still got options!

Even if you don’t qualify for the VA Renovation Loan, June is still a great time to explore other renovation financing options:

- FHA 203(k) Loans – These are perfect for homebuyers or homeowners looking to finance repairs and upgrades. The “Standard” version allows for structural changes and phased construction, while the “Limited” version is ideal for smaller, cosmetic projects.

- Fannie Mae HomeStyle® Renovation – A conventional loan that covers a wide range of upgrades, including landscaping, green energy improvements, and accessory dwelling units (ADUs)

- Freddie Mac CHOICERenovation® – Similar to the HomeStyle loan, this option is designed for buyers who want to customize or modernize their home purchase while keeping everything under one convenient mortgage.

Why June is the ideal time to start?

With summer break in full swing and longer daylight hours, June offers the perfect window to start a renovation project—especially one that can be completed before fall routines pick back up. Contractors may be more available, and renovation financing can give you the boost you need without delaying your goals or draining your savings.

If you’re thinking about buying a home that needs a little work or you’re ready to tackle that dream upgrade, this might be your moment. Ready to explore your options? Reach out today and take the first step toward making it happen.

Bill Stern | The Stern Team

Branch Manager | NMLS ID # 267577

CMG Home Loans | NMLS ID# 1820

M: 540-222-0164

bstern@cmghomeloans.com

Notice: This is an advertisement and is not a commitment to lend. Contact a loan officer today to explore the financing options specific to each borrower.

Visit corcoranmce.com to search listings for sale in Washington, D.C., Maryland, Virginia, and West Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Financing Investment Properties May be Easier Than You Think

You don’t have to be a financial whiz to make smart moves in real estate investing.

Owning residential investment property in the Washington Metropolitan area provides multiple advantages: steady cash flow, solid appreciation, and a hedge against inflation. Rental properties, which command a high enough monthly rent to cover a mortgage payment, may be viewed similarly to a blue-chip stock where the monthly principal curtailment is akin to a regular dividend payment. And while a stock can theoretically lose all of its value, “dirt does not go to zero.”

For some, acquiring residential investment property is a function of converting an existing primary residence into one that brings cash flow. For others, the acquisition requires purchasing property and obtaining financing for that purchase. The good news is that underwriting guidelines for residential investment financing have loosened in recent years, and Fannie Mae and Freddie Mac investment property loans no longer require down payments of 20%. A purchaser may put down as little as 15% of the purchase price, making the acquisition more attainable for some. If the down payment is less than 20% then mortgage insurance is required, which increases the monthly payment. Interest rates are more favorable if the down payment is at least 20%, and even more so if the down payment is at least 25%. Note that investment property loans do not allow for the use of gift funds to cover down payment, closing costs or reserve requirements.

For most individuals, qualifying for an investment property loan from an income and debt standpoint has also become easier. Lenders will generally use 75% of the expected rental income to offset the proposed mortgage payment. For instance, if the proposed mortgage payment on an investment property purchase is $3000 per month and the anticipated rent as determined by the lender’s appraiser is also $3000 per month, in most cases, the lender will give the mortgage applicant credit for $2250 (75% of anticipated rent) to offset the new monthly payment. This results in a new debt for qualifying purposes of only $750 per month. Standard conforming conventional loans do not require a lease to be in place for the property to be purchased and borrowers do not need to show a history of managing rental property.

Investment property loans do require the borrower to show reserve assets in the form of savings, brokerage, or retirement assets. The guidelines differ somewhat between Fannie Mae and Freddie Mac loans; Fannie requires reserve assets calculated as a percentage of the unpaid balances on all real estate loans held by the borrower, while Freddie requires a certain number of months of principal, interest, taxes, insurance, and HOA/Condo dues (PITIA) for all financed property held by the borrower. Neither set of guidelines is too onerous as Fannie requires reserves to be as little as 2% of outstanding balances on all mortgages held and Freddie requires as little as 2 months of PITIA on all properties owned and encumbered by mortgages.

The borrower’s application process for investment property loans is identical to that for a loan to purchase a primary residence, and there is no significant additional time needed by the lender to complete the underwriting process. The lender’s appraisal of the property will include one additional component referred to as a comparable rent schedule, which is used to determine the likely gross monthly rental income of the property. Other than that, the overall lender process and documentation requirements of the borrower are no different than for other residential loan applications. A borrower can ratify a contract for an investment property purchase and proceed to settlement just as quickly as they could for the purchase of a primary residence.

Ownership of residential investment property does not require advanced financial education and financing the purchase of residential investment property is generally just as easy as financing a primary residence.

Brian Bonnet, SVP, Sr. Loan Officer, NMLS ID 224811

Brian Bonnet, SVP, Sr. Loan Officer, NMLS ID 224811

Atlantic Coast Mortgage, NMLS ID 643114

O: 703-766-6702 | M: 703-304-0188

Email Me

Notice: This is an advertisement and is not a commitment to lend. Contact a loan officer today to explore the financing options specific to each borrower.

Visit corcoranmce.com to search listings for sale in Washington, D.C., Maryland, Virginia, and West Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

