Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

What’s the status of the mortgage industry this fall?

As we roll into fall 2021, the US mortgage industry will see some changes, some more attractive to consumers and some not as much.

Recent positive changes include a reduction in the spread between rates for owner occupied properties and those for second homes and investment properties. Several months ago, regulatory changes caused significant increases in the rates for non-owner occupied properties.

For a period, the rate spread between primary residence properties and non-owner occupied could be as high as 1.75% in rate. That spread is now back down to roughly .500% to .750% making investment purchases and second home purchases more tenable.

At the start of the pandemic, Fannie Mae, Freddie Mac and most of the secondary market imposed various additional restrictive underwriting guidelines. The purpose of the tighter underwriting guidelines was to protect lenders from potential increased risk associated with pandemic related economic downturns. At this point most of the more restrictive guidelines have been lifted and underwriting guidelines generally reflect pre-pandemic standards.

Mortgage program options have continued to rebound as well. Some programs were suspended early in the pandemic, again to allay risk. Many lenders suspended their non-conforming or jumbo programs. At Atlantic Coast Mortgage we suspended our construction loan and bridge loan programs at the beginning of the pandemic.

The good news is we have brought those two programs back. Additionally, we added programs such as special loans for doctors and lawyers. Most lenders in the secondary mortgage market have brought back their jumbo loan programs. The loan program offerings for consumers today generally mirror those offered prior to the pandemic.

The last bit of good news is conforming loan limits are going to increase significantly at the start of the new year. There are no official numbers currently, but we expect the standard conforming loan limit to increase from $548,250 to at least $625,000. At Atlantic Coast we have already begun making conforming loans up to that loan amount.

In the Washington Metro area, we enjoy the benefit of the 2nd tier conforming loan limit which is currently $822,375. That number will also likely increase to somewhere close to $900,000. Conforming loans have less restrictive underwriting standards including lower down payment requirements which make it easier to purchase property in the ever increasingly expensive Washington area.

Now for the less than pleasant news. Interest rates are increasing. We knew it would happen and it is generally a sign of an improving economy. Interest rates have been in the two percentiles for most of the past year. The Federal Reserve’s response to the pandemic economy were the reason for the historically low rates and now the Fed is faced with the need to address the reality of significant inflation. Generally, the Fed’s response to inflation is to increase the Fed funds rate which also has the impact of driving up all other interest rates as well.

Mortgage interest rates have inched into the low three percentiles for most transactions, and we expect they will continue to rise in the coming months. An increase in rates has an impact on a consumer’s ability to qualify for loans. At some point that will translate to pressure against the rising cost of housing. The lack of housing supply has been the primary driver of the cost and it will continue to be so, but a rise in rates will have some tempering affect.

Brian Bonnet, Senior Loan Officer (NMLS ID# 224811) of Atlantic Coast Mortgage, LLC (NMLS ID# 643114).

If you would like more information to help plan your next move, please contact Brian Bonnet at bbonnet@acmllc.com or call 703.766.6702.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

When I Fall in Love With a House, Should I Discuss it With My Agent While in The Home?

With today’s amazing technology, it’s increasingly likely a home may have a security system or other recording device in use. Homeowners regularly use cameras and sound recording devices for many reasons. Sometimes it’s a security concern, while other times it’s just to see who’s at the front door. Some use cameras and listening devices to check on their children while the babysitter is there or to make sure their puppy is not misbehaving. Whatever the reason, when you’re buying or selling a home, home recording devices should be considered.

One of the first things we tell our buyers when starting to look at homes is to wait until you’re outside to tell us that you love the home. And we certainly don’t want discussions about value and pricing inside the home.

We don’t want to give the seller any inside information on your thought process, especially if you decide to make an offer. We certainly don’t want our buyers to lose any of the negotiation leverage we hope to bring to the table, especially in this competitive market. Have you heard the expression poker face? Don’t show your cards to the other party, either with your face or verbally, when touring a home, whether it’s a private tour with your agent or when you are attending an open house.

So, what are your rights and responsibilities as it pertains to real estate? As a seller in Virginia, the listing agreement asks a question that you must answer honestly, disclosing whether you have a recording system in your home. If you do have a recording system for audio, your agent is required to disclose this to all buyers and their agents.

We know of a situation where the sellers checked the box for “no” audio, forgot about this and decided to check in on their puppy cam, which had been set up and not looked at in a couple of years. Their home had gone under contract with multiple offers, and there were no contingencies or further negotiations that would be affected. However, on a buyer visit to measure for window treatments, they heard the realtor and buyers criticizing their decor. They were offended and told their realtor about this and said that if they were not already committed, they would never have chosen this buyer. They were reminded by the realtor that they were in the wrong for listening, and they were instructed to turn off the camera for any future visits. In Virginia, it’s illegal to record a conversation without consent.

