Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Is There Evidence of a Flight to the Suburbs as a Result of COVID?

1849 Kalorama Rd NW, Washington, DC | Keith Milne

Ripple, Wave or Tsunami – Part II

By David Howell, Chief Information Officer, McEnearney Associates

In September we took our first look at comprehensive data to see whether there is evidence of “a flight to the suburbs” in the wake of COVID-19, wondering whether urban dwellers were seeking more elbow room and retreating from more dense living conditions. Two months ago, we said that any movement looked more like a ripple or a wave, and most certainly not a tsunami. With the passage of time and more data to examine, we’re seeing a ripple at best.

If significant movement were to occur, it would first appear in the market for condos and co-ops in Washington, DC. We took a look at the performance of that market from May 1 (when shutdown orders began to be lifted) through the end of October of this year and compared it to the same time last year. We also compared the condo/co-op market to attached and detached homes in DC to provide some additional context. Here’s what we found:

- There was actually a 20% increase in the number of newly ratified contracts on condos and co-ops. That’s actually better than attached homes (up 17%) and detached homes (up 11%).

- Most other key metrics – the average number of days on the market, sales price to list price ratio, and the percentage of homes with a price change before receiving a contract – very closely mirrored that of last year.

But that doesn’t mean there haven’t been changes in the market. The biggest shift has been in the types of condos and co-ops being purchased, and in the inventory of units on the market.

- The number of studio units – no bedrooms – going under contract fell by 15%, and the average inventory doubled.

- One-bedroom unit contracts rose by 8%, and inventory rose by 30%.

- Two-bedroom unit contracts rose by 30%, and inventory rose by 30% as well.

- The largest shift was seen in the biggest units – those with 3 bedrooms or more. Contract activity was up 42% while average inventory was up only 6%.

What does this mean? In general, the market for smaller units is softer, as demand has remained relatively flat while inventory has climbed. This suggests that more unit owners would like to leave behind those smaller units – and that means that prices are softer as well. This may also suggest that at this end of the market COVID has negatively impacted employment, so there are fewer buyers. The market for 2-bedroom units has changed with the increase in demand, but there has also been an equivalent increase in inventory, so the overall relationship between supply and demand is really unchanged. Yet the market for 3-bedroom and larger units (only about 13% of the overall condo market) is actually stronger than last year, with modest upward pressure on prices.

And to provide some additional context, while inventory of condos and co-ops is considerably higher than last year, the reverse is true for attached and detached homes in DC. The average month-end inventory of attached homes is down 40%. And since contract activity is up 17%, there is considerable upward price pressure as more buyers are competing for much thinner inventory. The same is true for detached homes in DC. Average inventory is down 54%, and with an 11% increase in the number of buyers, prices are climbing.

The softer condo market combined with a much stronger market for attached and detached homes in DC does suggest a modest shift in the most urban of the markets in the metro area to buyers looking for larger quarters, but there is no evidence of a big rush to the suburbs.

Check back with us soon for a similar look at the numbers in suburban Maryland and Northern Virginia.

[divider height=”30″ style=”default” line=”default” themecolor=”1″]

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

What is the Top Contributor to Household Wealth?

The top contributor to wealth in the United States IS homeownership, according to the National Association of REALTORS®. Unsure of taking your statistics from a trade organization? Well, U.S. Census researchers found that the biggest determinants of household wealth are owning a home, followed by a retirement account.

Visit the most recent “Survey of Consumer Finances” conducted every three years (last in 2019) by the Board of Governors of the Federal Reserve System — a federal agency and HQ of the nation’s central bank. They’re tasked with surveying the public to gain an understanding of the financial condition of U.S. households and to study the effects of our ever-changing economy. They consistently share data that the net worth of a homeowner is more than 40x greater than that of a renter!

No matter where you look, the data unwaveringly shows that buying starts most consumers on a path toward financial freedom. Of course, there are other ways — but buying property “forces” an owner into saving. As a homeowner makes their mortgage payment each month, they slowly realize gains in equity. While markets do ebb and flow, holding a property for long enough also means realizing gains in equity as values rise.

But, buying a home can be ridiculously challenging in our region. A buyer must go in with eyes wide open and a good strategy to make the most of this herculean effort. The good news? Buying is not impossible. The equity gains and tax write-offs start early on in ownership and continue. Plus, in a pandemic year when people want more control of their space, it may now even be among the strategies for staying healthier — who knew that would be a benefit of homeownership?