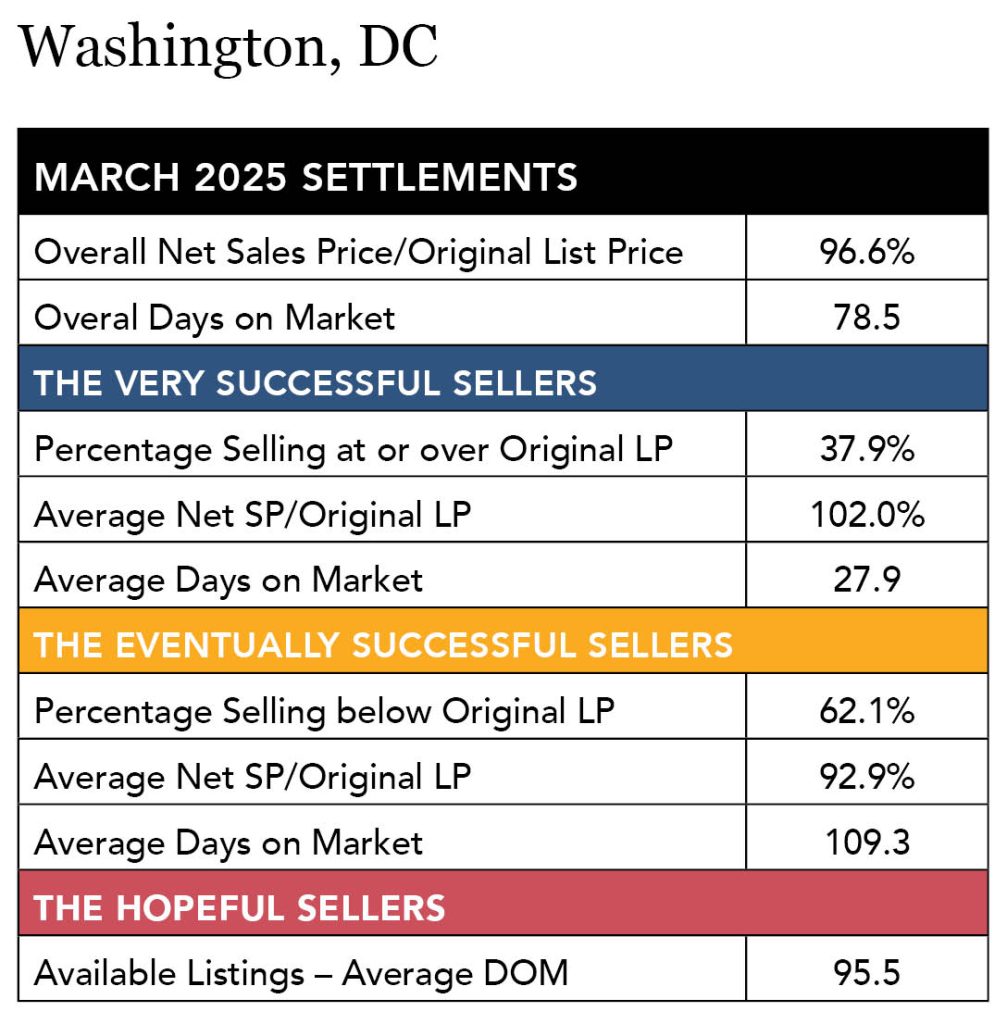

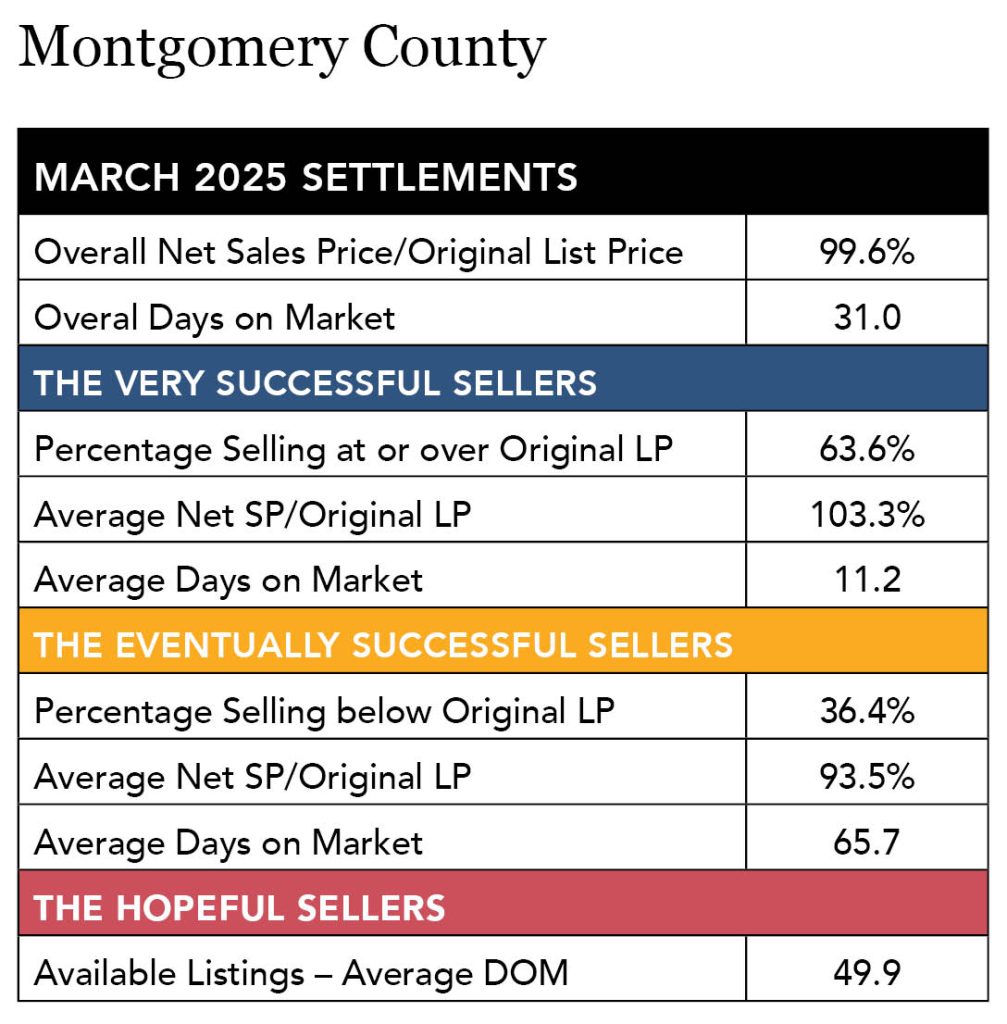

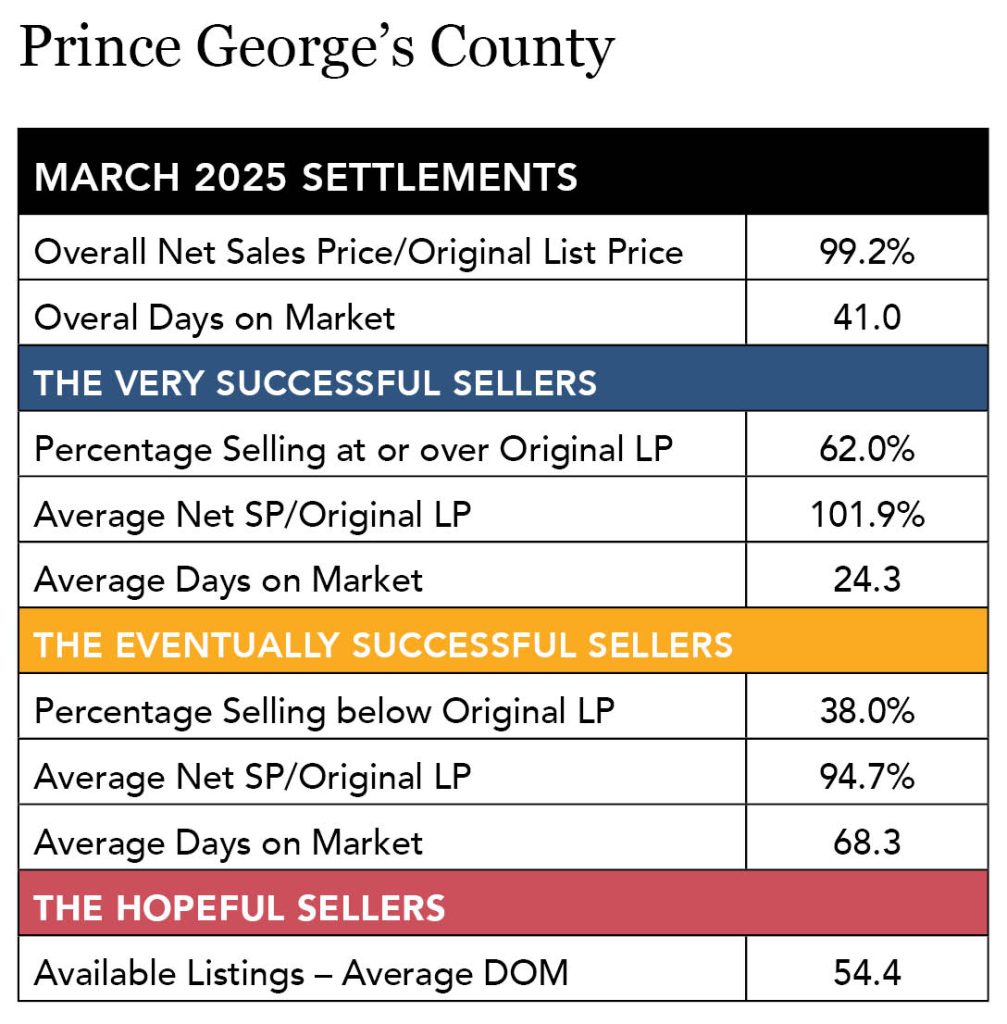

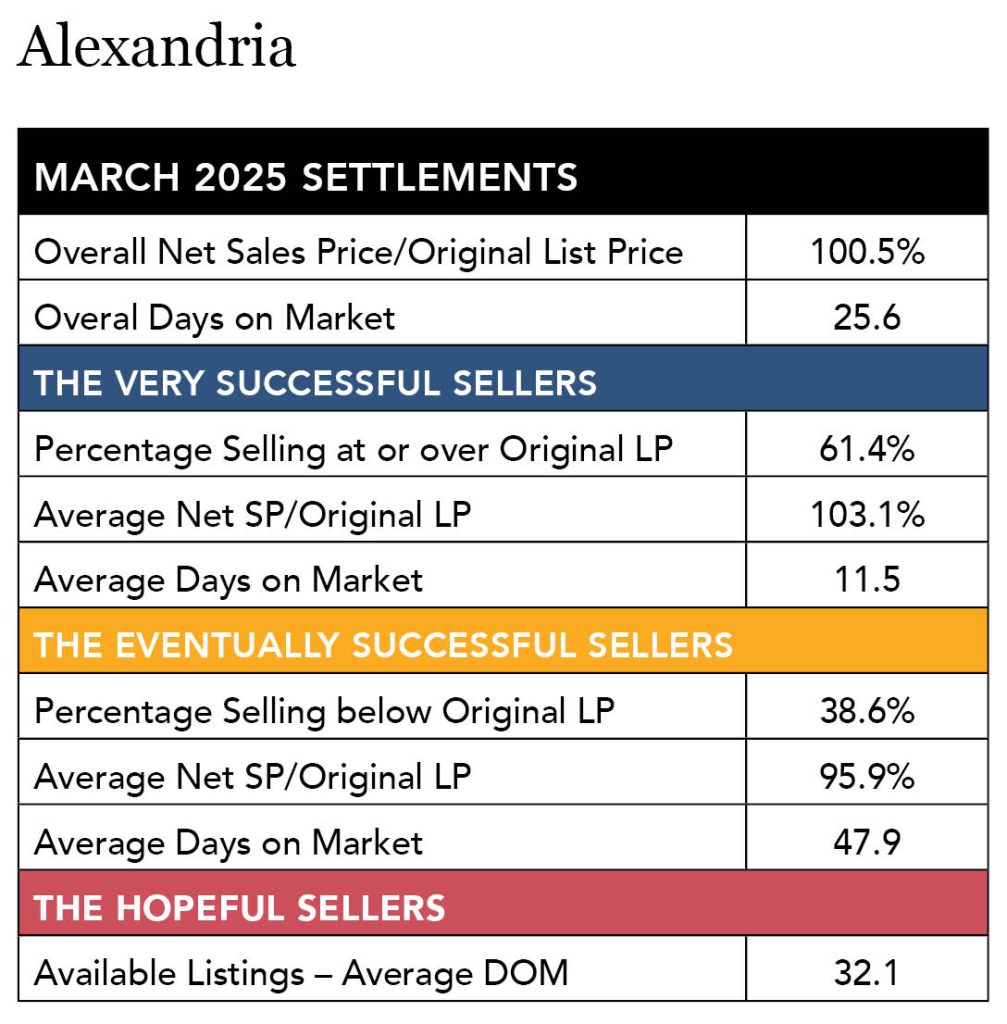

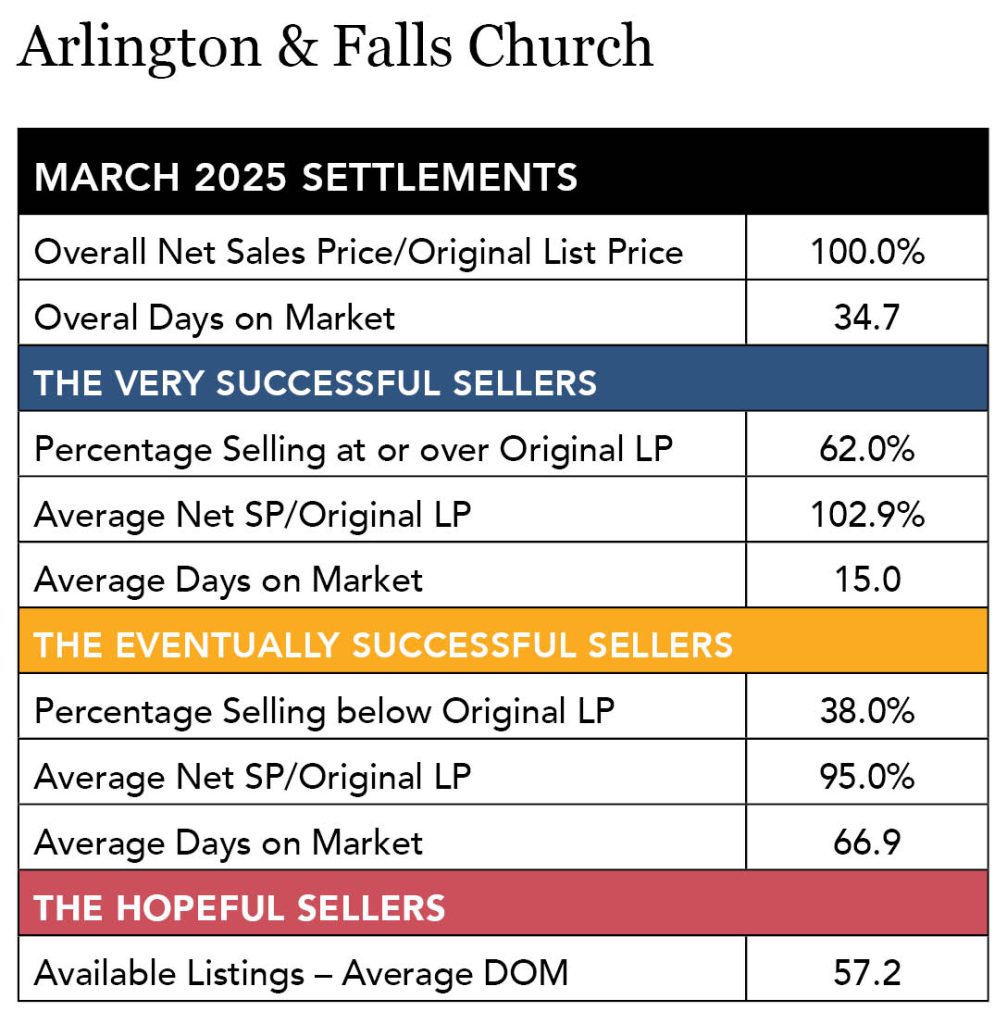

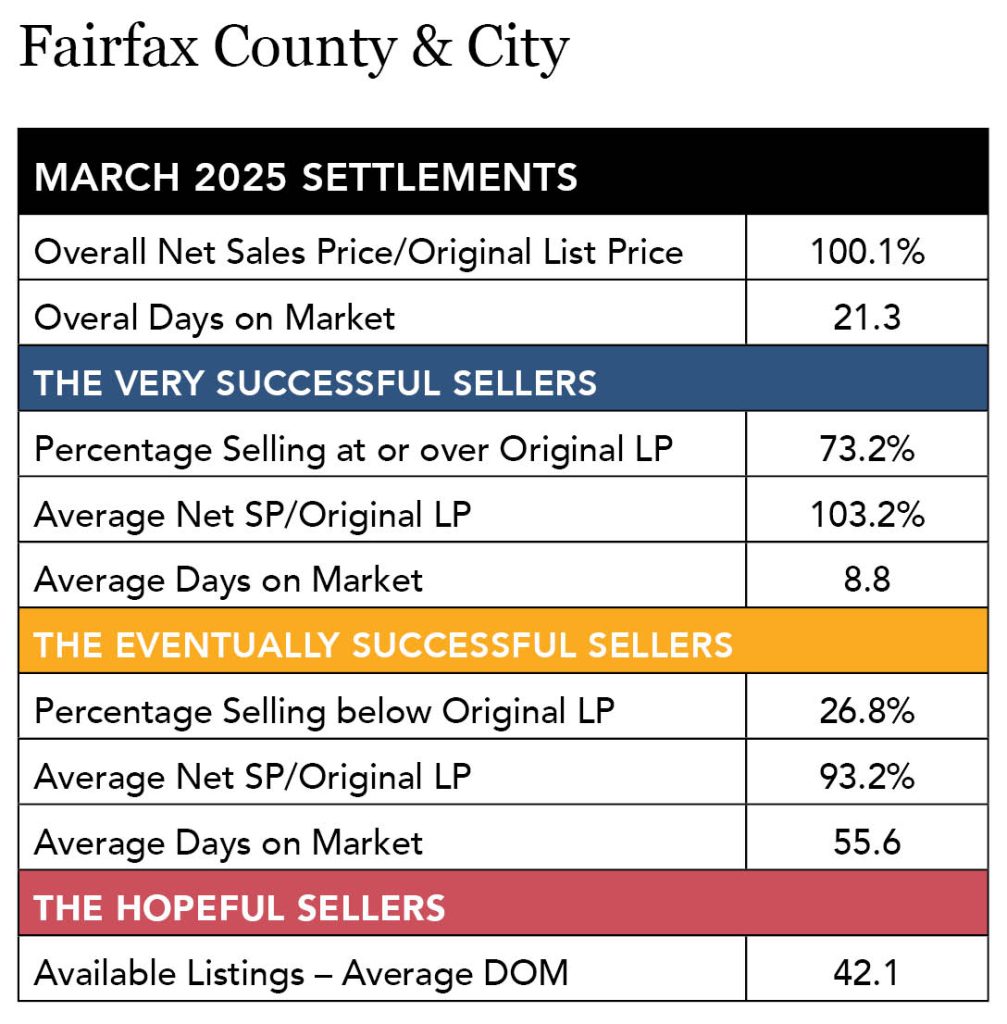

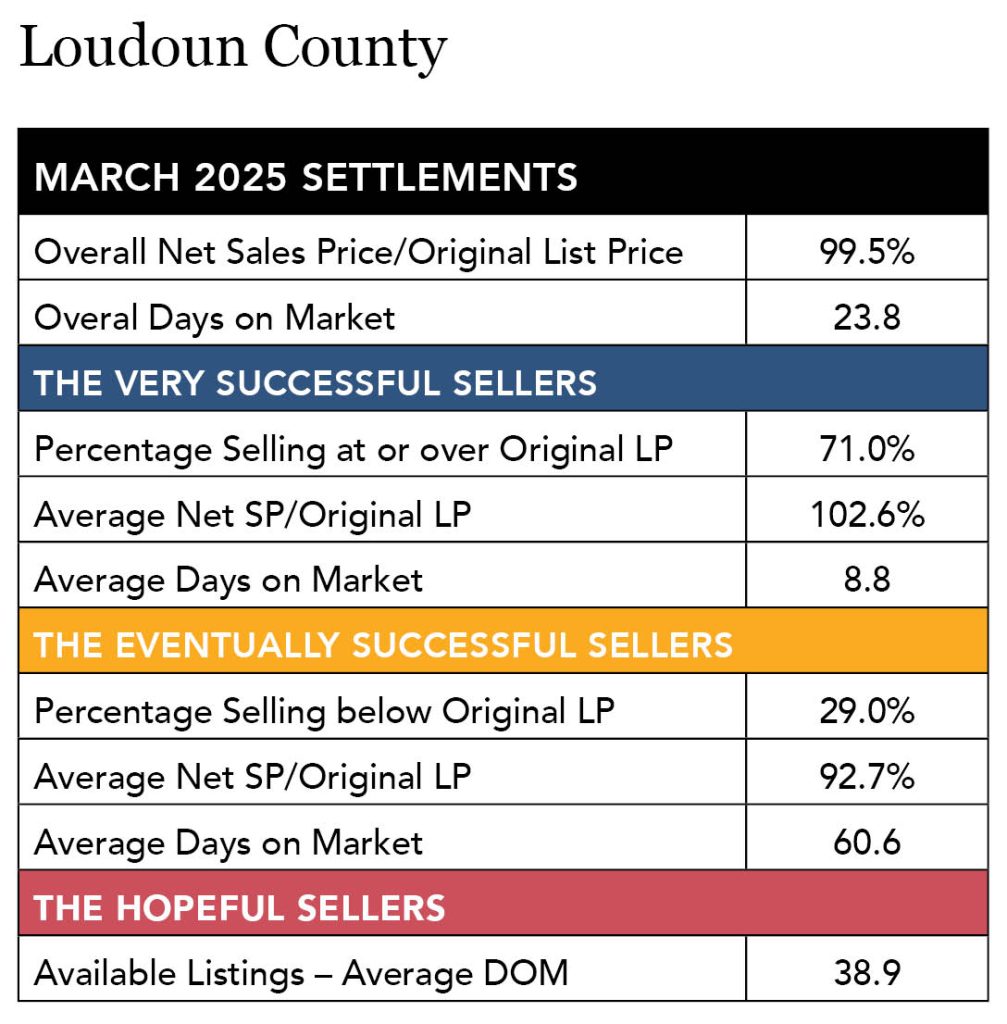

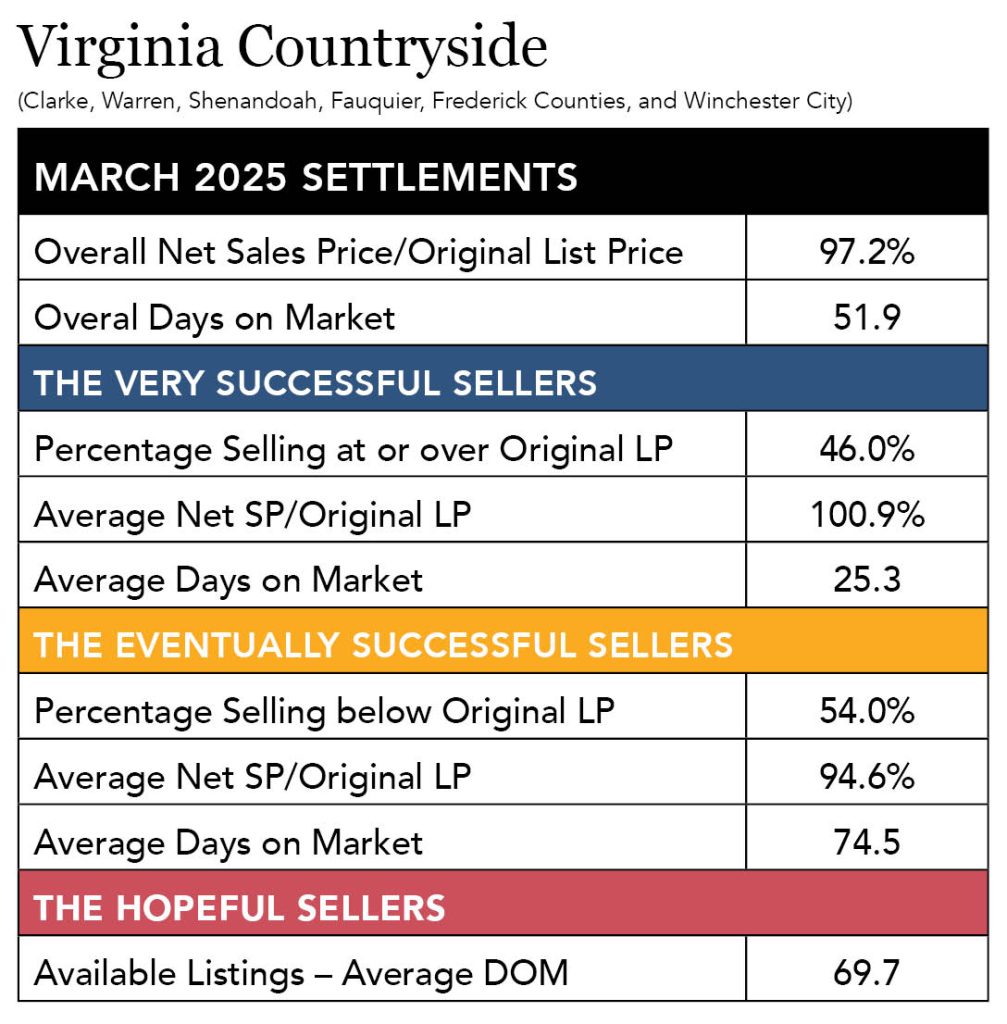

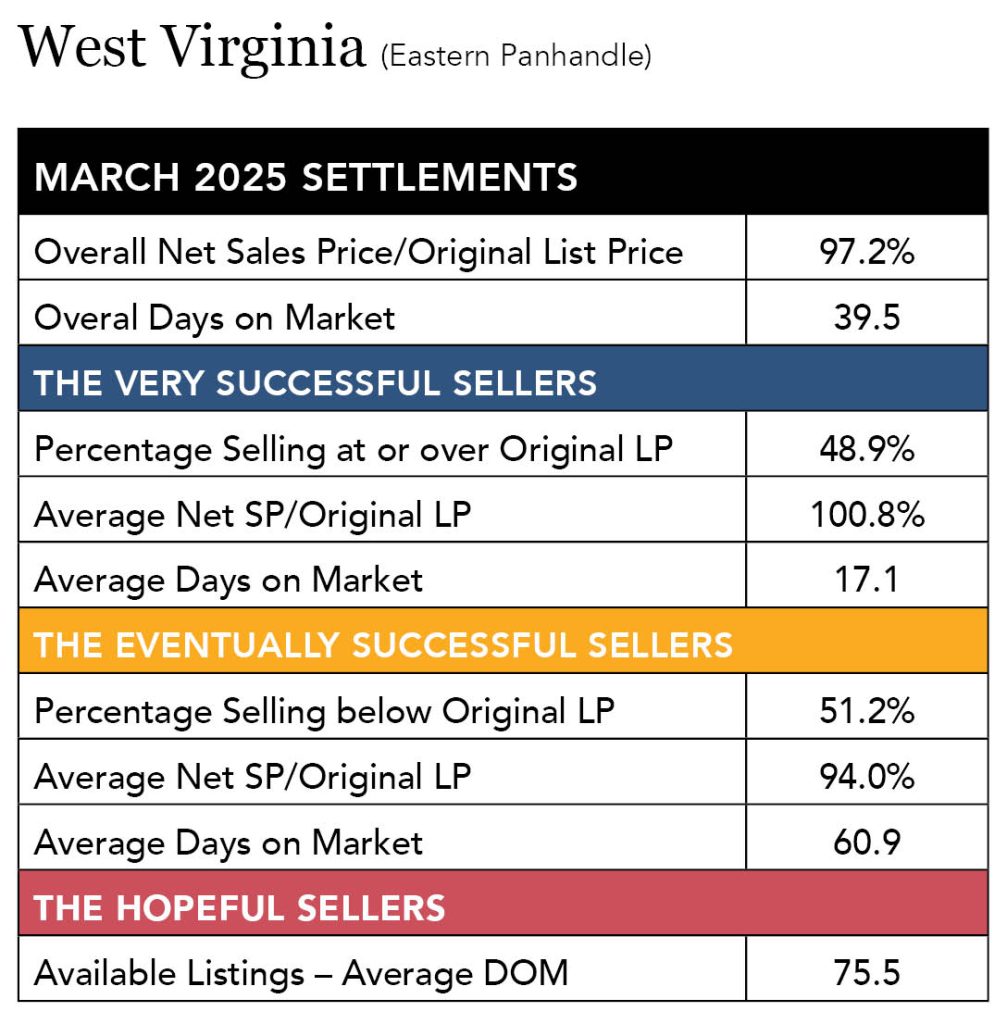

Spring 2025 Selling Trends: Inventory Is Up, Pricing Is Crucial

Data is coming in from the start of the spring selling market. Inventory is up, but it’s still a seller’s market … if the price is right.

Now that we are in the thick of the spring market, let’s look at which sellers are succeeding and which are still waiting for their buyers. And if you’re a seller getting ready to come to market, heed the warning: price matters and time kills.

General Takeaways

Compared to March 2024, there has been a noticeable cooling of the market. Homes in general are taking a little longer to sell and aren’t selling as close to their original list price. But the differences aren’t huge – about 1% less and about 5 days longer.