We also know of an instance where a seller signed into their recording system to hear the comments of buyers during their open house. They overheard comments about their home being overpriced, and they were furious. Their realtor had to remind them that they should not have had a recording device in the home without disclosure and that it needed to be disabled immediately — or post warning signs so realtors and buyers were aware.

According to a recent LendingTree survey, 30% of home sellers admitted to using hidden recording devices during open house visits. The study also showed that 44% of buyers would back out of a contract if they learned that the sellers had been recording them.

As a buyer, your rights are clear. A seller must disclose the presence of sound recording devices. If it’s simply a camera, with no sound recording, they do not need to disclose, but under no circumstances can a camera be in a private section of the house, such as a bathroom.

The reality is that cameras are present more and more and sometimes sellers don’t need to disclose, even though it is courteous to do so. There are also homes where audio is being recorded, even though it should not be, without disclosure. Sometimes sellers forget to disclose. It’s better to be safe than sorry. As a buyer, you should only discuss the home once you’ve departed the property. As a seller, know your responsibilities, disclose the presence of cameras and turn off all sound recording unless you post signs.

The Peele Group works with their seller clients to make sure that they are aware of the laws and that they are in compliance. We work with our buyers to protect their privacy and put them in the best position for strong negotiations.

If you’d like to discuss your plans for buying or selling a home, we are here to help! Reach out today to Kim and Hope Peele at 703-244-5852.

Kim Peele is a licensed real estate agent with McEnearney Associates, Inc., lives in Old Town and works in VA, DC & MD. She and her daughter Hope Peele are The Peele Group. Kim is a second generation Realtor and fourth generation Washingtonian and is dedicated to helping owners through the challenges of selling their home.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Where in the World Wide Web can I settle on my new home?

It started in March 2020 — my first “drive-by” settlement in a parking lot with sellers getting a clipboard, papers and a clean pen through their car window. I was in another car watching with my phone on speaker. The buyers copied the process 15 minutes later — same parking lot, same paperwork plus loan documents. It worked. One-time event, right?

Au contraire — as in so many areas, the real estate world has permanently changed due to the pandemic and safety worries. Here are some distinct differences in today’s world.

In the olden days of pre-2020, the highest tech was a “mail-away” scenario where papers were sent to sellers to print and go to a bank to find a notary wherever they were.

Now, the notary will come to you (called a mobile closing or remote notarization). The title company will designate a company and have a trained human come in person to your dining room table to tackle the papers and authenticate the actual signing before scanning and shipping everything to the closing company. For my clients, with the keen cooperation between the lenders and the title company, my far-flung sellers have opened their doors to these live notaries and completed their work in places from Vancouver to Colorado Springs to Naples, Italy.

A remote company can also handle long-distance virtual seller signings, and this is called eNotary. Just this year, I have had legal electronic signings occur with a seller recuperating in a Paris hospital and others unpacking at their new home in Austin, Texas. No face-to-face human interaction — just phone connections and internet presentation of the documents.

Buyers can now occasionally join in on the long-distance, remote-signing fun. International settlements were recently tricky due to time zones and FHA/FreddieMac/VA loan requirements that everything be signed on exactly the same date, which meant staring at the door waiting for FedEx or DHL to appear before 5 p.m. Now, buyers can standby for that very long-distance call, ask their questions and make an appointment with the approved eNotary.

“Hybrid settlements” have increased exponentially. According to one title company, every month more and more diverse closing styles are taking the place of sitting around the table at the lawyer’s office or settlement company conference room. I miss the camaraderie and ceremony of the group meeting of the sellers and buyers, but times have changed… Some in-person, some electronic, some in-office, the variable scenarios do add up to the official transfer of property, just without the warmth, good cheer, key transfer and stories about the neighborhood cat everyone feeds or the wonderful UPS fellow who goes the extra mile.

So why not just have local someone else show up to sign, you ask? There are strict rules these days on granting a Power of Attorney (POA) to sign on your behalf. No one with a financial interest in the transaction can be given this responsibility, so you need to find a relative, trusted friend or hire another attorney not involved in this specific closing. And, that person needs to actually show up ready to perform the tasks. “Wet signatures” with real ink are still required on Deeds of Trust, though one-by-one some jurisdictions are allowing carefully controlled electronic signatures. Even so, worry remains about the potential for foul play or hacking.