So, what does a buying strategy look like? The founder of McEnearney Associates, John McEnearney said that the three most important things to consider when buying are: Location, location, location. Buy where others want to buy or where you see upward trends. Yes, that means competition, but once in, it means greater gains.

Look at Alexandria and Arlington right now — the “Amazon Effect” has made inventory a trickle of what it once was (in fact, to look at it graphically, the stranglehold following the November 2018 announcement about HQ2 is very obvious). There’s a mad scramble of contract activity for good property. Imagine throwing breadcrumbs into an over-crowded duck pond and be careful not to lose your hand!

Start by meeting with a good realtor and locally-based loan officer (personally, I believe in the power of referrals to locally-based businesses — ask friends and family who they used). Read, listen, and learn. Buying a home is a process, like anything else, and there are LOTS of moving parts.

Carefully analyze your income. Consider not only the mortgage but potential maintenance or repair costs and rising utility and property tax costs. When meeting with a loan officer, instead of asking what you’re approved to purchase, back into the numbers — share what you’re comfortable paying monthly and then see what that, paired with your down payment, will buy you.

Think about your lifestyle… Consider commuting options and travel along with nearby major arteries/transportation hubs. While traffic is less than it used to be, it’s still a big factor. Do you like to be closer to the city and able to mosey over to the local coffee shop to enjoy a socially-distant cup of java with friends? Maybe you enjoy birdsong while looking over a generous lawn and watching the sunrise and deer meander. Don’t buy where you’ll hate living — trust your instincts. Stats and facts are great, but you need to like living there and coming home to what makes you feel happy and restored.

I’ve heard it argued that buying means a loss of freedom — you can’t just pick up and go. What’s great about owning in Northern Virginia and the D.C. Metro area is that you often CAN just pick up and go. We’re in a very transient area — people come and go all the time — whether that means a need for short-term rentals or the longer-term lease…

Contractors, military, state department, researchers and others move here regularly and need housing. What if the little condo you bought becomes a money-making investment for you while you channel your inner David Letterman and leave the big city for a fly-fishing adventure in Whitefish, Montana?

Buying is good. The process is hard, but worth it. It gives you options and financial freedom and that investment in your future is nearly priceless!

Ann McClure is a licensed real estate agent in Virginia and Maryland with McEnearney Associates, Inc. in McLean, VA. If you would like more information on selling or buying in today’s complex market, contact Ann at 301-367-5098 or visit her website AnnMcClure.com.

Take a look at our website for all of our listings available throughout Washington, D.C., Maryland, and Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

What Defines Mid-Century Modern Homes?

Colonial, split-level, Cape Cod… it’s no surprise that real estate has its own lingo, right down to the style of a home. In an effort to establish a deeper understanding of home styles, both in terms of how they’re built and what they seek to represent, McEnearney presents a series of articles to explore these differences. We’ll explain what makes a home a split-level versus a split-foyer, define traditional Colonials and Cape Cods; and learn to appreciate the subtleties of Art Deco and Victorian details. Third in our series is exploring the well-liked mid-century modern style of homes. Missed Parts I and II? Click here (Townhouses vs. Rowhouses) or here (Bungalow vs. Cape Cod).

A style of design that has seen a resurgence in popularity is mid-century modern, which extends beyond furniture and decor, but to architecture, as well. Interest in the style began to pick back up in the 1990s, as adults who had grown up in MCM-designed homes were reaching adulthood and buying houses they associated with their childhood. Coupled with the explosion of the hit television series Mad Men, the classic design shows no signs of fading.

Mid-century modern architecture refers to the wave of homes built between the end of World War II in 1945 and the mid-1970s. Following WWII, Americans were moving to larger plots of land in the suburbs and building open-concept homes on a single level. This, along with inspiration from Frank Lloyd Wright’s Prairie School design and a desire to incorporate nature via indoor/outdoor spaces, which flowed from one to another effortlessly, influenced the mid-century modern movement.

In the DMV area, MCM-style homes can be found in numerous neighborhoods including Hollins Hills (Fairfax), Carderock Springs (Bethesda), and Holmes Run Acres (Annandale).

If you’re looking for a MCM-style home, here are three key elements to look for:

One-level, and open-concept in design.

MCM homes are generally one-level with an open-concept layout, have expansive panes of glass (instead of traditional windows) and large sliding glass doors, and low-pitched or flat roofs.

Bringing the outdoors in.