Inventory is also influencing the statistical story. In every jurisdiction, the number of homes on the market at the end of March 2025 was up considerably from March of last year. An example: Northern Virginia inventory is 69% higher than it was this time last year. But, again, it’s a matter of context. Despite the big percentage increases, inventory in most areas is still well below the “normal” levels we saw pre-COVID. Overall supply in most of the suburban markets is still less than 1.5 months. DC stands at 4 months.

The biggest difference in most areas we track are the average days on market for the “eventually successful sellers” – those who sold at a net sales price less than their original list price. Compared to last March, those sellers are typically taking 20 days to as much as 40 days longer to sell than a year ago.

Even with the increase in inventory, absorption rates – the number of homes that are sold in a specified month in comparison to those still on the market – are still north of the 30% threshold for a “seller’s market” almost everywhere in the Greater DC/Baltimore Metroplex. The exceptions are all three property types in DC itself, and condos in Baltimore City – those reflect a balanced market.

Given the uncertainty in the economy, the market is holding up well. And as always, the specifics change when looking at more granular geographic, property type and price range data. For example, even though the overall condo absorption rate in Arlington County was 34% in March, it was 58% in Shirlington/Fairlington and 20% in Crystal City. Those differences really matter to a seller when making the final decision with an agent about what price to list a property.

It’s still a seller’s market throughout most of the region, but, in general, sellers don’t have as much leverage as they’ve had in the most recent past. Missing the market hurts, and waiting for a price to get aligned with the trends of the market hurts even more. Just ask the “Eventual Sellers” shown in the charts below, the majority of whom sold below their original list price and sat on the market upwards of two months longer than the “Very Successful Sellers.”

List Price Matters

Source: BrightMLS

Plan for Success

What can a seller do to ensure they land in the “Highly Successful” camp? The first step is to work with a licensed Realtor® who will provide local market insight and guide your pricing strategy. The second is to prepare your home to attract the most qualified buyers: fix, remodel, and paint for the best first impression, and consider offering credits for buyers.

Finally, have a plan to make a pricing adjustment if the home hasn’t sold within 21 days, which appears to be the local “tipping point” when sales prices drop. Most experts agree that a listing that is 30 days on market without an offer is likely 3-5% overpriced. Be ready to make a pricing decision that keeps you within a competitive time-and-pricing window that keeps buyers interested.

Read more housing analysis in our Market in a Minute and Weekly Meter, and connect with one of our agents to find the best strategy to very successfully sell your home!

Karisue Wyson

Karisue Wyson is the Director of Education for Corcoran McEnearney and was previously a Top Producer Realtor® in the Alexandria Office.

Visit corcoranmce.com to search listings for sale in Washington, D.C., Maryland, Virginia, and West Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Let’s Get Moving! Expert Tips To Smooth the Journey Home

THE Team from Town & Country Movers joins us this week for tips on a smooth move.

Moving can be the most stressful part of buying or selling a home, but it doesn’t have to be.