The burden falls heavily upon the buyers, no matter where they are, to watch for emails several days prior to the official closing date and to actually READ the documents, check the math and ask the questions that might have normally come up around the table. Corrections can be made, but time is always a factor. I suggest doing the walk-through five to seven days before settlement so that any adjustments can be made without stress. They may still have to find a bank officer, military base legal office or embassy to notarize last-minute changes, but progress is being made at every turn.

Happily, complicated and simple home sales continue every day. However, with more settlement styles and options, the world has turned upside down for the better. Welcome aboard!

These thoughts and years of experience are brought to you by Ann Duff, Realtor, with McEnearney Associates. Based in Alexandria, Ann is busy day-in and day-out in D.C., Maryland and Virginia, listing, selling, and leasing distinctive properties with and for wonderful people — and all with a splash of fun! Let’s Get Busy… contact Ann at 703-965-8700 or visit her website AnnDuff.com.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

What Updates Should I Consider if I’m Thinking About Selling My Home in a Year

This is a frequently asked question and one I am happy to address here. It is also a service I provide to my friends, neighbors and potential clients on a regular basis.

Start at the street, remembering that you only have one chance to make a first impression.

Does your home have curb appeal? Based upon the condition of the outside, would a buyer be motivated to check out the inside? Or do you need to think about painting, enhanced landscaping, new front door hardware or gutters? Is the driveway or sidewalk cracked? Does the fence need to be repaired or power-washed and stained? How old is your roof? (All buyers ask this question!)

Take a look at the photos of recent sales in your neighborhood to identify what the sellers did to get ready for market. Then walk through your house room by room to make a list of what types of repairs and/or upgrades would best showcase the features of your own home.

Because you have time before you are seriously thinking about selling, you can spread the updates and budget over a period of time. So many people wait until they are about to sell their house to make changes, and then wish they had been able to enjoy them earlier.

Consider the condition and age of your floors, walls, light fixtures, countertops, cabinets, bathrooms, and appliances and systems like the A/C, furnace, and hot water heater. Once you have your list, determine the priorities based upon your budget, keeping in mind that there are ways to update without a full remodel.

Unless you are planning to sell your house “as-is,” meaning you are not going to make any repairs or replace any of the mechanicals, buyers may pass on a purchase that will require a new HVAC system or roof or a home that has previous water damage. Fix those things upfront rather than waiting until a home inspection creates an opportunity for your buyers to void the contract.

Keep in mind that fresh paint is the least expensive way to make a big impact. I have a lime green kitchen, hot pink bathroom, and orange accent walls in addition to my collection of colorful contemporary art. I love the look, but I know that the colors will be distracting to buyers when the time comes. Although I have no intention of selling, I just had all of my hardwoods refinished, added new light fixtures and ordered some new furniture. I am also painting the walls white and moving my artwork around for a fresh new look to a home that I have lived in for almost 24 years.

Keep in mind that your goal when selling your home is to provide the potential buyers the opportunity to picture their own furniture and accessories in the space — not to worry about what they need to fix or replace. Take a step back, keep an open mind and consider bringing in a professional to make some suggestions.

Whether you are thinking of buying or selling — or just need suggestions for updating your home — I am happy to provide ideas or recommend contractors for your specific projects. I am a resource for the duration of homeownership, not just the buying or selling process. Feel free to reach out anytime!

Lisa Groover is a licensed real estate agent with McEnearney Associates, Inc. in Old Town Alexandria, VA. As an active member of the community since 1989, Lisa specializes in Alexandria, and is thrilled to have the opportunity to work closely with her friends, neighbors, former clients, and their referrals.

In addition to enjoying the Old Town lifestyle and the art related events and activities, she is a member of a number of volunteer organizations. Having had eight Golden Retrievers, she is dedicated to helping other dog owners through the challenges of renting, buying and selling their home.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Private Sale or Full Market Exposure?

Making an Informed Decision

By David Howell, Chief Information Officer, McEnearney Associates

In today’s hot real estate market, some sellers may be tempted to sell their home privately, although a private sale does not include full exposure to the market through the multiple listing service (MLS), the internet, and the thousands of agents and brokerage companies who work in this region. We’ve heard a number of possible reasons for wanting to do so, including convenience, privacy, and security.

At McEnearney Associates, we believe homeowners have the right to make that decision. We also believe that it is crucial to be informed, and sellers should fully understand the implications of listing privately when making their decision. The simple fact of the matter is — regardless of the listing company — sellers almost always benefit from full market exposure, and the data validate our conviction.