MCM homes seek to make the home a part of the nature around it. Builders sought to bring in a lot of natural light and materials in the interior spaces, via exposed beams, wood-paneled walls or stone fireplaces. Some also literally brought the outdoors in with interior courtyards or atriums with glass walls. Sliding glass doors and expansive windows were incorporated to provide scenic views and encourage occupants to go outdoors.

Simplicity over extravagance.

MCM is the opposite of fussy; look for clean-cut, no frills lines and edges, sight-lines that allow for homeowners to be a part of what’s happening around them (as opposed to the spaces being separated by walls) and features that serve a purpose, rather than for decoration.

Want to find a mid-century modern home of your own? Contact your favorite McEnearney Associate to start the conversation today.

[divider height=”30″ style=”default” line=”default” themecolor=”1″]

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

3 Key Steps to Winning The Offer When Purchasing a Home

The DC housing market is competitive. A lot of the more desirable homes in our area have bidding wars where multiple offers are laid on the table, and the seller gets to pick the one that they think is best. As a buyer, you don’t want to lose out on your dream home because you were unprepared. That is why I always discuss these three things with my clients before we make an offer on a home.

Determine Financing

There are a couple of questions that you should know the answer to before making an offer on a property. For example: Do I need to sell my house in order to buy a new one? Do I need to move money around in order to have enough money for the down payment? If I do that, will there be tax implications? What are the closing costs going to be?

A great lender can help you answer all of these questions and more. It is important to talk to one before even beginning your house search. This is probably the largest purchase you will ever make in your life, and most people take out a loan in order to do it. You want to be secure in knowing what level of home you can actually afford based on your monthly income. In fact, a pre-approval letter from a lender will almost always be required when making an offer on a property.

Your Realtor can connect you with a lender if you don’t know where to start looking. After all, a great Realtor has probably worked with many lenders, and some are better able to handle tight settlement deadlines and problems that occur during underwriting than others. Financing problems have caused many contracts to fall through. You don’t want that to happen to you!

Market Analysis

Most people are familiar with getting a CMA, or Competitive Market Analysis, on their home before they list it, but you should also get a CMA before buying a home. A thorough market analysis is an insurance policy on your investment. You want to make sure the home is worth what you are about to pay for it! A CMA will look at what homes in the area have sold for in the past six months as well as neighborhood trends. It also answers questions like does the list price accurately reflect this home’s value? You want to have a competitive offer, but you don’t want to overpay on a house that is not going to appreciate.

Get Familiar with the Sales Contract

A residential sales contract is a legally binding document that has the potential of costing you money or “damages” if you are in breach of the contract. This is why understanding what your sales contract means before you sign it is vital. The Northern Virginia Association of Realtors has a standard contract form used by agents throughout the region. Realtors undergo educational training to understand what each section of the sales contract means so that they can better advise their clients. For any legal questions, however, it is always best to talk to a real estate attorney.

Walking through the sales contract with your Realtor ensures that you understand your responsibilities as the offeror of the contract. Settlement date, earnest money deposit, and contingencies all have time limits so it is important that you understand what that means so you can meet those deadlines. Your Realtor will also explain what the different contingencies mean in detail, and whether or not you want to include them in the offer. A general rule of thumb in a seller’s market is that the more contingencies, the less desirable your offer.

Finally, Virginia is a “Buyer Beware” state which means that a lot of the “due diligence” for finding out the condition of the property falls on you as the buyer. For example, If you have not put your desire for inspections in the sales contract, the seller is not obligated to allow you access to the property to perform them, so you could be looking at costly repairs shortly after buying your home. I would highly recommend reading the material on the DPOR website before signing the Residential Property Disclosure Form that is part of the sales contract. It will help you to understand your rights as the buyer in your real estate transaction.

If you follow these three steps, you will be confident in the offer that you present to the seller. With an experienced Realtor at your side, you will stand out amongst the crowd of buyers, increasing the likelihood of winning the contest for your dream home.

Jean Beatty is a licensed real estate agent in VA, MD, and DC with McEnearney Associates, Inc in McLean, VA. If you would like more information on selling or buying in today’s complex market, contact Jean at 301-641-4149 or visit her website JeanBeatty.com.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

To Sell My House Do I Have to Neutralize Everything?

Question: I am getting my house ready to put on the market and wanted to ask if everything really needs to be all beige or gray?

Answer: The best way to answer this question is…it depends upon the type of property, the target buyer pool, if you are using your furniture and accessories, or if it will be staged.

When I am working with a seller, my first step is to have them give me a tour of their home to discuss what they are planning to keep, move, give away or sell. We also review the paint colors, artwork, accessories and bedding. I then come back on my own and walk through the house making a list of suggested repairs, painting, modifications, items to keep in the same room, items to move elsewhere, items to put into storage, and options for staging. Then we get together to review and make decisions on how to move forward.