The spring market is one of the busiest times for everyone associated with real estate, with Realtors® and their clients managing many different aspects of a sale or rental and interacting with many different vendors along the way. And given that the typical homeowner stays in their property for about 12 years, it’s not unusual to have questions about how to prepare for a major but infrequent life event: moving.

At Town & Country Movers, we understand the stress that comes with relocating and we believe that a smooth and stress-free move starts with a plan and the right team to help you get things moving. We’re a local, family-owned business that has been providing clients concierge-level service throughout DC, Maryland, and Virginia since 1977 and we’ve learned a lot over the years about the best strategies to get folks settled into their new homes.

If you’re planning a move to a new home either locally or out of the region, here’s what to think about as you vet and choose the professional moving company that’s right for you.

Local Moving: How to Select a Mover

From a couple of local college kids with a truck to nationally-recognized brands, you have many options for who will handle your move so it’s important to know what to look for as you’re researching moving companies. Start first with their experience and expertise:

- Are the crews full-time, professional movers? You’ll want to know that they have dedicated personnel who have had background checks, and who will arrive on time and fully staffed so not a minute is wasted in getting your household packed up. Find out if there is a point-person on site that you can communicate with to ensure all logistics are covered.

- Are they experienced in moving specialty items? If you have an impressive art collection, uniquely-sized furniture, or large items like a piano, make sure you choose a mover who has the right equipment to deliver these items safely.

- Do they offer packing assistance? This is time-consuming work and requires extraordinary care to ensure your goods are delivered safely to their destination. Save yourself time by choosing a mover who includes packing assistance in their services, at the very least for your breakable items. It will be money well spent!

Speaking of money well-spent, ask how your mover about their fees and how they are paid:

- Is a deposit required? Clarify upfront whether the company requires a deposit before the move, and if so, what their payment terms are. Legitimate movers will provide you with a clear, written estimate, which includes the total cost and any upfront deposit required.

- What is the pricing structure? Do they charge by weight, distance, time, materials, or is it a flat fee? Get a breakdown of all potential charges so that you aren’t surprised by additional fees like disassembling/assembling furniture, using stairs, or specialized handling.

- What forms of payment do they take? Reputable movers will be set up for credit card payments, but some may offer discounts for cash. Remember that some moving expenses are tax-deductible so you’ll want to get receipts for all payments.

And while experienced movers will take every precaution to ensure the careful handling of goods, accidents happen. Find out early what the company will do to compensate you if the worst-case scenario happens:

- What happens if there’s damage? Ensure that the moving company has liability coverage and clear policies for handling any potential damages to your belongings during transit. Movers may also provide you with worksheets to help you value your items for insurance purposes. This guide from the Department of Transportation offers statistics and other tips to keep in mind.

Long-Distance Moving: What You Need to Know

In addition to all the questions listed above, a long-distance move requires a bit more investigation and logistics. Here’s what to consider:

- Does the company manage your move from start to finish? Ask if the company provides end-to-end service, or if your belongings will be transferred to a different company or a different truck during the move.

- What are the delivery terms? Understand when and how your belongings will be delivered. Will your items arrive in one trip, or will they be stored temporarily at a facility?

- Who assists on delivery? Ensure that the company uses trained, professional movers at the delivery location. It’s also important that any movers assisting with the unloading have had background checks for your safety and peace of mind.

- How is the long-distance move priced? Long-distance movers may charge based on weight, distance, and packing requirements so get a clear estimate based on the specifics of your move.

- Will you have a single point of contact throughout the move? A moving company with a dedicated point of contact makes communication easier and ensures you’re always in the loop.

Why Choose THE Team, Town & Country Movers?

At Town & Country Movers, we believe in providing concierge-level service that makes your move as easy and stress-free as possible. Our team is composed of three women with nearly 35 years of combined experience in the moving industry. We pride ourselves on offering one point of contact from the very first call to the final unloading of your belongings.

Amy, Sarah, and Errin

Town & Country Movers, Inc.

703-216-1977 direct

THETeam@townandcountrymovers.com

Visit corcoranmce.com to search listings for sale in Washington, D.C., Maryland, Virginia, and West Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Your Mortgage Closing: What to Expect and How to Prepare

Bill Stern of CMG Home Loans joins us this week for a mortgage update.

Your offer has been accepted, you’ve sent your earnest money in, and you’ve started working with your trusty mortgage team whose goal is to get your loan through underwriting and fully approved for your closing. Congratulations!

But along the way, you’ve heard a lot of financial terms bandied about, and you’re feeling a little overwhelmed by all the “mortgagese” used in this industry. Ready for an overview of your loan closing process to help clear things up? Let’s jump right into it!

Understanding Mortgage Terms

During your home closing process, it can be tricky to wrap your head around all the jargon and terms, especially for first-time home buyers. What’s PMI? DTI, LTV, CTC, CD, so many acronyms to keep track of! Below are a few important terms to keep in mind:

- Loan-to-Value Ratio (LTV): An LTV ratio is calculated by dividing the amount borrowed by the appraised value of the property, expressed as a percentage. An LTV of 80% means the mortgage loan is for 80% of the value of the property, with the borrower making a 20% down payment

- Debt-to-Income Ratio (DTI): Your DTI ratio represents the total amount of debt you owe compared to the total amount of money you earn each month, measured as the percentage of your monthly gross income that goes to paying your monthly debt payments

- Example: If your gross monthly income is $6,000 and your debt adds up to $2,000 a month, you divide the debt by your income. Therefore, your debt-to-income ratio is 33 percent ($2,000 is 33% of $6,000)

- Clear to Close (CTC): The golden term in mortgage closing, CTC essentially means that underwriting has greenlit the loan for closing

- Private Mortgage Insurance (PMI) and Mortgage Insurance Premium (MIP): PMI is mortgage insurance required on Conventional Loans with a down payment below 20%, which is added on as a portion of your monthly mortgage payment. MIP is the mortgage insurance required on all FHA Loans, regardless of the size of your down payment. There’s both an upfront premium (UFMIP) and an annual premium payment

- Closing Disclosure (CD): Your initial CD is a breakdown that includes fees like your purchase price, loan fees, estimated real estate taxes, title costs, insurance, closing costs, and various other expenses besides – and note: you must sign the CD three business days prior to closing!

The Step-by-Step Process

Simply, here’s a quick snapshot of your mortgage closing process, easily laid out in these 6 steps:

- Loan Processing

- Underwriting

- Conditional Approval

- Clear to Close

- Closing

- Loan Funding

Homeowners Insurance

It’s vital to set up your homeowners policy with a reliable insurance agent. Your closing could be delayed if your policy isn’t created with the correct information as underwriters often have strict requirements for property home coverage. It’s for a good reason – they want to ensure your home is fully insured. Your insurance requirements could be even steeper if you live in a flood zone, which will require you to obtain flood insurance separate from your regular homeowners policy. Here are a few important insurance items that your agent will need to provide us ahead of time:

- Policy declaration page or binder providing 12 months of coverage

- Invoice or paid receipt

- Replacement Cost (noted on policy) or a separate Replacement Cost Estimator (RCE) document

Please Note: If your closing date does move up, even by a day, be sure to call your homeowners insurance agent to adjust the policy periods. Your policy period cannot start after your closing; it can start up to 15 days before your closing but never after.

Title Insurance

Title insurance offers protection from problems with a property’s title, including liens, ownership disputes, and encroachments. It’s a safeguard for both the lender and the home buyer against potential issues with the deed once it’s transferred from the previous owner. As the lender, we will request this and update the old title insurance with our mortgagee clause and your information. On top of the title policy, we receive the Closing Protection Letter (CPL), the title invoice, and the Wire Instructions.