BrightMLS, our regional multiple listing service, recently completed a two-year study looking at almost a half-million sales and analyzing the results of “off-market” sales vs. those sold through the MLS. To help ensure objectivity, the study was guided and validated by two Ph.D. Economists who have no ties to the MLS. The results are conclusive.

The study showed sale records of homes that were sold through the Multiple Listing Service and promoted to the entire BrightMLS network of 95,000 real estate professionals, concluding that these homes sold for higher prices than homes sold off the Multiple Listing Service. The median sales price for homes sold on-MLS was 16.98% higher than homes sold off-MLS. Similar results are demonstrated across BrightMLS’s three major Metropolitan Statistical Areas (MSAs) of Philadelphia, Baltimore, and Washington, DC.

As a subset of off-MLS sales, Bright analyzed “private sales,” which are defined as office exclusive listings promoted only within a brokerage office or company. Those office exclusives make up a small percentage of transactions, and nearly two-thirds (63%) ultimately end up not selling off-market and are instead promoted through the MLS. Like the findings from all off-MLS sales, homes marketed on the MLS sold for a median sales price of 16.84% more than those marketed through office exclusive arrangements. Additionally, those office-exclusive listings typically took longer to sell: homes entered into the MLS from the start went under contract faster than properties that started as an office exclusive and were later marketed on the MLS. (See the full BrightMLS Report at McEnearney.com/on-off-mls-study.)

It’s stunning that the results are so similar and so compelling.

Now, doesn’t this stand to reason? No individual agent or company has access to all of the buyers or even the majority of the buyers. Thus, in a time of record-low inventory, does it make economic sense to artificially restrict the number of buyers who could be interested in a property? To intentionally curb the demand side of the supply and demand equation?

Furthermore, we believe it is in the best interests of our clients to provide all qualified buyers equal access to all homes on the market, not only to protect equal housing opportunities but to ensure that they maximize the value of the investment in their property.

We’ll leave you with the following two questions that you should consider when listing your home:

- Is almost 17% a big price to pay for the perceived “convenience” of selling off-market?

- Who benefits most from an off-market sale – the seller or the listing company?

Take a look at our website for all of our listings available throughout Washington, D.C., Maryland, and Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

How much is my home worth?

Whether you just bought your home or you have owned it for years, it’s always fun to keep up with the current value and to see how your investment has appreciated.

As interesting as it is to see the recent sales and speculate your home’s worth, it’s important to note that many homeowners get a false idea of value by looking at online sites and other assessments. While those sources offer estimates of home value, most of them are not accurate and are just very rough approximate values. This is fine if you are not planning to sell anytime soon. However, it is super important to know the correct value range when it’s time to put your home on the market.

Your most important resource for a true value assessment of your home will be an experienced professional Realtor.

First, let’s talk about where homeowners tend to find information on home values. Everyone gets a city or county tax bill, which includes an assessment of value. The tax assessed value can be much lower or much higher than what your home would actually sell for on the open market. In most cases, an assessor has never seen the inside of your property. They use a software program based on sales data and a rough comparison of property features. Their goal is to provide a tax bill for town revenues, and they are not purporting to be an accurate source of value.

Another popular, yet misleading, source of home data is online valuation sites. Zillow is the main one that homeowners cite when discussing value. However, as with most of the online sources, Zillow gets its information from a combination of county websites, user input and recent sales. They publish their margin for error on their website, and in many cases, the error range can be significant. For instance, in Arlington County, Zillow lists the median error rate as 2.5%, so their valuation of a $1 million home is likely to be off by $25,000 or more. In other areas, the error rate is even higher. To view the Zillow margins for error in Virginia, check out Virginia Data Coverage and Zestimate Accuracy.

Another frequently used source of value is the neighborhood grapevine. Your neighbor sold their home, had multiple offers and it sold for well above list price. You think that your home is better than their home, and therefore, you decide that your home value is even higher. Unfortunately, unless you are planning on listing your home within a few weeks of your neighbor’s sale, this data can be unreliable. The real estate market can change drastically in just a short period of time, and it is important to look at not only comparable sales, but also the most recent ones. And, of course, the ages of the roof, HVAC, windows and other features must be accounted for in a value calculation.

So, as you can see, county assessments, online sites and neighbors are frequently used unofficial sources of home value. It’s fine to keep tabs on the market using these sources if you just want a general idea of value, but when the time comes to get serious about selling your home, it’s time to drill down into the details to determine value.

When the time comes to sell your home, what do you do to determine a good list price?

First and foremost, consult an experienced Realtor. A good full-time Realtor sells 20+ homes a year, brings lots of experience to the table and knows the nuances of pricing a home for sale.