I generally suggest a neutral wall color throughout the house. It does not have to be the same color in every room, but a pallet that keeps the home light and bright and flows nicely from room to room. In cases where each room is a different bold color, it can be a distraction to the potential buyer and an expense that they prefer not to incur before moving into their new home.

I personally have a lime green kitchen and a hot pink master bathroom and would definitely need to make some changes before putting my own house on the market.

With neutral paint, bedding, shower curtains and towels, carpet, or in most cases furniture, you can always add color and personality with your artwork and accessories. I just sold a home in Old Town Alexandria with creamy white walls, light hardwood and tile floors, and white blinds. We used grey and white linens and white towels, and brought in large colorful contemporary art and fun accessories to make it pop! The photos and feedback were fabulous and it sold in a few days.

In another listing, the contemporary townhome had dark hardwoods, white cabinets and countertops, light grey walls and beautiful neutral tile. The furniture, artwork, and accessories were bright greens and oranges. It was gorgeous!

In other situations, however, I have worked with sellers that, like me, love colorful walls and bold artwork and accessories, and were not open to making changes. The feedback I received from potential buyers was that they could not picture themselves or their furniture in the house, and the listing lingered on the market until the price or condition was modified.

Another thing to keep in mind is that most buyers keep up with TV shows, social media, and magazines about flipping houses, before and after makeovers, and how to decorate a new home. They will feel a neutral background offers them more options.

Whether you decided to go with a completely neutral look, or one with colorful accents, keep in mind that in order to get top dollar, your home should be move-in ready.

If you would like a professional, confidential evaluation of your home, please give me a call. I am happy to meet with you, tour your home, and offer suggestions for updates, repairs, or staging prior to listing your home.

Good luck!

Lisa Groover is a licensed real estate agent with McEnearney Associates, Inc. in Old Town Alexandria, VA. Having had seven golden retrievers since moving to Alexandria in 1989, she is dedicated to helping other dog owners through the challenges of renting, buying and selling their home..

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Should I Stage My Home When I List It For Sale?

At some point in every listing appointment the topic of staging comes up. Should I stage? Is it worth the money? In a word: absolutely!

There are countless articles and statistics that speak to the return on investment for every staging dollar spent. Professional stagers know how to optimize the home’s layout and visual impact, both in photographs that attract more buyers, and in the “wow factor” you experience when you walk into the home. A well-staged home is often sold before the buyer leaves the main floor. First impressions can mean everything!

What is staging?

Staging is the process of preparing a home for sale, and it can be as simple as decluttering, or full-service professional staging. Staging can also include painting and remodeling – from a little touch-up paint to a new kitchen – it’s all staging! An investment in staging depends on the home’s condition and the means and goals of the sellers.

As a Realtor, bringing up the need for staging can be tricky. In some cases, this is likely the most uncomfortable conversation we will have with you! While we know from past experience that homes staged with fresh paint, neutral furnishings and carefully arranged accessories tend to sell faster and for more money, we know it can feel personal to be told to make these changes to your personal space. (It’s not personal!)

There are many levels and elements to staging.

Often stagers are brought in for a consult when the ink is still wet on the listing agreement to determine if painting, updating, purging, or adding furniture would be recommended. The stagers will walk through your home and make recommendations on colors, furniture placement and what needs to be removed or potentially added.

Sometimes the home furnishings will be used, but stagers might bring in accessories including pillows, lighting, art, or seasonal enhancements like pumpkins in the fall to enhance the home.

A full stage means that the stagers will bring everything into an empty home and stage the rooms that will offer the greatest impact to the sale of the home.

The first two options are relatively inexpensive. The third quickly gets more expensive and it’s easy to understand why – the stagers are decorating and moving a houseful of goods in and then out again.

Can I do my own staging?

Certainly! Agents will always recommend that you remove all personal, religious, and political items from the home. The main idea is to allow the buyer to imagine how they will live in the home (not to showcase how the seller currently lives in the home), and you don’t want to turn off a potential buyer. (Once I unknowingly showed a vegan couple a home with countless animal heads mounted on the wall! No surprise, they didn’t buy it.)

Does the home need any updating?

While new kitchens and baths help to sell houses quickly, that’s not always in the budget. Simple things like paint, fresh towels, clean filters, working light bulbs, weeded gardens can have a big impact. Maybe the bathrooms are very dated, but in good condition. Can the vanity be painted? New faucets? Sometimes a little bit of effort and creativity can improve a space without a large investment.

