Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

This year will shake up how everyone is involved in the homeownership process as consumers, lenders, and Realtors explore solutions to keep the housing market moving at a healthy pace. The days of throwing a home on the market and watching multiple offers roll in is probably a thing of the past, but there are still advantages available to both sides to ensure people can buy the homes that are available, even with rates at their highest in several years.

For buyers, taking an (honest!) inventory of finances and speaking with a lender is the first step. While it is advisable to have a healthy cash reserve when buying a home, the old standard of 20% down is rarely the case today. The National Association of Realtors 2022 study of homebuyers and sellers showed that the typical down payment for first-time buyers was 6% while for repeat buyers it was 17%.

But even with lower requirements for a down payment, buyers will still have to qualify for financing and bring money to closing. What are some options to make every dollar count on the pathway to homeownership?

Rate Buydowns: Buyers over the past several years were treated to historically low interest rates in the high 2-percentiles to low three-percentiles. With rates now in the low to mid six-percentile, diminished buyer power is leading to creative solutions in adjusting where buyers start out with their rate – and where they might end up.

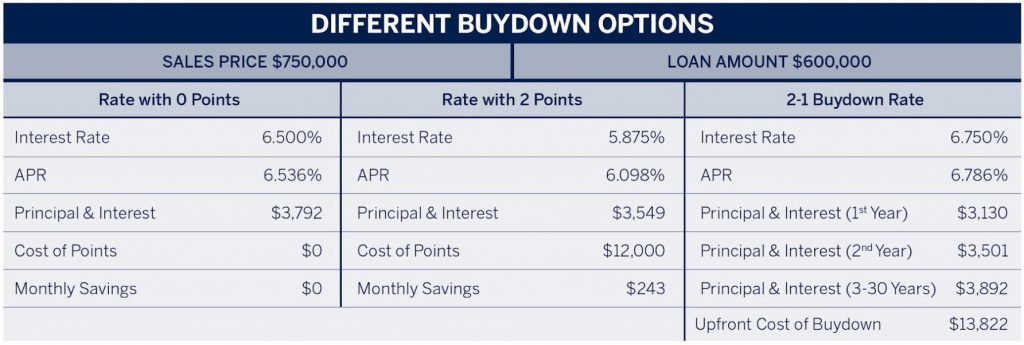

Brian Bonnet of Atlantic Coast Mortgage shared insight into two buydown strategies – one that’s traditional and one that has been sparking conversation among Realtors looking for every option to help their clients. The tried-and-true rate buydown is where buyers lower their interest rate by buying “points” at the time of closing. The lowered interest rate is fixed for the lifetime of the loan and offer buyers a consistent amortization schedule. The “2-1 Buydown” is a temporary rate adjustment where a buyer uses cash to lower their interest rate by 2% in the first year of their mortgage and 1% in the second year of the mortgage, coming back to their full rate at the 25th month of mortgage payments. For example, the buyer who would qualify at the loans note (which is generally slightly higher than the current market fixed rate – let’s say 7% — would pay to bring their rate down to 5% in 2023, 6% in 2024 and back to 7% — the rate at which the buyer was qualified – in 2025.

The benefit of this scenario is that buyers will have a cushion of two years before they start paying the fully amortized rate, and the cash can come in the form of a seller credit (see more on this topic below). Bonnet points out that consumers can’t assume rates will drop or that refinancing will be cheaper in 2025, and must think carefully about whether they will be in a better or worse position when the full rate goes into effect.

“Will rates be better after two years? Will you be in a better financial position to account for the increased interest payment? Will you be able to refinance if you aren’t?” Bonnet said the 2-1 buydown option is good for buyers who don’t expect to be in their home long-term, such as a military buyer who isn’t using their VA opportunity and plans to sell at the end of their assignment. “The typical buyer is not a 2-1 buydown consumer.”

Seller Credits: As buyers navigate higher interest rates, inflation and other economic factors, sellers may see homes taking longer to sell and with more negotiating on terms. In some cases a seller chipping in cash can be what gets a deal to the closing table. An example of a seller credit would look like this: A home is listed for $600,000 and gets an offer from a buyer who is putting a little less than 20% down and financing $500,000. Rather than negotiate the price to $590,000, the buyer offers the seller their asking price of $600,000 but asks for $10,000 to help them cover their closing costs. The net to the seller is $590,000 and the buyer is able to qualify for their loan and close with help from the seller.

Down Payment Assistance: Buyers can explore local grants and down payment assistance (DPA) programs that offer financial resources, some based on income and some are available to certain types of workers (ex: HUD’s Good Neighbor Next Door program that offers available homes at a discount to educators, civil servants, First Responders). To see what local monies may be available in your area, check these HUD resources for Virginia, Maryland and DC.

Government-Backed Mortgage Programs: FHA and VA loans are popular government-backed loans aimed at specific types of buyers and with specific criteria to qualify, usually less restrictive than conventional mortgage loans but with their own mandated processes and procedures. And for buyers who aren’t afraid of a fixer-upper, there are FHA 203(k) loans that serves as a construction loan that finances both the purchase and repairs to a home.

Adjustable Rate Mortgages: While these were popular in the mid-2000’s as buyers were trying to qualify for homes as prices dramatically rose, the economic factors aren’t as favorable for ARMs in 2023. Bonnet explained that because the bond markets currently have an inverted yield curve with a very wide spread, ARMs are generally not offering more favorable terms than fixed rates and signs do not indicate that this will improve anytime soon.

In many ways, consumers are back to basics when it comes to buying and selling a home in 2023. Save money, research options, be prepared to get creative, look for ways to collaborate. There is no magic wand when prices are high, inventory is tight and buyers are squeezed. But working with the right professionals like trusted local lenders and expert McEnearney Associates will get you where you want to go!

Don’t miss a post! Get the latest local guides and neighborhood news straight to your inbox!

![]()