Before you ever sell your home, your professional Realtor will prepare a Comparative Market Analysis (CMA). A CMA will take into account a wide range of very specific information, and most importantly, will include data on all sold homes in your area within a 6-12 month period.

The CMA will compare an array of features including: square footage, number of bedrooms, number of baths, style of residence and number of stories. Once the size is closely matched, then the qualities and updates of the home should be studied and factored in. This will include things like size of lot, orientation of the lot, your home’s location in the neighborhood, the age of roof and windows, upgrades to kitchen and baths, type of floors, and more. All of this will be compared to recently sold homes of similar size, to determine a value range for your home.

Lastly, your Realtor will discuss your home’s value range with you and make recommendations on what the best list price would be to drive buyer traffic in to see your home. A great Realtor will be able to suggest a list price that ends up being very close to the final sale price. Ideally, you will have chosen a list price that appeals to buyers and is supported by all the features of your lovely home, resulting in a quick sale at top dollar!

For a no-obligation Comparative Market Analysis for your home, reach out today to Kim and Hope Peele at 703-244-5852.

Kim Peele is a licensed real estate agent with McEnearney Associates, Inc., lives in Old Town and works in VA, DC & MD. She and her daughter Hope Peele are The Peele Group. Kim is a second generation Realtor and fourth generation Washingtonian and is dedicated to helping owners through the challenges of selling their home.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Buying an investment property or vacation home

With an increased need for privacy and cleanliness while vacationing, many people chose to stay at a place that felt like home away from their home this past year by renting a short-term property through websites like VRBO and AirBnB.

I recently stayed in one such vacation home with my family that was clearly a second home for the owners. I couldn’t help but think a number of times while we were there that it would be great to have a second home like this while having a supplementary income to finance it. By providing a wonderful vacation home for others, owning a second home comes into the realm of possibility for more homeowners.

But how feasible is it actually to own a short-term rental? There are three important things to consider before taking the plunge:

1. Know the law.

Ignorance of local laws is not defensible in court. Each jurisdiction has specific laws about short-term rentals and you should be aware of them before you purchase. Your Realtor should be able to recommend a good attorney who would have the answers to any questions that you might have. Also, a good Realtor has a network of trusted agents across the country who can help you find a home outside of their jurisdiction so that the purchase of your second home runs smoothly.

2. Only buy a home you would want to live in.

Many areas of the country are wonderful, vacation hot spots for a reason, but if it doesn’t match your style, don’t buy it. If you don’t enjoy spending time at the beach, don’t buy a beach home just because you think other people will like it. Some people are beach people, others are mountain people. There will be other people who find value in your property.

When purchasing, it is best to make a list of positives and negatives about the property that you are considering. Can you picture yourself in this home for years to come? Can you imagine coming back with friends and relatives? What will Aunt Mabel think about this place? Do you know the area and could find someone to look after it for you if a problem arises while the house is being rented? If a home checks everything off of your list, it might be a great option for you!

3. Ease of getting to and from the home and access to amenities.

You may find out that the local laws are amenable to short-term rentals and you love the area, but how easily accessible is the home? We stayed in a vacation home once that was on the side of a very steep hill. There was not much flat space to run or play, and the nearest town and grocery store was a half an hour drive away on sharp, twisty mountain roads.

While you may love the privacy, and it would look attractive to a first-time renter unfamiliar with the area who found the house online, a location like this may deter repeat business.

The best short-term rentals are those that you can rent again and again to the same people. It allows you to develop a relationship with them and know the people who are staying in your home and what state of cleanliness they will leave the home in afterward. Not only that, but repeat business ensures your potential rental income for the future. There was probably a reason that attracted you to the area in the first place — highlighting the features of the home to your renters will make them want to keep coming back.

Of course, there are many other things to consider before purchasing a second home, but with the rise in short-term rentals, low interest rates and ease and convenience of finding renters through online websites, there has never been a better time than now to jump into the secondary home market.

Jean Beatty is a licensed real estate agent in VA, MD, and DC with McEnearney Associates Realtors® in McLean, VA. If you would like more information on selling or buying in today’s complex market, contact Jean at 301-641-4149 or visit her website JeanBeatty.com.

Take a look at our website for all of our listings available throughout Washington, D.C., Maryland, and Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

What is Home Staging?

Staging is preparing a home for market by furnishing and decorating it specifically to attract potential buyers. Through the use of furniture and accessories, staging helps buyers envision how the space can best be used and makes the property appealing. It puts the home in its best possible light by accenting the home’s positive features and helping enhance the flow of the rooms.