Time to declutter!

It’s incredible how much we can collect after living in a home for a few years or more. If you’re looking to sell your home, you’ll want to tidy up and declutter! Movers will store your things for you for a small sum or sometimes even for free if you use them to move. Purging extra furniture, seasonal items and trinkets to open up the rooms is very beneficial. Half-full closets look a lot more spacious than one crammed from top to bottom. (This may be the hardest part of the process. But by the time you have finished purging, packing, and storing, the next part of the move will be easy!)

It’s all about the photos!

When it comes down to it, much of the work of staging is to create fantastic photographs. This is especially true in today’s increasingly virtual world where buyers are doing a lot of their searching online. How a home shows online often determines if a buyer chooses to schedule a showing.

It is important to ensure the photographs are capturing what you want to buyer to look at. We want them to see the wainscoting, the moldings, the beautiful windows in the home. If the eye is being drawn to table decor or window treatments, we are “selling” the wrong thing. However, the reverse is true as well: if we want to distract the viewer from a flaw – a dated tile countertop, for example – more pieces will go onto the counter to draw your eye away.

Staging is a honed skill that takes time, experience, and talent to execute.

By professionally staging a home, the seller is creating a picture of what living in the home could look like. Good staging is not decorating, it’s actually marketing. You want the decor to enhance, but not distract. Good staging shows your home in the best possible light and will often get your home sold faster!

Rebecca McCullough has built a successful real estate business in Alexandria and Northern Virginia by providing excellent service to her clients. If you would like more information on selling or buying in today’s complex market, contact Rebecca today at 571-384-0941 or visit her website RebeccaMcCullough.com.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

What Should I Expect From a Home Inspection?

Home Inspections. So beneficial — even in a very tight inventory market. I get it, sometimes to get a house a buyer might feel they have to waive the inspection. However, I would encourage this buyer to still do a home inspection, post-closing or at least have some experts out to check major systems (HVAC, roof, chimney, electrical, and plumbing). Making the most of this time and these experts is key to successful homeownership.

Buyers, this is your opportunity to learn about your future property — the biggest investment you will likely ever make. Won’t your parents feel better knowing you inspected? All kidding aside, home maintenance is critical to both enjoying where you live and your prospects for resale down the road.

An inspection may also reveal current defects or, at the very least, items needing attention in the future. For instance, did you notice the tell-tale signs of water intrusion along the baseboards in the lower level? Or the mold-like substance on rafters in the attic? Are these signs of a current issue?

Inspectors are great resources for prioritizing projects: Needed updates, ideal upgrades and critical maintenance. Take advantage of their knowledge — learn where to spend money and where you may be able to wait, at least for now. You may even learn of alternate solutions you might not have considered or even known about, otherwise. What? You can open those painted windows with a pizza cutter? And, sealing your air ducts can increase the energy-efficiency of your home by how much? That might really save on your energy bills! You’ll find out if I install a UV light on the furnace, does it really help with allergies and other bacteria?

Get your questions answered… Why is carrying the water away from the house so important? Why does your gas furnace need a certain amount of air flow around it? Why are the expensive furnace filters maybe sometimes not as good as the cheaper ones?

What if you are buying a new construction property? Many times, I have heard of buyers forgoing inspections on a new home, but experience has taught me, just because a home is new does NOT mean it is defect-free. I once saw an independent inspector find an issue with a gas furnace that both the builder’s inspector and the county inspector missed, that could cause a potentially deadly carbon monoxide issue!

A good home inspection offers a baseline. God forbid you have an insurance claim — at least you would have written documentation of the condition your home was in should you ever have to prove it. Like the Farmers Insurance commercials, but with my twist, “Inspectors, they know a thing or two because they’ve seen a thing or two.”

Let’s play devil’s advocate… Suppose you spend several hundred dollars and have a great home inspection and very few issues are found. No, you didn’t waste your money! Congratulations — you were just validated! You made a sound investment. Isn’t that peace-of-mind worth a few hundred well-spent dollars? Your realtor must have taught you well!

Buying a property “AS IS”? Don’t you still have to know what IS is? Learn about the home and its issues and then decide if you still want to move forward. Perhaps there’s a cracked foundation. Just like leaving spoiled milk in the fridge — it won’t get any better if you just leave it. Depending on how your contract is written, you may be able to void following an inspection, so you don’t have to inherit someone else’s problem.