Your Closing Date

It seems simple: you’ve received CTC, you’ve signed your closing disclosure three days prior to your closing, and your closing date is set with the title company and the sellers – you’re ready to move! What else is left to do? We just ask that you set realistic expectations, even at this final stage. Maybe the seller needs to move up or push back the date for various reasons. Delays can happen at any stage. We also ask that you try not to move your own closing date willy-nilly. You may need to update your insurance policy’s effective dates, for instance. We may also need to re-verify your employment if the closing gets pushed back. These are important things to keep in mind!

We hope you now feel ready to take on homeownership since we’ve ironed out some of the details of the loan process itself. You’ll have a dedicated team working with you throughout the loan processing period, so if you need anything clarified or re-explained, we’re here to help you every step of the way.

Bill Stern | The Stern Team

Branch Manager | NMLS ID # 267577

CMG Home Loans | NMLS ID# 1820

M: 540-222-0164

bstern@cmghomeloans.com

Notice: This is an advertisement and is not a commitment to lend. Contact a loan officer today to explore the financing options specific to each borrower.

Visit corcoranmce.com to search listings for sale in Washington, D.C., Maryland, Virginia, and West Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

When Is The Best Time To List My Home?

Across the country, sellers are consulting their calendars to land on just the right time to list their properties.

Just like the temperature, the spring real estate market is heating up in our region, and buyers are anxious to get in on the action. Limited inventory still favors sellers, but there are strong signs that more homes will continue to be added, allowing buyers a better chance of finding a home that meets their needs.

It’s not a secret that the spring market is the busiest of the real estate cycle, but unlike local declarations of the change in season – “the first pitch of Nationals baseball” or the “first blooms of the Tidal Basin’s cherry blossoms” – there’s no clear date that sellers can peg for “The Best Day” to list their home. Locally, the “spring market” is loosely defined by many agents as “between the Super Bowl and Memorial Day,” which is pretty broad. If you’re looking to move soon and you can be flexible about your listing strategy, here’s what to consider.

Realtor.com’s annual “best time to sell” analysis identifies April 13-19 as the ideal new listing window based on seasonal trends in pricing, demand, and days on market (DOM) seen over the past seven years. But Zillow pushes their ideal date further out and predicts that, based on 2024 data, sellers who listed their home in the last two weeks of May netted an additional 1.6% on the sale, about $5,600 on the typical U.S. home.

Because all real estate is LOCAL, let’s take a look at the trends in our region, with the disclaimer that the best time to list your home is…when you need to move! Life changes can happen at any time, necessitating a move when you may least expect it. Factors like rising or falling interest rates (ex: higher interest rates are likely to keep would-be sellers in their current homes), consumer confidence, and the impact of cuts to the Federal workforce can also influence local market activity, throwing a potential curveball at well-crafted listing plans.

“In general, April and May tend to have the most available inventory, with March and June close behind. Same goes for new listings coming on the market,” says David Howell, CIO and a Principal of Corcoran McEnearney. “But it’s important to note that the relative supply doesn’t change as much as the actual inventory. And that’s because there are more buyers in the spring as well. So, the supply of homes – inventory and contracts – is only a little lower in the spring than it is in the winter months.”

“That wasn’t always the case,” says Howell. “Many years ago, we could count on the market being very quiet from Thanksgiving through most of January. But as our market grew more culturally diverse, the traditional seasonality waned to some degree.”

Another regional influence is the high number of military installations and the servicemembers who keep them operating, but even that impact is shifting from a spring/summer impact to one that is increasingly spread out over the year. “The summer months were always the biggest for military moves, but PCS (permanent change of station) moves in the military are now typically three years rather than two like they used to be, decreasing the number of moves military personnel would make,” Howell explains.

“What moves the market far more than the seasons is geography and major economic indicators – like mortgage rates and unemployment,” he adds.

As we head toward what could be peak Selling Season, what are the stats telling us about what to expect? BrightMLS, the mid-Atlantic database of real estate transactions, reports that year-to-date, new listings are up 10.4% in the D.C. region, compared to 4.8% for the overall Bright MLS service area. (This is higher than last year but is 5.3% lower than listing activity in the week prior.)

BrightMLS also reports that for the week ending March 23, the increase in local inventory is encouraging sellers to lower their prices, with the share of sellers dropping their asking price now two percentage points higher than it was a year ago. It had been anticipated that DOGE would cool housing market activity in the greater Washington, D.C. area, but BrightMLS reports that the uptick in new listing activity has drawn some sidelined buyers into the market.

“In the spring market, homes tend to go under contract about 10-15% faster, likely influenced by a combination of better weather that makes it easier to see and show houses and the simple fact that there are more buyers in the spring,” says Howell.

Sellers who are preparing to list soon should expect some negotiation from buyers who see, maybe, not “bargains” but “opportunities” with more homes to choose from. Buyer activity was relatively stronger in the D.C. area market than in other parts of the Mid-Atlantic region last week, with pending sales activity the strongest in the local markets where listing activity has increased the most.

If you’re planning to list within the next month or two to capture excited buyers and stand out from the competition, working with the experienced Realtors® at Corcoran McEnearney who understand the nuances of our local market will ensure your real estate goals are achieved no matter what season you’re selling.

Karisue Wyson

Karisue Wyson is the Director of Education for Corcoran McEnearney and was previously a Top Producer Realtor® in the Alexandria Office.

Visit corcoranmce.com to search listings for sale in Washington, D.C., Maryland, Virginia, and West Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

What You Don’t Know About Flood Risk Can Cost You

The seasonal transition to spring rains brings a risk of flooding, but smart homeowners and buyers know how to navigate potentially troubled waters ahead.

Pop Quiz! True or False?

- Question 1: Homeowners insurance covers flood damage.

- Question 2: Flood insurance will cover the repair or replacement cost of a home, regardless of the property value.

- Question 3: If my home is damaged by a flood, I will get Federal assistance.

- Bonus Question: Sellers have to disclose if a property is in a flood zone.

The answer to all three of those questions is FALSE, and the answer to the Bonus Question is … “Probably not.“

According to the National Association of Insurance Companies (NAIC), flooding is the most frequent and expensive natural disaster in the United States. Climate change is exacerbating the risk of flooding as more frequent and violent storms and hurricanes are impacting areas that rarely see flooding, like the September inland disaster caused by Hurricane Helene moving across the southern Appalachian Mountains – devastating parts of Georgia, Tennessee, Virginia, and the Carolinas.

As we spring into flood awareness season, it’s important to understand the logistics of determining whether you need flood insurance, how to acquire it, and what it covers in the event of a claim. Flood insurance can be very expensive – one inch of water can cause $25,000 worth of damage, according to data collected from the Federal Emergency Management Agency (FEMA) – so it makes financial sense to investigate whether a property is at risk for flooding. However, where to get that information varies based on where the property is located.

How To Uncover Risk

Sellers in DC must disclose if their property is in a flood hazard area or special flood hazard area (SFHA) on a Seller’s Disclosure Form that is provided to buyers, while Maryland sellers are only required to disclose whether water stands on the property for more than 24 hours after heavy rain and whether or not the property is located in a flood zone. Virginia sellers don’t need to make any representations about whether a property is in a flood hazard area unless the property has been deemed a “repetitive risk loss,” meaning the property has had two or more claims of $1,000 or more paid by the NFIP within any rolling 10-year period. West Virginia has no seller requirements for disclosing flood risk at all, one of 21 states without any obligation to inform a buyer of this potential hazard.

Therefore, it is up to buyers to conduct a due-diligence review of the property, and they can start by reviewing FEMA’s flood maps or state-specific resources like these for Virginia, DC, Maryland, and WV. Buyers should also look for guidance from their lending institutions, who will most likely require flood insurance as part of a mortgage.