Will the stager use the seller’s furniture or bring in furniture?

There are many different approaches to staging, depending on whether or not the seller has moved out of the property. In a vacant home, a stager will bring in furnishings, rugs and accessories. This is the most effective approach because the stager is working with a “clean slate” and is able to create a home atmosphere appealing to buyers with on-trend items that the stager has preselected just for that purpose.

A stager may also work in a home still occupied by the seller and use the seller’s furnishings. In this situation, the stager first goes through the home with the seller, removing and packing up as much of the seller’s belongings as possible. Off-season items, personal photographs, collections and infrequently used items are some examples of what is packed away. If there are packed items that the seller needs to use on a daily basis, the stager will ensure those items are accessible. Once the home is cleared out of excess items, the stager will rearrange furniture, rugs, window treatments and lighting to enhance the home’s atmosphere. Frequently, additional items are brought in from the stager’s inventory of furnishings to round out what is in the home and complete the staging effect.

Is the entire house staged or only certain rooms?

It depends on the size of the property and the staging budget. Standard rooms to stage are usually the living room, dining room, kitchen, family room, primary bedroom and a bathroom. The secondary bedrooms do not need to be staged unless one is to be staged as a home office. With everyone working from home in the last year, a home office is now also standard for home staging. Even if it is not a separate room, having a dedicated space for a desk and work area is an important feature.

Staging outdoor space is now popular as well. Outdoor spaces do not have to be full kitchens or outdoor wet bars as seen in luxury magazines and home television shows. Showcasing a patio off the kitchen with a table and chairs as an alternative dining area or highlighting a fire pit with Adirondack chairs in either the front or backyard as a gathering spot is appealing to buyers who value having that additional living space at their home.

How much does staging cost and what are the benefits to the seller?

Prices for staging vary widely in Northern Virginia depending on the company and services being used. On the lowest end, a staging consultation may cost several hundred dollars for a few hours of advice. For full service, a vacant home that has staging in the living room, dining room, primary bedroom and bathroom, home office, family room, and patio will cost approximately $3,500 to $5,000 for the first 30 days. Renewing for a second month will usually be slightly less.

Staging offers big benefits for the seller, including a higher sales price and fewer days on the market on average. Research shows that staged homes sell for 20% more than homes not staged, and they sell 88% faster than homes not staged. The seller must be willing to invest in the staging costs at the time of listing or be willing to pack up most of their personal belongings to realize these benefits.

What is virtual staging?

A budget-friendly alternative to in-home staging is virtual staging. Virtual staging is photographically staging a home for online viewing by potential buyers. To create the virtually staged home, the property is photographed empty without furnishings. After the photos are uploaded, furniture and staging items are virtually added to the photos. The property will remain empty for actual buyer tours, but the online virtual staging will help potential buyers envision a fully furnished space.

Kathy Hassett is a Realtor with McEnearney Associates and a partner with the MPH Home Team in Alexandria, VA. Kathy has lived in Alexandria for over 25 years and started her journey in real estate as a settlement attorney in 1993. With her in-depth knowledge of the local area and her real estate know-how she serves as a strong advocate for her clients’ best interests. She provides her clients with experience-based strategies to help them navigate real estate transactions, reduce their risk, and save time and money. She would love the opportunity to work with you. Contact her today at 703-863-1546.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

Should I Rent or Buy?

When considering a move, sometimes there’s a dilemma. Is this the right time to buy, or should I rent again? In some areas of the country, it’s a clear choice. If mortgage payments will be consistently lower than rent, or at least close, there is an obvious opportunity to see appreciation in your investment and come out ahead in a few years. In our area, it can be a little tricker.

The first step in your decision-making process is to find a good Realtor who will be patient, answer all of your questions and see you through the process — whether you decide to rent or buy this year. Your Realtor will guide you through the process of shopping for homes that fit your situation and budget and will negotiate diligently on your behalf when the time comes. They also have great resources and can refer you to trusted lenders, which is your second most important step in making your decision about a home!

Whether you want to buy now, or even in a year or two, an experienced local lender will provide all the important financial information that you need to make your decision. They will look at your credit score, job history, income, as well as your assets and debt. All this information will help them to map out the best plan for your future, regardless of where you already are in the process. A good lender will give you options for loan programs, helping you create the most competitive offer when you are ready to buy, and they will show what your interest rate would be depending on how much you put down on your loan. They will also have guidance for you on how your tax savings may allow you to make a mortgage payment higher than what you would be comfortable paying for a rental. Your Realtor and lender should be identified early, as they will become your close advisors in this journey to decide whether to rent or buy.