Sellers, you’re not off the hook. Ensure a good selling experience… Have your HVAC serviced and change those filters! Get a roof certification. Have your chimney cleaned. Check the sump-pump, clean your gutters, check your ice maker and furnace humidifier — these are frequently a homeowner’s “problem children”.

Before listing, make a list and have a handyman take care of any minor, long-overdue maintenance. Once you have a contract, be sure to clear paths to panels, HVAC, water heater and crawl spaces (inside and out) before an inspection.

Finally, just because you had an inspection doesn’t mean all issues will be found. I would average that about two-thirds may be discovered, because an inspector can’t tear open the walls (though they may use infrared and moisture meters) and they can’t pull up the flooring, etc.

Remember, depending on the terms of your contract, the process following the inspection is a negotiation between buyer and seller. Just because an issue is found does not mean the seller will address it. Knowledge is key — learn about your home, prioritize your projects to create a plan for action, and take pride in your investment. It’s money well-spent.

Ann McClure is a licensed real estate agent in Virginia and Maryland with McEnearney Associates, Inc. in McLean, VA. If you would like more information on selling or buying in today’s complex market, contact Ann at 301-367-5098 or visit her website AnnMcClure.com.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

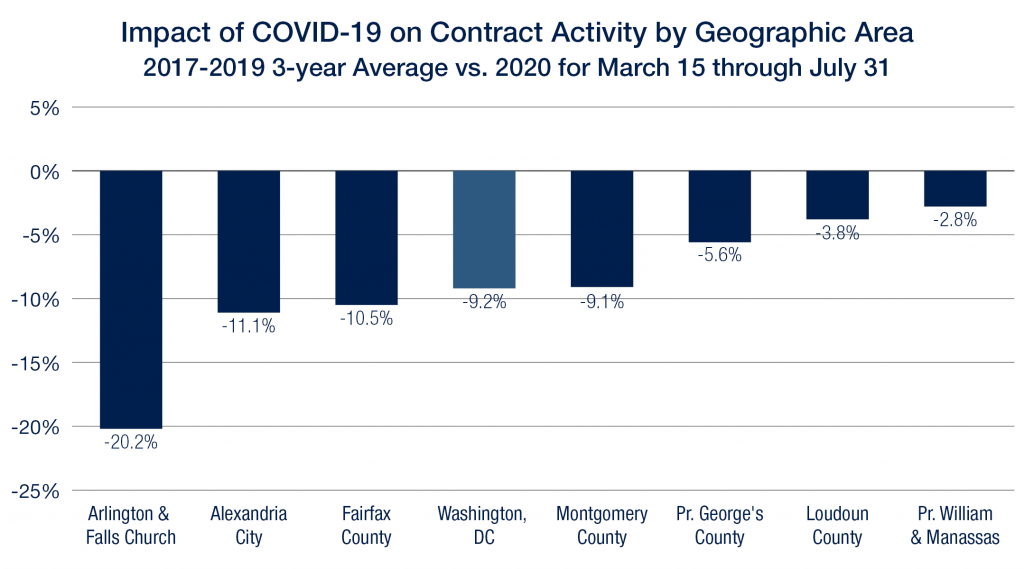

Has COVID Changed Real Estate Consumer Behavior in the DC Metro Area?

Ripple, Wave or Tsunami – Part I

By David Howell, Chief Information Officer, McEnearney Associates

There has been much national conversation that the COVID-19 pandemic has caused a “flight to the suburbs” as urban dwellers seek more elbow room. Has that happened in the metro Washington, DC market?