How to Get Insured

Homeowners insurance policies do not cover flood damage so owners will have to secure a special flood policy. Some of these policies may be privately insured, but most flood insurance comes from the National Flood Insurance Program (NFIP), a public-private partnership between the federal government, the property and casualty insurance industry, states, local officials, lending institutions, and property owners. It was created by Congress in 1968 to provide insurance to help reduce the socioeconomic impact of floods to property owners, renters, and businesses.

Start with your preferred insurance company for guidance on securing coverage as they may already be connected with the NFIP. According to FEMA’s last update in 2019, the average flood policy cost to consumers was about $700, but, depending on the value of the property, an owner may need to get an additional private policy outside of their insurance company as the NFIP only covers up to $250,000 in repair costs and up to $100,000 for contents coverage. Private insurance may not be available in all states, and more restrictions are happening each year as climate change disasters push premiums ever higher and force insurers to leave some coverage areas completely. Federal programs in the event of natural disasters rarely come close to covering actual repair or recovery costs, generally providing just $3,000-$6,000 for individual grants.

Keep in mind your flood insurance coverage might not automatically renew so be sure to check your renewal date to ensure the premium is covered. Flood policies take 30 days after registration to become active so the time to get a policy in place is NOW.

The National Association of Realtors® (NAR) estimates that the NFIP is essential to 1,360 home sale closings daily, translating to approximately 41,300 affected monthly transactions nationwide. If you’re in the market to buy a home, connect with one of our expert Corcoran McEnearney Agents who will advise you on the best way to protect your purchase, no matter what storms may lie ahead.

Visit corcoranmce.com to search listings for sale in Washington, D.C., Maryland, Virginia, and West Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Real Estate Taxes in the DC Metro Area: What Homeowners and Investors Need to Know

Real estate taxes are an important consideration for anyone looking to buy property or invest in real estate.

For those in the Washington, D.C. metro area, understanding the region’s tax landscape is crucial, as the area encompasses multiple jurisdictions with different tax rates, rules, and regulations. Whether you are already a homeowner, a prospective buyer, or an investor, knowing how property taxes work can help in financial decisions regarding property ownership.

Real estate taxes are local taxes levied on the value of land and buildings. They are collected by city or county governments and are a primary funding source for local services such as schools, public safety, roads, and parks. Property taxes are calculated on the assessed value of the property and the tax rate set by the particular taxing jurisdiction.

In our region, there are distinct tax regimes (e.g. state, county, and city) to consider since the area spans multiple jurisdictions – Washington, D.C., suburban Maryland, and Northern Virginia. Each jurisdiction has its own approach to real estate taxation, which can lead to significant differences in tax rates and policies. Generally, across our local jurisdictions there is a process for assessing the value of real property and then applying a tax rate, which is typically set by the jurisdictional government each spring.

Real Estate Taxes in Washington, D.C.

Washington, D.C., has its own independent property tax system. The city assesses the fair market value of the property, and imposes taxes on the property to help fund services, including public education, emergency services, and infrastructure.

Washington, D.C., imposes different tax rates on residential property and commercial property. As of 2024, the residential real estate tax rate in D.C. was $0.85 per $100 of assessed value. This means that for every $100 of assessed value, homeowners paid $0.85 in property taxes. The tax rate for commercial properties in D.C. is higher than for residential properties, standing at $1.85 per $100 of assessed value. This rate applies to properties used for business purposes.

Real Estate Taxes in Maryland (Suburban DC)

In Maryland, property values on residential property are typically assessed every three years. The assessments are conducted at the local jurisdictional level and overseen by the State Department of Assessments and Taxation (SDAT). The local governments of Montgomery and Prince George’s counties establish their own tax rates applied to each $100 of assessed value. Montgomery County is one of the largest and most populous counties in Maryland, and its real estate tax rates are among the highest in the state. As of 2024, the real property tax rate in Montgomery County was $1.04 per $100 of assessed value for residential properties.

In addition to the standard real estate tax, Montgomery County property owners may also be subject to a fire and rescue tax for properties located in certain districts. This tax is typically a small percentage of the property’s assessed value and is used to fund local emergency services.

Prince George’s County has a slightly different property tax rate. As of 2024, the real estate tax rate in Prince George’s County was $1.10 per $100 of assessed value for residential properties. Much like Montgomery County, Prince George’s also levies additional taxes for specific services, such as fire and emergency services, and may have different rates for commercial properties. It is prudent for prospective property owners to check with the local tax authority for any additional taxes that may apply.

Real Estate Taxes in Virginia (Northern Virginia)

In Virginia, real estate taxes are imposed on the fair market value of real estate as of January of each calendar year. Tax rates vary by locality. Some of the major Northern Virginia counties include Arlington, Fairfax, and Loudoun, in addition to the independent City of Alexandria. Like the other jurisdictions in the metro area, each county in Virginia establishes its own tax rate and to some degree its tax regulations.

Arlington County is known for its proximity to Washington, D.C., and is home to many government employees and young professionals. As of 2024, the real estate tax rate in Arlington County was $1.013 per $100 of assessed value. Arlington has an additional stormwater tax, which is designed to fund the local stormwater management system. The amount varies depending on the size of the property and its impact on the county’s stormwater infrastructure.

Fairfax County, the largest jurisdiction in Virginia by population, has a higher real estate tax rate than Arlington County. The 2024 tax rate in Fairfax is $1.14 per $100 of assessed value for residential properties. Like other localities, Fairfax may have additional taxes for special services such as fire protection or emergency services, depending on the specific area within the county. The City of Alexandria, an independent city within Virginia, has a tax rate that is distinct from the adjacent counties. As of 2024, the real estate tax rate for residential properties in Alexandria was $1.11 per $100 of assessed value.

Loudoun County’s tax rate for 2024 was $1.085 per $100 of assessed value. Loudoun historically provided certain exemptions for different land uses, such as agricultural, but residential development continues to decrease the instances of these exemptions.

Property Tax Appeals and Exemptions

If you feel that your property’s assessment is too high in any of the jurisdictions in the DC metro area, you have the right to appeal the assessment. Each jurisdiction has a formal process for appealing property tax assessments, and it usually involves providing evidence, such as recent appraisals or sales of similar properties.

Additionally, some jurisdictions offer property tax exemptions and credits for qualifying homeowners. For example, D.C. offers a homestead deduction that allows homeowners to exempt a portion of their property’s assessed value, reducing their overall tax burden. Similarly,

Maryland and Virginia offer various tax relief programs for seniors, disabled persons, and certain Veterans.

Local property tax payments are due twice each year, although the due dates vary from jurisdiction to jurisdiction. If a property is encumbered by a mortgage, the mortgage company may require 1/12th of the annual tax liability be included in the monthly payment, which would be placed in escrow, allowing the mortgage company to make the semi-annual tax payment to the appropriate jurisdiction. Most mortgages are set up to require a tax escrow payment, though a conventional mortgage may not require a tax escrow if the loan amount falls below a specific loan-to-value.

Taxes help fund the services in our communities and it’s important to understand how they are collected and what they are used for. If you’re interested in understanding how taxes will affect your home affordability scenario, reach out to me or anyone on the Atlantic Coast Mortgage team to learn more.

Brian Bonnet, SVP, Sr. Loan Officer, NMLS ID 224811

Atlantic Coast Mortgage, NMLS ID 643114

O: 703-766-6702 | M: 703-304-0188

Email Me

Notice: This is an advertisement and is not a commitment to lend. Contact a loan officer today to explore the financing options specific to each borrower.

Visit corcoranmce.com to search listings for sale in Washington, D.C., Maryland, Virginia, and West Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()