Let’s talk about the upside of buying. Clearly, there are many reasons to buy. First, you can truly make your home your own. Remodeling, updating and even just painting are all your decisions and to your tastes. Second, your investment will grow and make money for you as home values increase. Third, depending on the mortgage program chosen, your payments will remain almost the same for many years, except for minor changes in taxes and insurance. Lastly, the cost of waiting will be higher interest rates — now at all-time lows — and more expensive homes. Your buying power will lessen the longer you wait.

A few years back, we met Margaret and Devon (names have been changed) at a rental in Alexandria where the monthly rent was $2,700. It was a 2-bedroom, 2-bath condo about a mile from the center of Old Town. They were newlyweds and expecting their first child. They mentioned to us that they didn’t think that it would be possible for them to own a home in this area. We suggested they talk with one of our favorite lenders, and they discovered that a mortgage payment for a home up to $550K would be about the same monthly payment. Also — they could get away with just 5% down. Like many newlyweds, they didn’t have quite that much to put down, so their parents gave them a tax-deductible gift of $25K. In this instance, it made much more sense to buy than rent, and this family was thankful for the information. Several years later, their $549K purchase is now worth $635K and growing.

Now, let’s talk about the cons of buying and why some are deciding to rent.

First, when you buy a home, the maintenance becomes your responsibility, so knowing exactly what you are getting into is important. How old are the systems in the home and the roof? What’s new, and what will need to be replaced in the next few years? Your realtor will help you evaluate the home and get the necessary inspections.

Secondly, it’s often competitive to get a home. This past year has been a seller’s market in much of the U.S., and Northern Virginia and D.C. have been particularly difficult areas for buyers. Many listings have had anywhere from 5 to 20 offers on them. Low interest rates and pandemic-induced cabin fever has caused people to reevaluate their space, and in many cases, look for a newer, larger home. The Amazon headquarters and new Virginia Tech campus on the Route 1 corridor created a lot of buzz about increasing values. All of this resulted in high demand and low inventory.