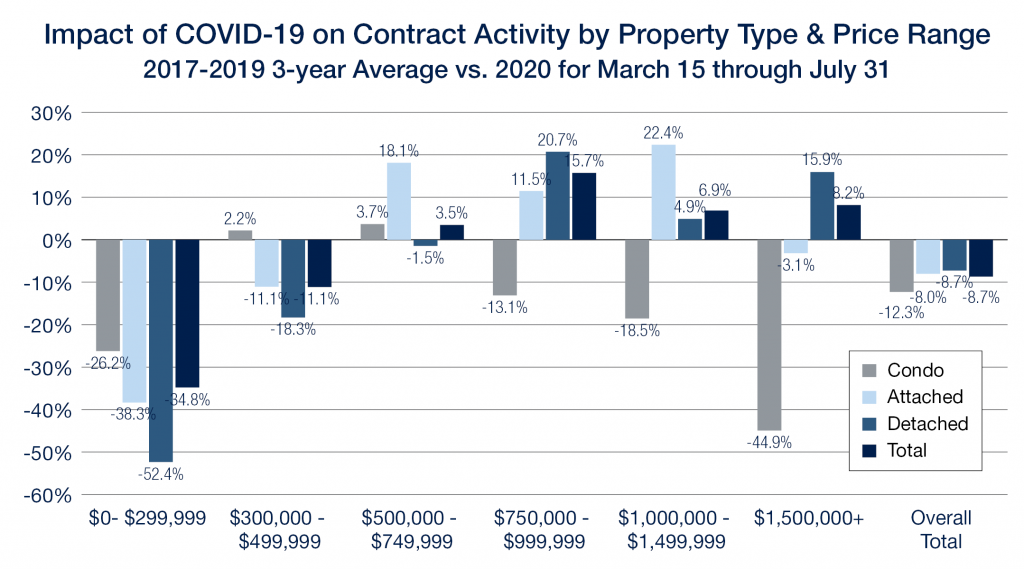

The region began to shut down in mid-March of this year, so we examined new contract activity from March 15 through the end of July for 2020 and compared that to the average activity of the same four-and-a-half-month time period for 2017-2019. As the chart indicates, there is no question that the outer suburban markets have fared better than Washington, DC and the close-in suburbs. Washington, DC contract activity is down a little over 9.2%, and Arlington is off over 20%, while Loudoun and Prince William Counties are only off between 3% and 4%. And in those areas most impacted by COVID, the condo market has been hit even harder. But there is nothing in these numbers to suggest that consumers are fleeing the city in droves. It’s not a tsunami – it’s somewhere between a ripple and a wave.

The impact of COVID has also been felt disproportionately at the lower end of the price spectrum. Job losses have been heavily concentrated in the service and hospitality sectors, and entry-level home purchases have been hit pretty hard. While the overall drop in contract activity in the region has been 8.7%, homes priced less than $300,000 have fallen by almost 35%, while activity for homes priced more than $500,000 has actually risen. Total new contract activity for condos is off 12.3%, while attached and detached homes are off 8.0% and 7.3% respectively. This is another indication that there has been some movement away from more dense living conditions, but it hasn’t been massive.

We are very encouraged by the rebound in contract activity since the middle of May, and the region’s real estate market is in far better health than we would have guessed just a few months ago. Yet a rebound and a recovery are not the same things. There is still an enormous amount of uncertainty about the future path of the COVID virus, and it will take a long time to fully replace the jobs lost and to climb out of the deep economic hole that COVID-19 has produced. We have been proud members of the Washington, DC real estate community for 40 years and continue to believe that this is the best place to live and work in the world. We are realistic in knowing that we are a long way from a full recovery, but optimistic that we will recover here better than almost anywhere.

[divider height=”30″ style=”default” line=”default” themecolor=”1″]

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Top Five Home Improvements to Enjoy Now That Pay Off Later

There are certain things that I always recommend to my clients if they are thinking of putting their home on the market in the next five years. Putting some money into updating your home now can make it more appealing to buyers down the line. It will also allow you to enjoy the updates before you finally take the plunge and move.

The following list is my top five recommendations on home improvements.

1. Spruce Up the Kitchen

Most of your time at home is usually spent in the kitchen. Between meals and snacks, the kitchen receives the most foot traffic out of any other room in the home. A full kitchen remodel can be very expensive. As an alternative, you can focus on some key areas. If your cabinets are older, but still in good shape, hire a professional painter to come and repaint them. After they have been repainted, update all the knobs and hardware to a more modern look.

Replace your old countertops with Silestone or quartz. It will bring a fresh look to the kitchen, and they don’t scratch easily, unlike granite.

If the floor is older, either replace it, refinish it, or add something on top. You might want to match the kitchen with the rest of the house. Which brings me to my next point.

2. Replace or Refinish Outdated Flooring

A general rule of thumb is to have hard surface flooring in all of the main areas of your home, especially the living room, dining room, and kitchen as most modern home buyers do not like carpet. You can choose a less expensive option like floating laminate flooring or a more expensive option like engineered or solid hardwood floors depending on your budget.

If you already have hardwoods in your home, and they are refinishable, it might be time to update the color scheme to something more modern. The current trend is to have darker, matte flooring. If you need ideas for colors or simply don’t know where to start, attend an open house at some new builds in your neighborhood and ask them what flooring they used. Model homes usually showcase the current trends, and builders always have a list of materials that they used.

A word of caution, if you are going to replace the flooring in your home, do not mix flooring types. At least not on the same level. The change between different flooring is like a full stop for your brain. It can make a room seem smaller than it actually is.

3. Update the Bathrooms

It is relatively inexpensive to replace the vanities and toilets in your bathrooms. Also, hiring a contractor to re-glaze the tile and bathtub, especially if they are older or an odd color, is a great way to get more use out of what you already have, while making your bathroom seem like new again.

4. Add Recessed Lighting

If your home is older, it might not have as much recessed lighting as more modern builds. Adding recessed lighting to your home will add to the overall mood and functionality of your home. Since it requires working with circuits and electrical wires, I would strongly recommend hiring an electrician. Not only do buyers like well-lit homes, but it will also help with your marketing as light is essential for great photographs. Most home buyers start their search on property websites like Zillow or Realtor.com, and professional photographs help make your home stand out while highlighting the best features to potential buyers.

5. Replace the Roof

If your roof is less than 10 years old, it is a huge selling point for the home. A new roof prevents leaking, water damage, and a host of other problems. I realize that this item can get very pricey, so consider contacting a roofing company to come out and take an assessment. If they find hail damage, they can work with your insurance company to get it replaced for the cost of your deductible.

Looking toward the future and starting now is the key to a smooth, easy home sale later. To get the most out of your home, consider making these improvements today so you have time to enjoy them. If you are thinking about making a move, reach out to me to discuss next steps.

Jean Beatty is a licensed real estate agent in VA, MD, and DC with McEnearney Associates, Inc in McLean, VA. If you would like more information on selling or buying in today’s complex market, contact Jean at 301-641-4149 or visit her website JeanBeatty.com.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Senior Law Day – Should I Stay or Should I Go?

When the punk rock band The Clash put a song with this title on their 1981 album release, they surely never imagined the classic lyric being used in a Senior Housing context.

Senior Services of Alexandria (SSA) along with the Alexandria Bar Association is proceeding with its annual Senior Law Day — only virtually this year. Instead of the usual half-day program, it will be broken into three virtual panel discussions. The overall theme, “Should I Stay or Should I Go,” addresses housing for older folks, financial concerns around housing and care, and estate planning. Experts from these fields will speak on three successive Fridays beginning September 11.

The first panel will address the big picture of housing, from Aging in Place to Downsizing and Home Modifications to Senior Communities — plus the legal documents that go with such options.

The second panel will address financial concerns such as long-term care, Medicare/Medicaid, what the different housing options may include, as well as tax breaks and funding home modifications.

The third panel will cover Estate Planning, from basic documents, powers of attorney and other “agents,” and the impacts of such documents — or lack thereof.

The first panel on September 11, features Rachel Baer, Esquire, to address legal documents related to housing, Heidi Garvis of Caring Considerations to address the costs of home care vs. community care, and myself — Pete Crouch, Seniors Real Estate Specialist at McEnearney Associates, Inc. to speak to housing options.

As for housing options, there are many, many choices to consider as we age. The first is clearly Aging in Place, which, as the name implies, means staying put in your current housing. It does require, however, making a plan for potentially changing health and financial considerations. Houses, condominiums and apartments can be modified to make them more compatible with such considerations over time, and a well-thought-out plan can make all the difference.

We are also very fortunate in our area to have many options for housing. A large number of older Alexandrians have chosen to move to condos and apartments. The idea is to lessen the maintenance burden of single-family dwellings, provide one-level living, and enhance social interaction, among other benefits. In fact, almost half of the members of our local Senior Village — At Home in Alexandria — have downsized to condominiums and are Aging in Place there. Again, financial and estate planning considerations can be crucial.

Another option is our local Senior Communities. These range from Independent Living to Assisted Living to Memory Care to Life Plan Communities (also known as CCRC’s — Continuing Care Retirement Communities). Each has its strengths and its appeal.

I encourage you to register for Senior Law Day(s), so you can learn about all of the topics covered in this article and more. Registering once gives you access to all three panel discussions, starting September 11 from 2-3 p.m. Take in your housing education from the safety of your home! Please join us!

Register here for 2020 Senior Law Day.

Pete Crouch has been a licensed Broker in Alexandria for over two decades. Pete also has a specialty in Mature Moves and he is a Board Member for At Home in Alexandria (AHA) Senior Village. He was the 2018 National Recipient of the “Outstanding Service Award” for work with Senior Communities. Text 703-244-4024 or email PCrouch@McEnearney.com for a copy of his Downsize Alexandria! Booklet about living more simply in Greater Alexandria.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()