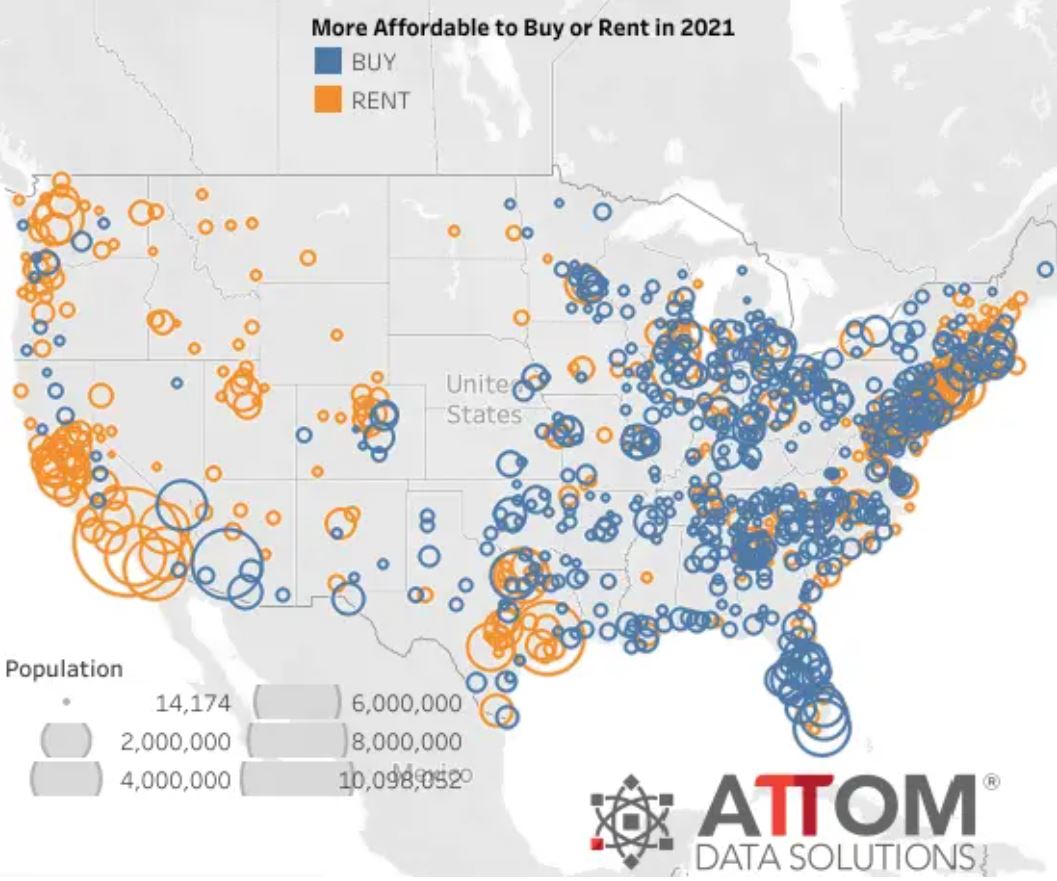

Photo Courtesy Of: Attom Data Solutions

According to ATTOM Data Solutions, a property database company, “owning a median-priced three-bedroom home is more affordable than renting a three-bedroom property in 63% of the 915 U.S. counties analyzed for the report.”

The bottom line is, your decision on whether to buy or rent will be unique to your situation. You should talk to a Realtor and a lender, sooner rather than later. They will help you with a full evaluation of the market and of your buying power so you can make an educated decision on whether to buy a home this year or to wait.

And, of course, if we can be of assistance, we are always happy to help! We would never try to convince someone to get into a situation that they cannot afford. However, we would also never want someone to miss opportunities that they can afford because they didn’t know their options. Homeownership is often more attainable than people realize. Simple education, guided by the experts, is the key to not missing out on your chance to invest in your future! For a confidential meeting, reach out to Hope and Kim Peele at 703-244-5852.

Kim Peele is a licensed real estate agent with McEnearney Associates, Inc., lives in Old Town and works in Virginia, D.C. and Maryland. She and her daughter Hope Peele are The Peele Group. Kim is a second-generation Realtor and fourth-generation Washingtonian and is dedicated to helping owners through the challenges of selling their home.

Take a look at our website for all of our listings available throughout Washington, D.C., Maryland, and Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()

How To Say Goodbye To Your Home

Selling your house and saying goodbye to the home that you lived in can be a very emotional experience for a lot of homeowners.

If you have lived in your home for a long time, you probably made many unforgettable memories with your family, friends and loved ones that it will be hard to let go of when the time comes to move. Whether you realize it or not, you have an emotional attachment to this home, and as you think about moving, you can be overcome with feelings of sadness and hesitancy.

I would like to introduce you to the three transition methods I use with my clients to help ease their minds about their upcoming move.

1. Make Memories Before You Leave

Begin by taking pictures of your home inside and out, even before you begin the moving and packing process. Every crayon scribble, crooked picture and misplaced sock is a sign of a well-loved and well-lived home.

Take photos with your favorite neighbors and caption them with their names and dates. Hopefully you will keep in touch after the move, but you will never have the same kind of relationship when you no longer live next door to each other. You can also say goodbye to your favorite cashier at the local grocery store, or the pharmacist who always refills your prescriptions. It helps create closure for you and it makes them feel like you’ve noticed their hard work over the years.

Have dinner one last time at your favorite restaurant if you are moving very far away and take a commemorative photo. Write down your usual order on the back so that you can always remember your times spent there.

2. Take Something with You

Just because you are leaving doesn’t mean you can’t take something with you! Create a memory box of items around your yard. Leaves from the trees, presses of the flowers from your garden or a watercolor sketch of what your home looked like in full bloom. Many talented artists can create works of art based on your old home that you can display in your new one.

As long as you remove them before your home goes on the market, you can replace certain fixtures in your home and bring them along with you to your new one. For example, I had clients that loved the specialty billiard light fixture they kept over their pool table. They removed the fixture and put it into their new house and replaced it with something less unique for the new buyers.

Make sure you do replace anything you take with you though, otherwise the market value of your home will go down.

3. Look Toward the Future

Instead of dwelling on the past, look toward the future! Focus more on the upside of where you are going and the wonderful opportunities that your new home will provide you. You can do a Google search on the new area where you will be moving to and find new restaurants you want to try, new stores to shop at, as well as look up your kid’s new schools.

Look into local classes at the community center or Facebook events that are coming up in your town so that you can meet the people in your new neighborhood. There is something exciting about a fresh start and new opportunities to find new things to love.

Saying goodbye to your home can be difficult, but there is always a reason to be hopeful and optimistic about where you are going. A trusted Realtor can help guide you through the process.

Jean Beatty is a licensed real estate agent in VA, MD, and DC with McEnearney Associates Realtors® in McLean, VA. If you would like more information on selling or buying in today’s complex market, contact Jean at 301-641-4149 or visit her website JeanBeatty.com.

Take a look at our website for all of our listings available throughout Washington, D.C., Maryland, and Virginia.

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()